Maximizing Foreign Derived Intangible Income: Key Strategies

The Foreign Derived Intangible Income (FDII) deduction offers a valuable tax break for domestic corporations that generate income from exporting intellectual property. Since it was introduced by the 2017 Tax Cuts and Jobs Act (TCJA), the FDII deduction incentivizes domestic corporations with a lower tax rate on foreign-derived intangible income, promoting international taxation and domestic job creation. AVGI experts discuss how to maximize the valuation impact of the FDII rules.

Introduction to FDII and Tax Benefits

The Foreign-Derived Intangible Income (FDII) deduction is a significant tax incentive designed to benefit domestic corporations, including both U.S.-based businesses and non-U.S. companies operating within the United States. Introduced as part of the Tax Cuts and Jobs Act (TCJA), the FDII deduction aims to encourage domestic corporations to retain intangible assets and the income they generate within the U.S., supporting international taxation fairness and enhancing the global competitiveness of American businesses.

At its core, the FDII deduction provides a reduced tax rate on foreign-derived intangible income, rewarding companies for engaging in export activities and generating income from sales or services provided to foreign persons. This incentive not only helps domestic corporations lower their effective tax rate on qualifying income but also promotes job creation and economic growth by making it more attractive to conduct business from within the United States.

To qualify for the FDII deduction, a domestic corporation must earn gross income from export activities, such as the sale of goods, services, or intangible property to unrelated foreign customers or foreign persons. The FDII computation involves several key elements: gross income, deduction eligible income, foreign-derived deduction eligible income, deemed intangible income, and qualified business asset investment. Notably, gross income for FDII purposes excludes certain categories, such as Subpart F income, foreign branch income, and other types of income subject to special tax rules.

A central component of the FDII calculation is the deemed tangible income return, which is determined as 10% of the average adjusted bases of depreciable tangible property—referred to as qualified business asset investment—used in the corporation’s trade or business. The excess income above this fixed return is considered deemed intangible income, which is then eligible for the reduced FDII tax rate.

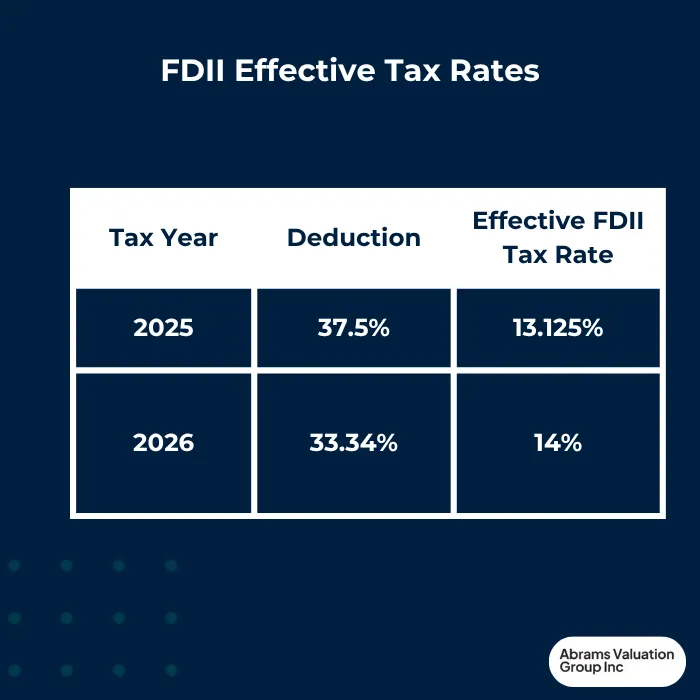

For tax years beginning before January 1, 2026, the FDII deduction allows domestic corporations to benefit from a lower effective tax rate of 13.125% on foreign-derived intangible income, compared to the standard 21% corporate tax rate. This reduced rate applies to the portion of taxable income derived from foreign sales and services, after accounting for the deemed tangible income return. The deduction is subject to certain limitations, including a cap based on the corporation’s taxable income and scheduled reductions for future tax years.

To claim the FDII deduction, domestic corporations must file Form 8993, Section 250 Deduction for Foreign-Derived Intangible Income (FDII) and Global Intangible Low-Taxed Income (GILTI), as part of their annual tax return. It is important for businesses to be aware of the deduction’s limitations, such as the taxable income limitation and the phase-out of the deduction for tax years beginning after December 31, 2025.

In summary, the FDII deduction offers a valuable opportunity for domestic corporations to reduce their tax liability on income derived from foreign markets, supporting export activities and the retention of intangible assets within the U.S. As international taxation rules continue to evolve, staying informed about FDII requirements and related provisions—such as the GILTI regime and tax rules for controlled foreign corporations—is essential for maximizing tax benefits and maintaining a competitive edge in the global marketplace.

Calculating Foreign Derived Intangible Income (FDII)

There are numerous factors that go into calculating FDII. Here are clear steps to calculate your company’s FDII and determine your eligible deduction:

Determine Qualified Business Asset Investment (QBAI):

Calculate the average adjusted bases of tangible depreciable property used in the corporation’s trade or business. This value represents the corporation’s qualified business asset investment.Calculate Deduction Eligible Income (DEI):

Identify the corporation’s gross receipts, which are used to determine gross income and gross DEI for FDII purposes. Gross DEI is a key component in the calculation and allocation of deduction eligible income. Exclude certain types such as Subpart F income and foreign branch income. Then subtract all deductions properly allocable to that gross income to arrive at the deduction-eligible income.Compute Deemed Tangible Income Return (Deemed Return):

Multiply the QBAI by 10% to determine the deemed tangible income return, also referred to as the deemed return. This represents the fixed return on tangible assets.Calculate Deemed Intangible Income (DII):

Subtract the deemed tangible income return (deemed return) from the DEI. The result is the deemed intangible income, representing income attributed to intangible assets.Determine Foreign-Derived Deduction Eligible Income (FDDEI):

Identify the portion of DEI that is derived from sales or providing services to foreign persons or related parties for use outside the United States. Then subtract deductions properly allocable to this income to calculate FDDEI. Proper documentation of these transactions is important to ensure qualification.Calculate the Foreign-Derived Ratio:

Divide FDDEI by DEI, capping the ratio at 1. This ratio represents the proportion of income that qualifies as foreign-derived.Compute FDII:

Multiply the deemed intangible income (DII) by the foreign-derived ratio. The result is the foreign derived intangible income eligible for the FDII deduction.

Example:

Suppose a corporation has $10 million in gross receipts, $8 million in gross income, and $6 million in deduction eligible income (DEI) after subtracting allocable deductions. Its QBAI is $10 million, so the deemed return is $1 million (10% of QBAI). The deemed intangible income (DII) is $5 million ($6 million DEI minus $1 million deemed return). If $3 million of the DEI is foreign-derived (FDDEI), the foreign-derived ratio is 0.5 ($3 million FDDEI / $6 million DEI). The FDII is $2.5 million ($5 million DII x 0.5 foreign-derived ratio). This process shows how gross receipts, deductions, and the deemed return are used in the FDII calculation. Additional examples can further clarify allocation methods and compliance steps.

Deduction eligible income and foreign-derived deduction eligible income are based on income earned from foreign sources, which directly affects the amount of tax the corporation must pay (pay tax) under FDII rules.

When providing services or selling to foreign persons or related parties, both service and providing services can qualify for FDII if the services are provided to foreign persons or related parties outside the United States. Proper documentation is essential for these transactions.

For related party transactions, special rules apply. Sales or services to a related party may only qualify for FDII if the property is ultimately sold to an unrelated foreign party for foreign use, or if the service is provided to a foreign person. Understanding the impact of related parties and related party transactions is crucial for FDII qualification.

The operative section of the Internal Revenue Code, such as Section 250, and further guidance from the IRS may be needed to address complex allocation or calculation issues related to FDII.

Understanding FDII Tax Implications

The FDII deduction has significant tax implications for domestic corporations, including allowing eligible income to be taxed at a lower rate compared to standard corporate tax rates. This lower rate on foreign-derived intangible income can result in substantial tax savings and directly impacts tax planning strategies, as understanding prevailing tax rates is crucial for optimizing deductions and incentives.

Under the Tax Cuts and Jobs Act (TCJA), which was a major tax reform effort, for taxable years prior to January 1, 2026, a U.S. corporation is allowed a 37.5% deduction on the foreign-derived intangible income (“FDII”) amount included in income, effectively reducing the tax rate on FDII to 13.125%, compared to the general 21% corporate tax rate. This favorable tax treatment incentivizes companies to create and store their intellectual property (IP) on U.S. soil and benefit from lower taxes when exporting that IP to foreign markets.

The 2025 One Big Beautiful Bill has adjusted this phase-down, reducing the deduction for FDII to 33.34% for taxable years beginning after December 31, 2025, thereby increasing the effective tax rate on FDII to 14%. Additionally, the Bill renamed FDII as “foreign-derived deduction eligible income” (“FDDEI”), reflecting the evolving terminology in tax law.

The FDII deduction applies to a broad range of export activities, including sales of tangible and intangible assets as well as a wide array of services provided to foreign persons. Domestic corporations must carefully consider the tax implications of the FDII deduction, including its impact on their overall tax liability, and ensure compliance with all relevant provisions of the Internal Revenue Code and related regulations.

This includes considering other provisions such as GILTI and Sec. 861, and understanding the operative section of the Code that governs expense allocation and FDII calculations. The FDII rules offer domestic companies holding IP a valuable opportunity to maximize export revenue while minimizing tax liability, but awareness of the scheduled changes and new terminology is essential for effective tax planning and strategy.

When evaluating the impact on international operations, it is important to consider foreign income and the specific rules that apply to foreign jurisdictions. The amount of income earned from foreign sources will affect the amount of tax a corporation must pay (pay tax) under these provisions. Additionally, understanding the rules for related parties and related party transactions is critical, as sales or services involving related parties may have different qualification requirements for FDII benefits.

5 Actionable Ways to Maximize Your FDII Deduction

Business owners can take several practical steps to maximize the benefits of the Foreign Derived Intangible Income (FDII) deduction. Here are five actionable strategies to consider:

Optimize Qualified Business Asset Investment (QBAI): Carefully manage and utilize your depreciable tangible property to influence the deemed tangible income return. Efficient asset use and accurate valuation of tangible assets can increase the deemed intangible income, enhancing your FDII deduction.

Maximize Deduction Eligible Income (DEI): Ensure proper classification of income and expenses to increase your deduction eligible income. Exclude non-qualifying income such as Subpart F income and foreign branch income, and allocate deductions precisely to prevent unnecessary reduction of DEI.

Maintain Thorough Documentation of Foreign-Derived Deduction Eligible Income (FDDEI): Keep detailed records of sales and services provided to foreign persons or related parties for foreign use. This documentation is crucial to substantiate your FDDEI claims and withstand IRS scrutiny.

Structure Related Party Transactions Strategically: Design related party sales and services so that property sold to related parties is ultimately sold to unrelated foreign persons for foreign use, or services are directly provided to foreign persons. This structuring helps ensure these transactions qualify for FDII benefits.

Stay Updated on Tax Law Changes and Compliance Requirements: Monitor legislative changes affecting the FDII deduction, including the scheduled reduction in deduction percentages after 2025. Staying informed allows you to plan proactively and maximize tax benefits within the current legal framework.

Implementing these strategies can help your business fully leverage the FDII deduction, reduce tax liability, and enhance competitiveness in foreign markets.

Benefits of Getting an Intangible Assets Valuation from AVGI Experts

Intangible assets can be challenging to quantify accurately, yet their value significantly impacts a business’s tax position, especially concerning foreign derived intangible income and related tax provisions like the GILTI tax. Getting a precise valuation from AVGI’s experts equips business owners with a clear understanding of their intangible assets’ worth, helping to avoid overpaying taxes and ensuring compliance with complex tax rules. This accurate valuation not only supports strategic tax planning but also enhances financial reporting and business growth strategy.

By partnering with AVGI, business owners gain access to specialized knowledge in valuing intangible assets, maximizing the benefits of the FDII deduction, and navigating the intricacies of international taxation. Don’t leave your intangible assets’ value to guesswork—contact AVGI today to secure an expert valuation that can optimize your tax outcomes and strengthen your business’s financial position.