Read Part 1: How to Value a Business: Understanding The Valuation Process

Recap: There are 3 stages to business valuations. During Stage 1, the appraiser selects the business valuation approaches and methods that are most applicable to the subject company and performs calculations to reach a preliminary valuation.

In Stage 2 of the business valuation, the appraiser adjusts the preliminary valuation to the appropriate level of value (LOV) consistent with the subject company they are valuating.

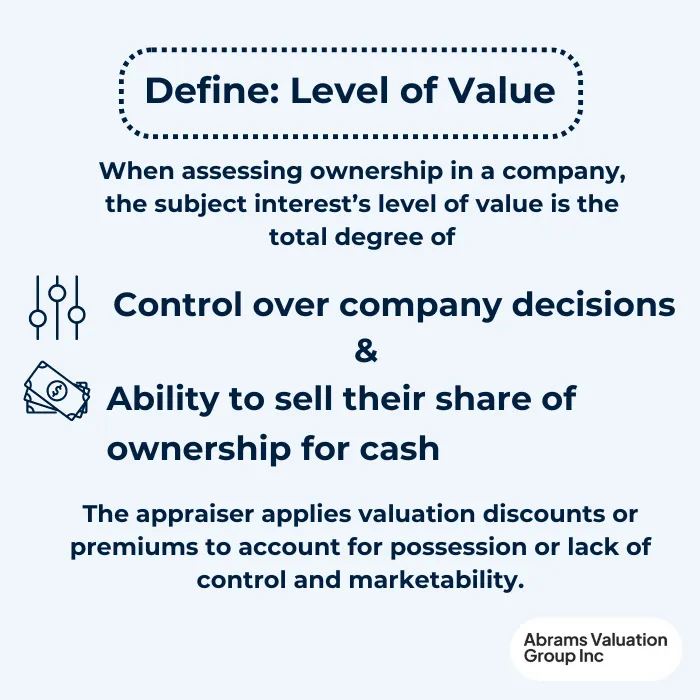

Levels of Value: Definition

Not all interests in a company are equal. When assessing ownership in a company, the appraiser takes into account several factors to determine the subject interest’s level of value:

- Control- how much control does the interest have over company cash flow and decisions?

- Marketability- how easy it is to sell the interest in the company for cash?

Interests with both control and marketability (i.e. the interest owns a majority number of shares in a publicly traded company) have the highest level of value.

Interests that have control but lack marketability (i.e. majority shares of a private company) or lack control but are easily marketable (i.e. minority shares of a public company) have a lower level of value.

Interests that lack both control and marketability have the lowest level of value.

Why Levels of Value Matter

When performing a preliminary valuation, the appraiser uses data from other Guideline Companies (GCs) for which data is more readily accessible. The GCs are similar to the subject interest in industry, size, etc. but may not have the same level of value.

In order to reach an accurate valuation for the subject interest, the appraiser must adjust the level of value from the preliminary valuation to match the subject interest’s level of value. Otherwise, the appraiser will be “valuing apples and applying the results to oranges.”

Valuation Adjustments with Valuation Discounts and Premiums

The appraiser may use one or more methods to adjust the preliminary values they calculated to the level of control and marketability consistent with the subject interest. As illustrated below, the appraiser can apply premiums to increase the LOV and discounts for lack of marketability (DLOM) or lack of control (DLOC) to decrease the LOV.

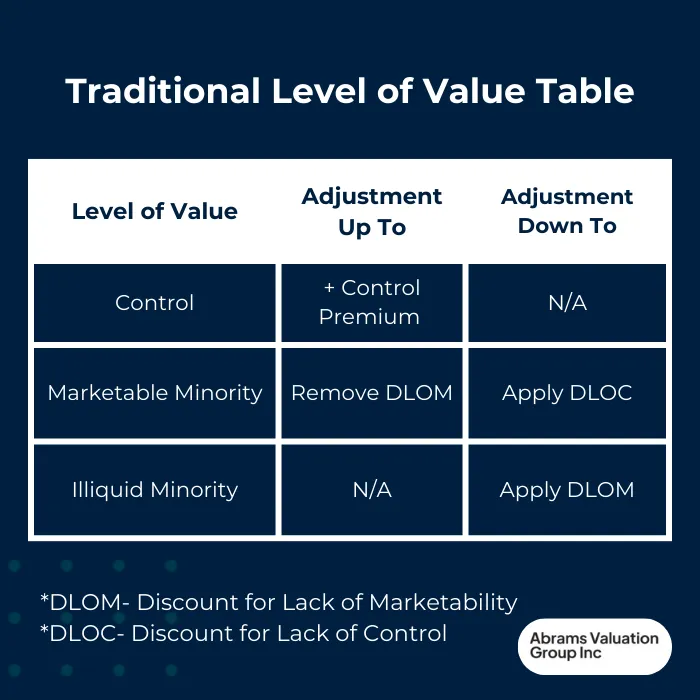

Traditional LOV Table

The traditional LOV chart acknowledges 3 levels of value:

- A control interest in a business. The control interest, as its name implies, controls cash flows in the business. The traditional LOV table does not differentiate between a control interest in a public firm from a private firm. The logic of this position is that the control interest controls cash flows and therefore should not suffer a DLOM. The logic is flawed, but there are practitioners who adhere to this LOV chart.

- A marketable minority interest. One level down from a control interest, a marketable minority interest is a typical interest that trades in publicly traded stocks. It is marketable, because the owner can call his or her broker, issue a sell order at the going market price, and receive cash in three days. It is a minority interest and suffers from lack of control, because the owner of 10 shares in a large company with millions of shares cannot call up the President to give him advice, criticism, or admonishment.

- Illiquid minority interest. The lowest level of value is a minority interest in a private firm. This interest has no control and is difficult, expensive, and time-consuming to sell. Thus it suffers from a lack of control and lack of marketability.

To move down from a control interest to a marketable minority interest, the appraiser would subtract DLOC. To move from a marketable minority interest down to an illiquid minority interest the appraiser would subtract DLOM. To move down from a control interest to an illiquid minority interest the appraiser would subtract DLOC and DLOM.

Valuation Adjustment Example

If the appraiser is using a Guideline Public Company Method and applies the average Price-Earnings ratio of the public Guideline Companies (GCs) to the subject company’s earnings, the resulting LOV would be a marketable minority level—consistent with the source data.

To value a control interest in the subject company, the appraiser adds a control premium.

To value a minority interest, if the subject company is publicly traded, then no LOV adjustment would be needed.

If it is privately owned, the appraiser would subtract a DLOM to adjust the LOV down to an illiquid minority interest.

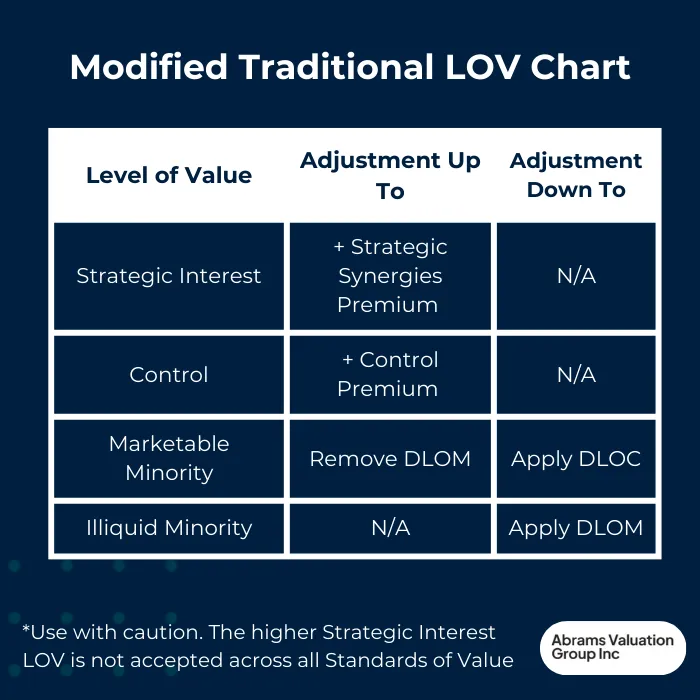

Modified Traditional LOV Chart

The modified traditional LOV chart adds a new row at the top for a Strategic Interest, i.e., for a buyer who pays an additional premium for synergies with the seller. One must be very careful with the strategic LOV, as its higher LOV is permissible in some standards of value but not others.

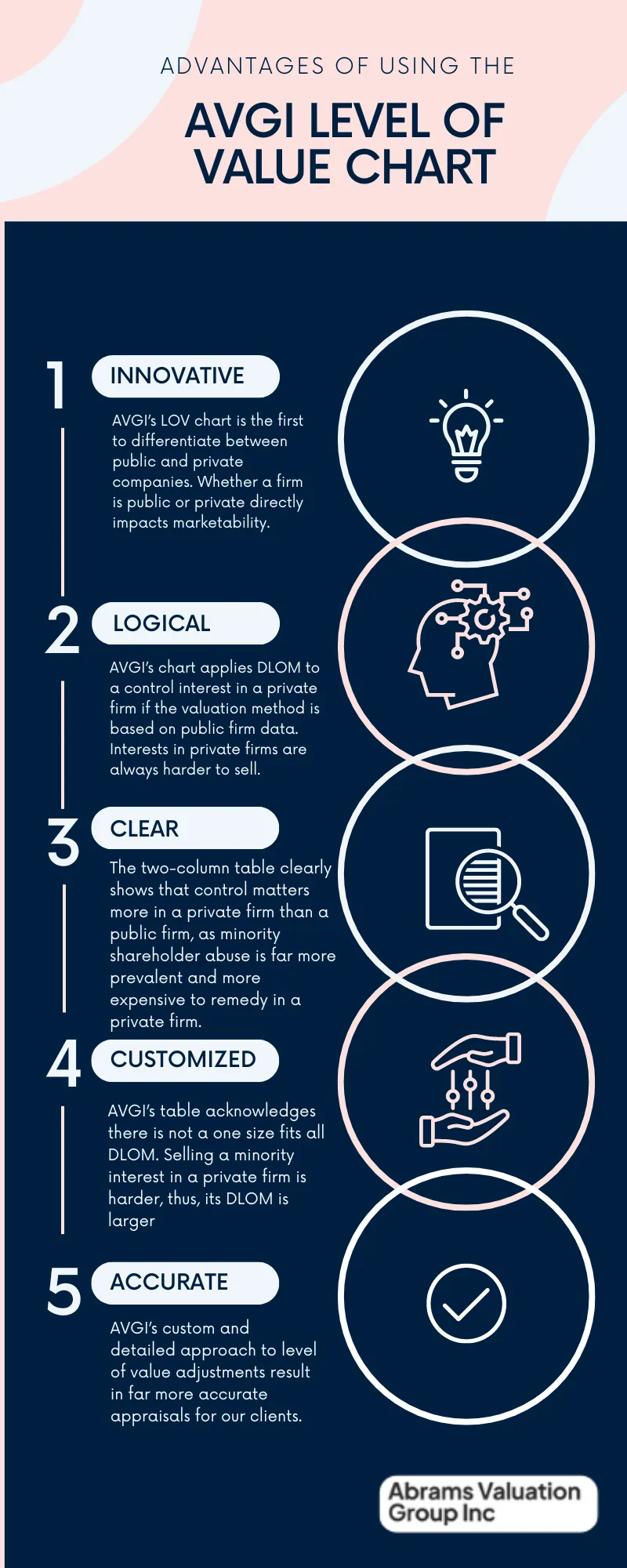

AVGI’s innovative LOV table: The logic behind it

The distinguishing feature of the traditional LOV table is that it is a one-column table that does not account for differences in Public vs Privately owned companies.

AVGI’s innovative LOV table is unique in that it first distinguishes between public and private firms, which affects marketability. AVGI’s approach streamlines the LOV adjustment process and enhances the valuation accuracy.

AVGI Level of Value Table

To adjust a public firm valuation to a private firm value, we would apply DLOM. To adjust from a private firm valuation to a public firm value, we would remove the DLOM embedded in the private firm valuation.

Benefits of the AVGI LOV chart

There are three important advantages of AVGI’S 2 column chart over the traditional LOV chart:

- In AVGI’s two-column LOV table we apply DLOM to the valuation of a control interest in a private firm if the valuation method is based on public firm data. This is a more logical position. If the owner of a private business has to sell quickly because of a bad medical diagnosis, it makes no sense that he or she is likely to receive an offer as if the firm were publicly held. Instead, the owner is most likely to lower the price in order to compensate the buyer for investing in an illiquid business interest.

- The two-column table clearly shows that control matters more in a private firm than a public firm, as minority shareholder abuse is far more prevalent and more expensive to remedy in a private firm.

- The two-column table clarifies that there is not necessarily only one DLOM, where one size fits all. One can generally sell a control interest in a private firm within one year of deciding to sell, but selling a minority interest in a private firm is usually more difficult and may take 2 to 30 years. Thus, DLOM is larger for minority interests than control interests. Additionally, it is greater for firms in which the minority shareholders have been poorly treated.

In short, the AVGI two-column table is a superior method for applying valuation premiums and discounts, and produces more accurate results more efficiently.

How are DLOM and DLOC Valuation discounts calculated?

The usual methods for calculating Discounts for Lack of Control and Marketability are:

- Economic Components Model Method (ECM). This is a hybrid method that combines the Market Approach for the delay-to-sale and monopsony power components with the Income Approach for the excess transactions cost components.

- Partnership Profiles Database Method (PPM). This method falls under the Market Approach and applies to valuing asset holding companies, especially those that hold real estate as its primary asset.

- Quantitative Marketability Discount Model (QMDM). This method is purely an Income Approach. One of its weaknesses is that there is no empirical basis for the estimates needed to employ this approach. Jay B. Abrams has published compelling empirical evidence of the failure of the QMDM to accurately predict restricted stock discounts.

At AVGI, our appraisers use the methods that result in the most accurate representation of the lack of marketability or control in the particular valuation assignment.

Conclusion: Level of Value Adjustments

Level of value adjustments are a critical component of the business valuation process. The appraiser determines the level of control and marketability of the subject interest and adjusts the preliminary valuation to match the same level of value. This adjustment is necessary to ensure an accurate valuation, as the use of data from other companies with different levels of value can lead to incorrect conclusions.

The appraiser uses valuation discounts and premiums to adjust the LOV to the appropriate level, and the modified traditional LOV chart offers a more comprehensive approach to this process. The business valuation process is complex, and the level of value adjustments is just one aspect of it. Still, it is crucial to consider these adjustments to arrive at a reliable and accurate valuation of a business.