How Net Operating Loss Carryforward Rules Affect Tax Planning

Every business owner aspires to run a profitable and fulfilling enterprise. However, the realities of cashflow issues, unexpected expenses, and other financial troubles can mean that a business may be operating at a loss, rather than at a profit. Such a business is likely able to deduct the business losses from their taxes, up to the excess business loss limitations. But what happens when a business ends up with more deductions than taxable income? AVGI’s valuation experts break down the topic of net operating losses and how net operating loss carryforward rules affect tax planning for business owners.

What is a Net Operating Loss?

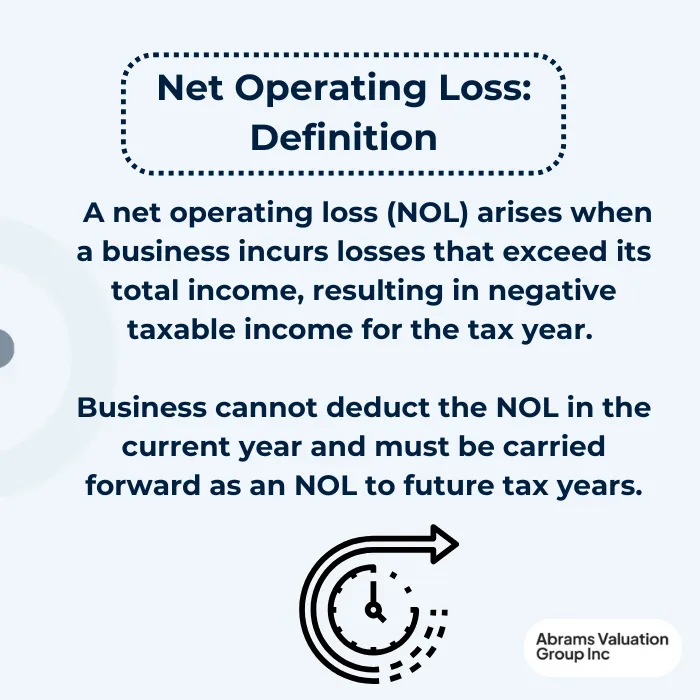

A net operating loss (NOL) occurs when a business’s deductions exceed its taxable income in a tax year, resulting in an operating loss that can be used to offset future taxable income. NOLs are an essential tool for business owners’ tax planning, as they allow businesses some tax relief to recover from a loss as well as balance out fluctuating taxable income across tax years.

The Internal Revenue Code (IRC) Section 172 governs NOL deductions, with different carryover and carryback rules applying to various tax years. There have been many changes in recent years to the legislation surrounding utilizing NOLs, so it’s important to note the year of the loss and the year that you wish to utilize the NOL. Currently, in 2025, NOLs have a few important characteristics, reflecting the changes in legislation:

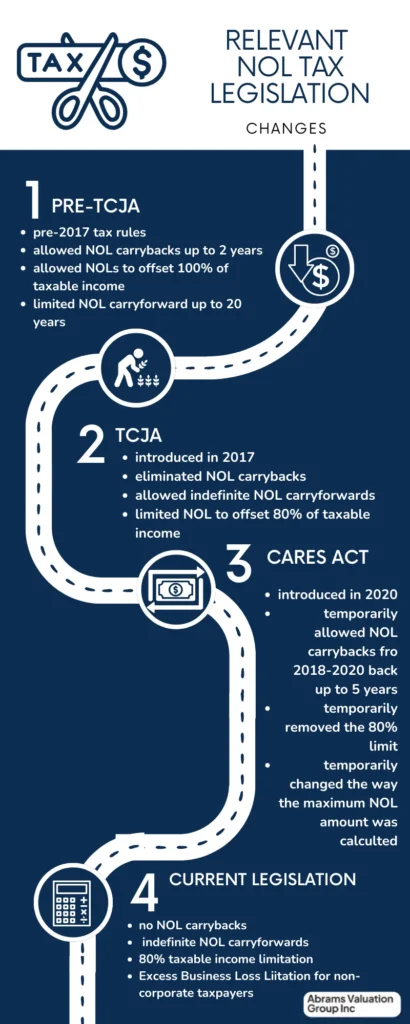

- Indefinite NOL Carryforward Rules: Businesses can now carry forward NOLs into future tax years indefinitely, allowing them to eventually realize the full amount of their net loss. This is in contrast to the older 20-year carryforward rule, which no longer applies.

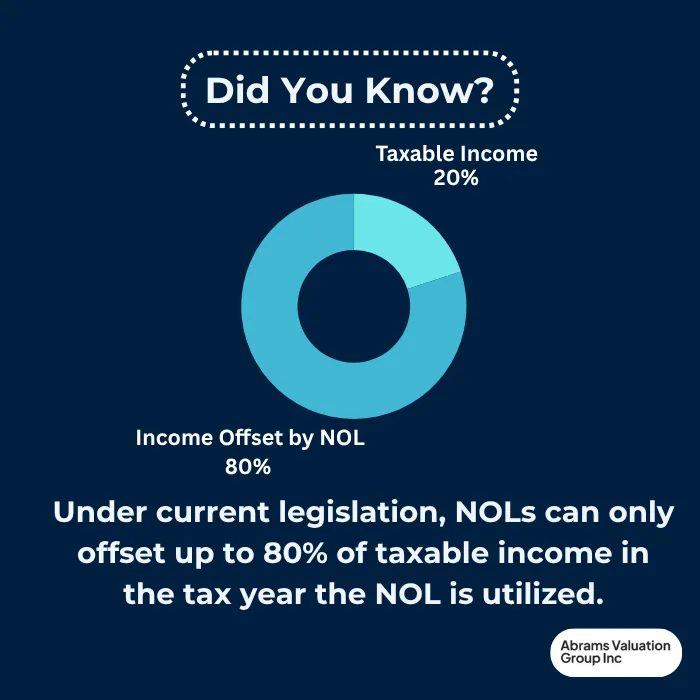

- 80% Limit: An NOL can only reduce up to 80% of the business’s taxable income for any tax year, even if the NOL exceeds 80%. The excess can be carried forward indefinitely, as we mentioned above.

- No NOL Carrybacks: NOLs can generally no longer be carried back to claim a refund for taxes paid in previous years. However, farming losses can claim a NOL carryback for up to 2 years retroactively.

- NOL Amount Limit: The NOL for post-2020 tax years is capped at:

- The value of pre-2018 NOLs carried to the current tax year (which can offset 100% of taxable income), plus

- The lesser of the two:

- NOLs carried to the current year from post-2017 tax years, or

- 80% of the excess taxable income remaining after applying pre-2018 NOLs. (Example below)

- Excess Business Loss Limitation: An additional rule for non-corporate taxpayers, including individuals, pass-through entities, estates, and trusts. Business losses exceeding the EBL threshold in tax years 2021-2028 are recorded as NOLs that can only be carried forward to future tax years.

All of these factors must be carefully considered in accurately calculating the NOL for the current tax year.

Steps to Calculate the NOL for the Current Year

Because of the many factors that impact calculating and using NOLs, we must calculate NOLs very methodically to avoid costly mistakes. Below we have broken down the steps to calculate the NOL for the current tax year:

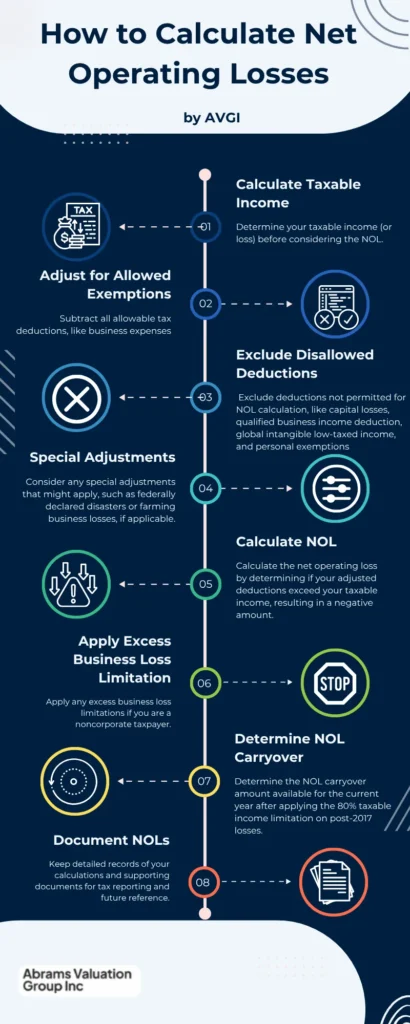

Determine your taxable income (or loss) before considering the NOL.

Identify all allowable tax deductions, including business expenses. Exclude deductions not permitted for NOL calculation, such as the qualified business income deduction, global intangible low-taxed income, and personal exemptions, and capital losses exceeding capital gains.

Subtract the total allowable deductions from your gross income to find the preliminary loss amount.

Consider any special adjustments that might apply, such as federally declared disasters or farming business losses, if applicable.

Calculate the net operating loss by determining if your adjusted deductions exceed your taxable income, resulting in a negative amount.

Apply any excess business loss limitations if you are a noncorporate taxpayer.

Determine the NOL carryover amount available for the current year after applying the 80% taxable income limitation on post-2017 losses.

Keep detailed records of your calculations and supporting documents for tax reporting and future reference.

It is important to note that the NOL deduction is determined by the tax law applicable in the year the NOL is deducted from taxes, not the loss year. Furthermore, tax years beginning in 2018-2020 have specific NOL rules, including a five-year carryback period. It is essential to factor in all of these elements when calculating the NOL deduction for a specific year, as each factor can significantly influence the bottom line NOL result.

Example of NOL Limit Calculation

To illustrate how the NOL Amount Limit works, consider the following example:

A business has pre-2018 NOL carryforwards of $100,000 and post-2017 NOL carryforwards of $150,000. The business’s taxable income before applying any NOL deduction is $200,000 for the current tax year.

Step 1: Apply the pre-2018 NOLs first

These old NOLs can offset 100% of taxable income.

Deduct $100,000 from $200,000 taxable income, leaving $100,000 taxable income remaining.

Step 2: Calculate 80% of the remaining taxable income after pre-2018 NOLs.

80% of $100,000 equals $80,000.

Step 3: Determine the lesser of:

- Post-2017 NOL carryforwards: $150,000

- 80% of remaining taxable income: $80,000

The lesser amount is $80,000.

Step 4: Total NOL deduction allowed for the current tax year:

- Pre-2018 NOLs: $100,000

- Plus the lesser of post-2017 NOLs or 80% limit: $80,000

- Total NOL deduction equals $180,000.

Step 5: Calculate taxable income after NOL deduction:

$200,000 minus $180,000 equals $20,000 taxable income subject to tax.

This example demonstrates how the 80% taxable income limitation applies to post-2017 NOL carryforwards, while pre-2018 NOLs can offset taxable income fully. The business cannot deduct the entire $150,000 of post-2017 NOLs this year due to the limitation, but the unused amount can be carried forward indefinitely to future tax years.

It’s essential for owners to have a financial advisor or qualified tax professional who can guide them on how to best leverage NOLs for their specific tax situation.

Federal NOL Rules

Federal NOL rules have evolved significantly over recent years, with changes introduced by the 2017 Tax Cuts and Jobs Act (TCJA), the 2020 CARES Act, and the 2022 Inflation Reduction Act. We’ve organized the most notable changes for taxpayers below:

- The TCJA limited NOL deductions to 80% of taxable income and eliminated carrybacks for most taxpayers

- The CARES Act temporarily allowed a five-year carryback for NOLs from taxable years 2018, 2019, and 2020 to offset financial damage from the Coronavirus pandemic.

- TCJA legislation allowed NOL carryforwards to be carried forward indefinitely, but subject them to the 80% taxable income limitation.

Tax professionals must consider these changes when advising clients on NOL planning and tax strategy.

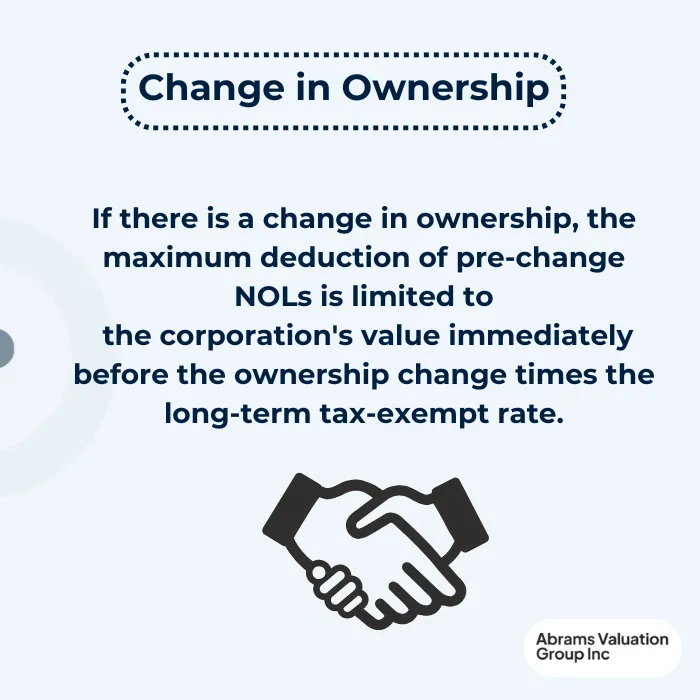

NOLs and Changes in Ownership

Corporations face specific limitations under Internal Revenue Code Section 382 when there is a significant change in ownership. This occurs when stock ownership increases by more than 50% among shareholders holding at least 5% of the stock over a three-year period.

Under these circumstances, the annual deduction of pre-change NOLs is limited to an amount equal to the corporation’s value immediately before the ownership change multiplied by the long-term tax-exempt rate.

For instance, if a corporation is valued at $2 million at the time of ownership change and the applicable long-term tax-exempt rate is 4%, the corporation can only use $80,000 of its pre-change NOLs each year to offset taxable income. This limitation helps prevent companies from acquiring loss corporations solely to exploit their tax attributes.

NOL Carryback and Carryforward Rules

In the past, businesses could carry back NOLs to claim refunds from taxes paid in previous tax years. This provided businesses with much-need cash flow relief following a period of financial strain. However, the 2017 TCJA legislation eliminated the ability for most businesses to carry back NOLs, which means that most businesses can no longer rely on immediate tax refunds to supplement their cash flow.

The CARES Act temporarily revived carryback rules for businesses affected by Coronavirus, but this provision has since expired. The current legislation through 2028 does not allow carryback for most businesses. However, there are a few exceptions, including farming losses, which have a two-year carryback period. Most businesses can only carry forward NOLs to offset future taxable income.

Understanding carryback and carryforward rules is crucial for effective tax planning and maximizing tax benefits.

Estates and Trusts

Estates and trusts are subject to similar NOL rules as individuals and corporations, with a few modifications for nonbusiness income and excess business loss limitations. The NOL calculation for estates and trusts involves subtracting allowable deductions from taxable income, considering qualified business income and capital gains. Like businesses, estates and trusts can carry forward NOLs indefinitely, but are subject to the 80% taxable income limitation. Tax planning for estates and trusts requires careful consideration of NOL rules and their impact on taxable income and tax liability. As with all tax matters, AVGI strongly recommends consulting a qualified financial professional before making any significant tax decisions.

Capital Gains Consideration

Capital gains are subject to special rules when calculating NOLs, with limitations on the amount of capital gains that can be offset by NOLs. The NOL calculation involves considering capital gains and qualified business income to determine the allowable deduction. Taxpayers must carefully consider the impact of capital gains on NOLs and tax liability, as well as the interaction with other tax provisions, such as the alternative minimum tax. Depending on the taxpayer’s situation, these tax liabilities and benefits can override or limite one another, so it is essential to understand their impact individually and collectively for effective tax planning and to maximize tax benefits.

Income Tax Implications

NOLs can significantly reduce future income tax liability, allowing businesses to offset future taxable income. For this reason, carrying forward NOLs is of great benefit to businesses that anticipate higher income in the future, like startups. However, the 80% taxable income limitation on NOL deductions limits the amount of taxable income that can be offset, making it essential to carefully consider NOL planning strategies. In addition, taxpayers must consider the interaction between NOLs and other tax provisions, such as the alternative minimum tax and excess business loss limitations to plan effectively and maximize benefits.

Itemized Deductions and NOLs

Itemized deductions, such as charitable contributions and medical expenses, can impact NOL calculations and tax liability. These deductions influence the determination of taxable income computed for the tax period, which in turn affects the net operating loss amount available for carryforward or carryback. It is important to understand that certain itemized deductions may be limited or adjusted when calculating the net operating loss under internal revenue code section provisions.

For instance, deductions related to federally declared disasters may be treated differently, allowing taxpayers to factor in losses that occurred due to such events in the NOL calculation. Additionally, nonbusiness deductions and capital losses exceeding capital gains are typically excluded from the NOL computation to ensure the loss reflects operating activities accurately.

Taxpayers using the accrual method of accounting must also carefully consider the timing of income and deductions, as this can affect the modified adjusted gross income and the resulting taxable income for the tax period. The interaction between itemized deductions and the alternative minimum tax further complicates the calculation, making it essential to consult a qualified tax adviser to navigate these rules effectively.

Deferred Tax Assets and NOLs

NOLs are considered deferred tax assets, which can be used to offset future taxable income and reduce tax liability. The valuation of deferred tax assets involves considering the likelihood of realizing the tax benefits, as well as the impact of other tax provisions, such as the alternative minimum tax. A company with NOLs that will likely be able to utilize them in the coming years may be valued more for this deferred tax asset. Therefore NOLs can be a valuable asset for a business.

State Tax Implications

State tax implications of NOLs vary, with some states following federal NOL rules and others having their own rules and limitations. Taxpayers must carefully consider the state tax implications of NOLs, as well as the interaction with federal NOL rules, to optimize tax benefits. Tax professionals must evaluate the impact of state tax rules on NOLs and tax liability to optimize tax benefits.

NOL Documentation

Accurate documentation of NOLs is essential for tax planning and compliance, including records of taxable income, deductions, and carrybacks and carryforwards. Taxpayers must maintain detailed records of NOLs, including calculations and supporting documentation, to support tax returns and audits. Understanding the documentation requirements for NOLs is crucial for effective tax planning and minimizing the risk of audits and penalties. Tax professionals must ensure that NOL documentation is precise and complete in order to calculate NOL deductions accurately and be prepared in case of an audit.

NOL Audits and Examinations

NOL audits and examinations can be complex and time-consuming, requiring careful consideration of NOL rules and documentation. Taxpayers must be prepared to support NOL calculations and documentation, including records of taxable income, deductions, and carrybacks and carryforwards. Tax professionals must be prepared to defend NOL calculations and documentation during audits and examinations to optimize tax benefits and minimize tax liability.

Navigating Net Operating Loss Carryforward Rules: In Conclusion

In summary, understanding net operating loss carryforward rules is crucial for effective tax planning, especially for businesses facing fluctuating income or losses. Recent legislative changes, including those from the Tax Cuts and Jobs Act and the CARES Act, have shaped how NOLs can be carried forward indefinitely but are limited to offsetting 80% of taxable income in any one tax period.

While carrybacks are generally no longer allowed except for specific cases like farming losses, careful calculation and documentation of NOLs can provide valuable tax relief by reducing future tax liability. If you want to ensure your business losses are accurately calculated—and potentially discover losses higher than originally thought—contact AVGI today. AVGI has helped numerous businesses maximize their tax benefits by expertly navigating net operating loss carryforward rules.