How Does Liquidity in Business Affect Company Value?

Liquidity in terms of business value refers to how quickly and easily an asset can be converted into cash without significantly affecting its price; liquidity refers both to market liquidity, or the ease of buying and selling assets at stable prices, and accounting liquidity, which focuses on near-term business obligations. In business, liquidity is a critical measure because it indicates a company’s ability to meet its short-term financial obligations using liquid assets, and it is a key part of overall financial health.

More Liquidity: A business with higher liquidity (more readily available cash or cash-equivalent assets) is generally considered safer and more adaptable. Liquidity is important for covering payroll, inventory, rent, utilities, and taxes during cash flow slowdowns. High liquidity reduces the risk of insolvency, makes it easier to cover operational expenses, and allows a company to take advantage of investment opportunities. Investors and creditors often value liquidity highly, which can increase the business’s overall value and lower its borrowing costs.

Less Liquidity: A business with less liquidity may struggle to pay bills or debts on time, increasing financial risk. Too little liquidity can lead to missed payments, damaged credit, or even bankruptcy. While illiquid assets might appreciate over time, the inability to access cash quickly can lead to operational problems or missed opportunities. This higher risk can decrease the business’s value in the eyes of investors and lenders.

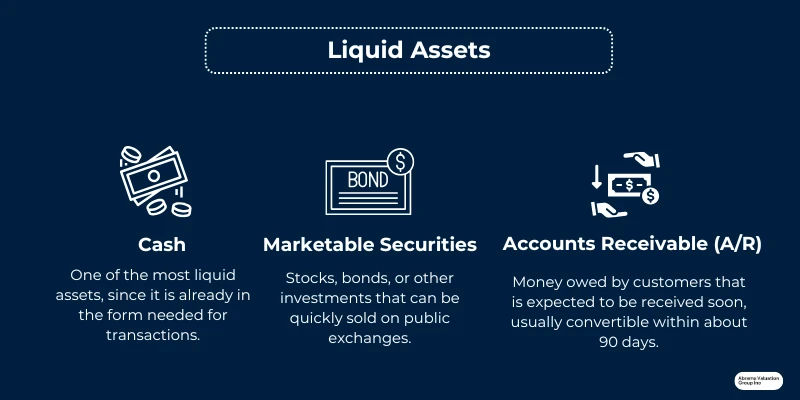

Examples of Liquid Assets

Cash: One of the most liquid assets, since it is already in the form needed for transactions, and cash liquidity refers to immediate funds available in checking and savings accounts.

Marketable Securities: Stocks, bonds, or other investments that can be quickly sold on public exchanges; liquid stocks are generally easier to sell because higher trading volume tends to support more stable pricing.

Accounts Receivable: Money owed by customers that is expected to be received soon, and some liquidity measures treat receivables and other short-term investments as quick assets convertible within about 90 days.

Example: A tech company holding $1 million in cash, cash equivalents, and publicly traded stocks can quickly pay suppliers or invest in new projects, boosting its flexibility and value.

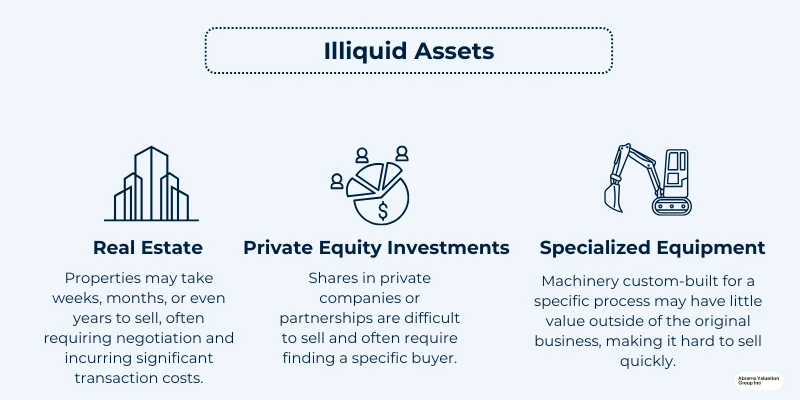

Examples of Illiquid Assets

Real Estate: Properties may take weeks, months, or even years to sell, often requiring negotiation and incurring significant transaction costs.

Private Equity Investments: Shares in private companies or partnerships are difficult to sell and often require finding a specific buyer. See our guide on selling a private company to a third party vs ESOP here.

Specialized Equipment: Machinery custom-built for a specific process may have little value outside of the original business, making it hard to sell quickly.

Example:

A manufacturing business owning $5 million in custom machinery and warehouses may have high asset value on paper, but if it needs cash urgently, selling these assets quickly could result in substantial losses or delays.

Liquid vs Illiquid Assets and Market Liquidity

Liquid assets can be turned into cash quickly and with minimal loss of value, so businesses can more easily convert assets when needed; they include cash, marketable securities, and other resources that can be sold fast, while market liquidity describes how easily assets trade at stable prices and accounting liquidity measures whether a company has enough assets to cover near-term obligations. In contrast, Illiquid assets require more time and may lose value if sold quickly (e.g., real estate, specialized equipment, and collectibles).

In summary, higher liquidity generally enhances a business’s value by reducing risk and increasing flexibility, whereas lower liquidity can decrease value due to higher risk and less operational agility, especially because liquidity supports the ability to cover short-term liabilities with available assets.

Valuation Discounts, Liquidity Ratios, and Discount for Lack of Marketability (DLOM)

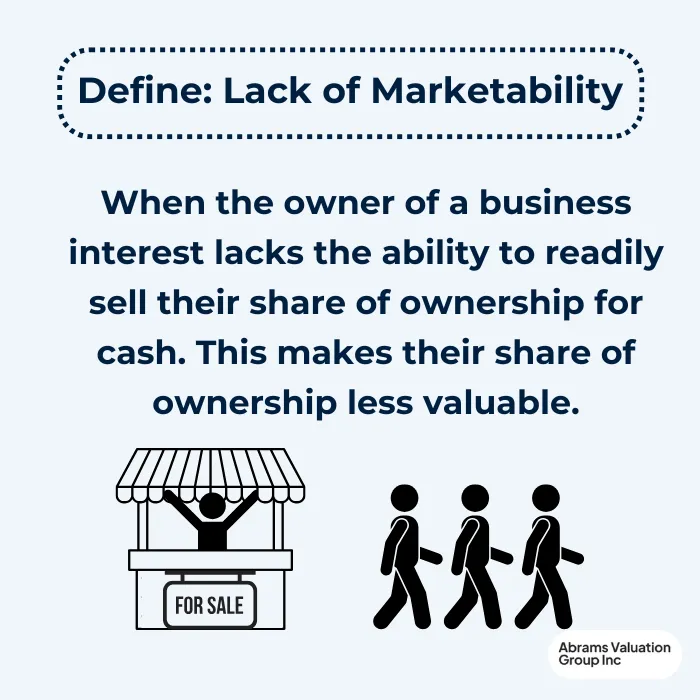

When assessing the value of a business, particularly a private company, it is important to consider valuation discounts. One of the most significant is the Discount for Lack of Marketability (DLOM). This discount reflects that some business interests cannot be easily sold or converted to cash, making them less attractive to potential buyers and investors.

Beyond marketability discounts, analysts also review a company’s liquidity and overall financial health on the balance sheet using standard financial ratios. They compare current assets with current liabilities to assess the company’s financial position, and ratio analysis often includes the Quick Ratio and Current Ratio to evaluate financial health.

Why Private Companies Face DLOM

Private companies usually do not have access to public markets, which means their shares cannot be quickly or easily sold. This lack of liquidity adds risk and inconvenience for potential buyers or investors, who may require a lower price to compensate for the difficulty of selling their ownership interest, and stronger liquidity can also help private companies secure loans or maintain credit lines on better terms because suppliers and lenders often offer cheaper financing to more liquid businesses. As a result, the appraised value of a private business is often discounted to reflect this lack of marketability.

Arranging bank loans or a business line of credit before cash is tight can provide an emergency cushion when marketability is limited.

Advantages of DLOM

Tax Purposes: Applying a DLOM can reduce the appraised value of a business for estate and gift tax purposes, which can result in lower tax liabilities when transferring ownership.

Divorce Settlements: A lower business valuation can reduce the financial obligation of the owner when dividing assets.

Shareholder Buyouts: DLOM can lower the required payout to minority shareholders during buyouts.

Succession Planning: Reduced appraised values can facilitate generational transfers by minimizing perceived value disputes and preserving flexibility through stronger liquidity planning.

Litigation or Dispute Resolution: In partnership dissolutions or shareholder disagreements, applying a DLOM can result in a lower valuation and potentially reduce the amount owed by the business or controlling shareholders.

Employee Stock Ownership Plan (ESOP) Transactions: Applying a DLOM can lower the cost of funding an ESOP, benefit company cash flow, and reduce the need for expensive emergency financing that often carries high interest rates and unfavorable terms.

Asset Protection: A lower business valuation due to DLOM can sometimes reduce the target value in lawsuits or creditor claims, offering a form of owner wealth protection.

Disadvantages of DLOM

Pricing the Business to Sell: A higher DLOM results in a lower appraised value, which can reduce the sale price and make it harder for an owner to realize the business’s full worth.

Raising Capital: Potential investors may be discouraged by a lower valuation, making it more difficult or expensive for the business to raise funds. Weak liquidity can also increase liquidity risk, while strong liquidity management may improve access to funding.

Securing Loans: Lenders often base loan terms and approval on business valuations. A high DLOM can lead to less favorable loan terms, higher interest rates, or even denial of credit. They also want to see enough cash or other liquid resources to cover current liabilities and short term debts.

Employee Equity Compensation: Lower business valuations can make equity-based compensation less appealing to current and prospective employees, impacting recruitment and retention.

Mergers and Acquisitions: In M&A negotiations, a high DLOM can weaken the company’s bargaining position or lead to less advantageous deal terms.

Public Perception and Partnerships: A persistently low valuation may affect the business’s reputation, making it less attractive for strategic partnerships or collaborations.

Insurance Claims and Settlements: In cases where business value is relevant to insurance claims (such as business interruption insurance), a lower valuation due to DLOM could result in smaller claim settlements.

Poorly managing liquidity can force emergency financing, while good planning includes cash buffers, accessible credit lines, backup business credit lines, and automatic sweep accounts to avoid operational disruptions.

Businesses can optimize liquidity by monitoring cash flow, comparing current assets with current liabilities and accounts payable, and refining inventory levels to avoid overstocking and free up cash; this also helps maintain a safety net during revenue dips, supply chain disruptions, or seasonal slowdowns.

Holding too much cash can also be inefficient, since idle funds may be better reinvested to generate profit.

In summary, while valuation discounts like DLOM can offer advantages in certain contexts—especially for tax planning—they can also reduce a business’s perceived value in situations where a higher valuation would be desirable.

Conclusion

Liquidity and marketability are two critical factors that drive business value—especially for private companies. While high liquidity tends to enhance business value and operational flexibility, low liquidity can lead to the application of significant valuation discounts such as the Discount for Lack of Marketability (DLOM). As discussed, DLOM can both benefit and hinder a business depending on the scenario: it may lower tax liabilities or settlement amounts, but it can also reduce sale prices, investor interest, and borrowing capacity.

Navigating these complexities requires a nuanced approach and an understanding of how valuation methods and discounts apply to your unique circumstances. Assessing liquidity in business should also include regular working capital tracking by reviewing assets, current liabilities, and comparing incoming cash with outgoing expenses to manage short-term debts and spot bottlenecks early.

Among the common liquidity ratios, the current ratio—also called the working capital ratio—is calculated by dividing current assets by current liabilities, and a result above 1 is generally favorable when evaluating short-term liabilities. The quick ratio, or acid-test ratio, excludes inventory and prepaid expenses and measures (cash + marketable securities + accounts receivable) against current liabilities. The cash ratio is the most conservative measure, using cash and cash equivalents relative to current liabilities to assess whether a company has sufficient liquid assets to cover short-term obligations.

If you’re looking to accurately assess your business’s value or understand the impact of liquidity and marketability on your company, the experts at AVGI can help. Contact AVGI today for professional business valuation consulting and discover how we can support your financial goals.