How Does a Gift of Equity Impact Your Taxes? Benefits, Rules, and Tax Implications for Buyer + Seller

Generous parents, grandparents, and other family members may be looking to help their child purchase a first home. If the grandparent already owns real estate, they might want to give their grandchild a gift of equity to smooth the pathway to homeownership. Abrams Valuation Group, Inc. explores the potential tax ramifications of gifts of equity for buyers and sellers and how getting a valuation may help clarify one’s true tax obligation.

What is a Gift of Equity?

A gift of equity occurs when a family member sells a home to another family member at a price below market value. The difference between the actual sales price and the home’s market value is the gift of equity.

How Does a Gift of Equity Work?

When bequeathing a gift of equity, the seller agrees to sell the home for less than its market value, giving the buyer a portion of the home’s value as a gift. The buyer can then use the gifted equity toward the down payment, closing costs, or both.

Gift of Equity Example

If Grandma Smith owns a home worth $1 million and she sells it to her grandson, John Smith, for just $600,000, Grandma Smith has given John a gift of equity worth $400,000. If John wants to put down a 20% down payment on the house, he can use some of the $400,000 gift of equity gift funds towards a $120,000 down payment and some towards closing costs. In addition, his monthly mortgage payments are lower, as he only needs to pay up a loan for a home worth $600,000, rather than $1 million.

Benefits of a Gift of Equity for the Buyer

Lower Down Payment with an Equity Gift

A gift of equity can reduce or eliminate the need for a down payment, which can make homeownership much more accessible to first-time buyers.

Reduced Monthly Payment

The gift of equity can reduce the purchase price of the home, making monthly mortgage payments more affordable.

Private Mortgage Insurance (PMI) Implications

When a buyer receives a gift of equity, it can affect the private mortgage insurance (PMI) requirements. If the gift of equity is large enough to cover a significant portion of the down payment, the buyer may be able to avoid having to pay PMI. This is because the loan-to-value ratio, which is a key factor in determining the need for PMI, is lowered when a substantial gift of equity is applied to the home purchase. Lenders typically require PMI when the down payment is less than 20% of the home’s purchase price. However, the need for PMI may be eliminated if the gift of equity brings the effective down payment to 20% or more. It’s important for buyers to discuss the specifics of the gift of equity with their lender to understand how it may impact their PMI requirements.

Gift of Equity Rules

Not everyone qualifies to give a gift of equity. There are rules and regulations regarding who is an eligible gift of equity donor and lender.

Eligible Donors and Lender Requirements

In the context of giving a gift of equity, a lender refers to the financial institution or individual providing the mortgage or loan for the property. The lender may be involved in assessing the gift of equity and ensuring that it meets the necessary requirements for the mortgage. Lenders specify eligible donors, who may include a spouse, a domestic partner, and a legal guardian.

The donor is the individual or party gifting the equity in the property. The donor is the property’s original owner who is gifting a portion of the property’s equity to the recipient, typically a family member or someone with a close relationship with the donor. Most gifts of equity occur between parents and children or grandparents and grandchildren.

Government-Backed Loans and Conforming Loans

FHA (Federal Housing Administration) loans allow gifts of equity from family members who are not interested parties. In addition, Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Corporation) allow gifts of equity as long as the buyer and seller are related by blood, marriage, or legal guardianship.

Gift of Equity Process

1. Structuring a Gift of Equity for Home Purchase

– Verify lender requirements and obtain a written agreement.

– Confirm that the lender will allow a gift of equity and what their requirements are.

– A formal written agreement or equity letter is essential in outlining the terms and conditions of the transaction.

2. Market Value Assessment and Important Legal Documents

– Obtain a professional appraisal to determine the property’s current market value.

– Important legal documents include the gift of equity letter, purchase agreement, and sales contract.

3. Finalizing the Gift of Equity

– Ensure that all parties involved fully understand and agree to the terms outlined in the gift of equity agreement.

– Complete all necessary paperwork and documentation required by the lender and legal authorities.

– Proceed with the home purchase transaction according to the terms specified in the gift of equity agreement.

Gift of Equity Tax Implications for the Seller

Giving a gift of equity comes with several tax implications for the seller, depending on the seller’s tax situation. As always, it’s important to discuss your personal tax situation with a qualified tax professional who understands all the factors in your situation. Here we will examine the tax implications for the seller in a general way.

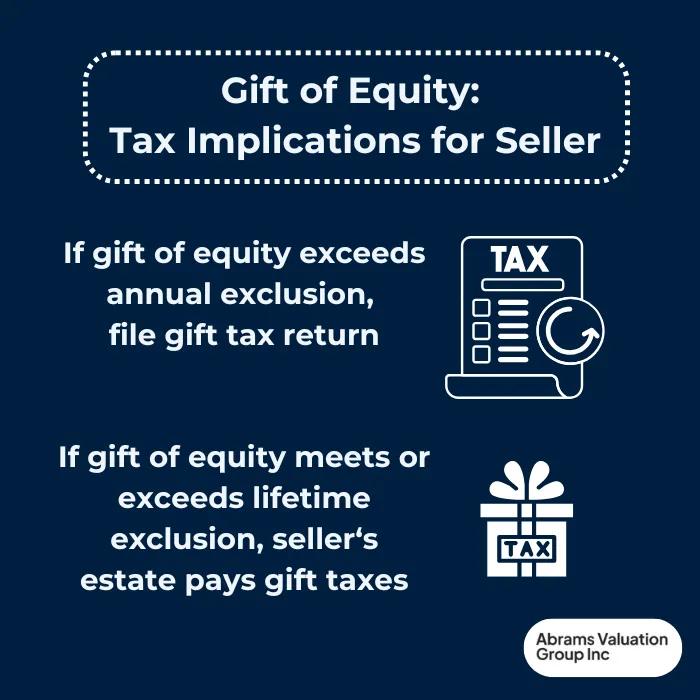

Gift and Estate Tax Considerations

If the gift of equity value exceeds the annual gift tax exclusion for that tax year, the seller must report the gift of equity on a gift tax return, even if they do not owe any gift taxes. If the seller has already met or exceeded the lifetime gift tax exclusion at the time of giving the gift of equity, then the gift will be taxed as part of the seller’s estate taxes at the appropriate gift tax rate for the seller’s estate.

Tax Implications for the Buyer

Capital Gains Tax Considerations

The initial gift of equity has no immediate tax implications for the buyer. However, the buyer needs to realize that it may affect their taxes if they choose to sell the home in the future. This may be something to consider if the buyer wants to buy the house as an investment property versus a primary residence. If the current buyer sells the home for more than they bought it, they will owe capital gains taxes on the profit. This is because they bought the house at below-market value due to the gift of equity.

Getting a Gift of Equity Valuation Can Clarify Tax Obligations

If you are a gift of equity buyer or seller, getting a gift of equity valuation can save thousands of dollars in unnecessary taxes. Real estate values are constantly changing and dependent on many factors, so the gift of equity at the current market value may not accurately reflect your gift, estate, or capital gains tax obligation when taxes are due.

Getting a professional gift of equity appraisal is a wise tax strategy, as it empirically defines your actual tax obligation and is defensible in court in case of an IRS audit. It is an excellent preventative measure to submit a third-party gift of equity valuation to avoid an audit proactively. With Abrams Valuation Group, Inc.’s over 99% audit success rate, you can rest assured that your gift of equity appraisal is in good hands.

Contact AVGI today for a free consultation.

Gift of Equity FAQs

How Does a Gift of Equity Work for Home Buyers?

A gift of equity can help home buyers qualify for a mortgage and reduce their monthly payments.

Can a Gift of Equity Be Used for a Down Payment or Closing Costs?

The gift of equity must be used for the down payment first, and if there is any remaining value, it can be used for closing costs.

Are There Any Restrictions or Limitations When It Comes to Using a Gift of Equity?

There are restrictions and limitations when using a gift of equity, including lender requirements and tax implications.

How much equity can I gift?

The amount of equity you can gift typically depends on the lender’s policies and the specific circumstances of the transaction. It’s important to verify the lender’s requirements and obtain a written agreement that outlines the terms and conditions of the gift of equity transaction.

Is gifted equity taxable?

Yes, gifted equity is taxable, although the tax implications are different for buyer and seller. Furthermore, the taxes are often deferred rather than immediate. For the seller, the gift of equity is counted towards their lifetime gift tax exclusion. If they have already met or exceeded the exclusion threshold, the gift of equity will be liable to pay gift taxes from the seller’s estate after the seller’s death. From the buyer’s perspective, they will only be taxed on the gift of equity if they subsequently sell the home for a higher amount than they purchased it. In that case, they would owe capital gains taxes on the difference between the fair market value of the property and the price they paid with the gift of equity.