How Does Alt Min Tax Work?

Introduction to AMT

The alternative minimum tax (AMT) is a parallel tax system that requires taxpayers to calculate their tax liability twice – once under the regular income tax rules and once under the AMT rules. Taxpayers must pay the higher of the two calculated tax liabilities. The alt min tax ensures that high-income taxpayers are obligated to pay a minimum amount of tax. The AMT applies to individuals, estates, and trusts, and is calculated using a different set of tax rates and exemptions than the regular income tax.

The Corporate AMT (CAMT) applies to large corporations. Because this tax is designed to be difficult to avoid, the alternative minimum tax is an important tax planning consideration for high-income taxpayers. AVGI’s valuation experts explore the alt min tax along with key takeaways for high-income individuals.

Alternative Minimum Tax History and Purpose

The alternative minimum tax was created in 1969 to prevent wealthy taxpayers from avoiding income tax entirely by using excessive legal tax preferences and loopholes. The AMT was designed to ensure that taxpayers with high income pay a minimum amount of tax, regardless of the regular income tax deductions and credits they claim. Over time, the AMT has undergone several changes, including updated exemption amounts and phase-out thresholds.

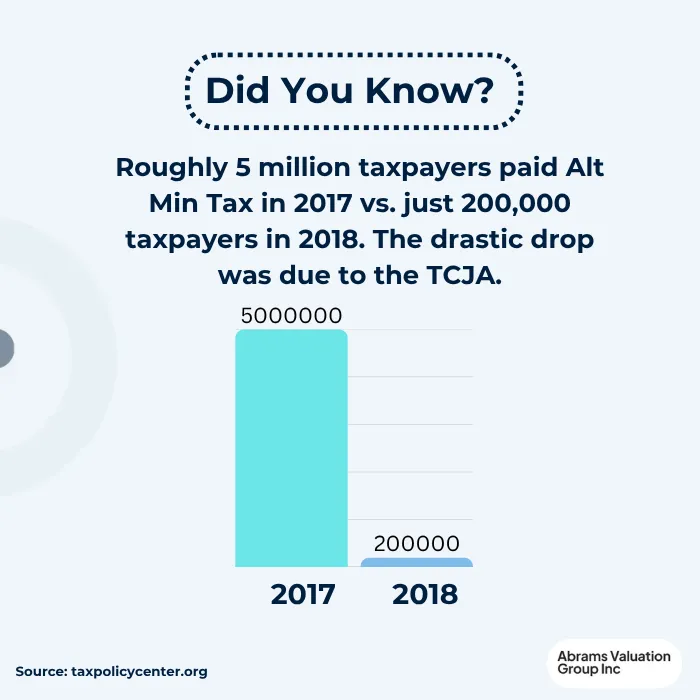

The 2017 Tax Cuts and Jobs Act (TCJA) introduced significant changes to the AMT, including increased exemption amounts and phase-out thresholds. However, until recently, AMT was not adjusted to the skyrocketing inflation levels, meaning that many middle-class taxpayers were stuck with an AMT obligation. The newly passed 2025 OBBB (One Big Beautiful Bill) finally adjusted the AMT for inflation, a huge tax relief for middle-class taxpayers in the coming tax years.

Alternative Minimum Tax Rates

The AMT tax rates are 26% and 28%, which apply to AMTI after subtracting the AMT exemption amount. The 26% rate applies to AMTI up to $239,100, and the 28% rate kicks in once AMTI reaches above $239,100. The AMT tax rates are an essential consideration in tax planning, as they can significantly impact tax liability.

AMT Rate | AMTI Single/Head of Household | AMTI Married Filing Jointly | AMTI Married Filing Separately |

26% | $88,101 to $239,100 | $88,101 to $239,100 | $68,501 to $119,550 |

28% | above $239,100 | above $239,100 | above $119,550 |

Alt Min Tax Exemptions

Alt Min Tax Exemptions

Alt Min Tax Exemptions

Alt Min Tax ExemptionsThe 2025 Alt Min Tax Exemptions are listed in the table:

Filing Status | Exemption Amount |

|---|---|

Single/Head of Household | $88,100 |

Married Filing Jointly | $137,000 |

Married Filing Separately | $68,650 |

The amount of income that can be exempted from AMT begins to phase out once a taxpayer’s alternative minimum taxable income (AMTI) reaches certain thresholds. Specifically, the exemption amount is reduced by 25 cents for every dollar of AMTI above these phaseout thresholds, effectively increasing the taxable income subject to the alternative minimum tax.

AMT Phaseout Thresholds 2025

Filing Status | Phaseout Threshold |

|---|---|

Single/Head of Household | $626,350 |

Married Filing Jointly | $1,252,700 |

Married Filing Separately | $626,350 |

For example, a married couple filing jointly with an AMTI of $1,300,000 would reduce their exemption amount by 25% of the excess $47,300 ($1,300,000 – $1,252,700), which equals $11,825. This means their exemption would be reduced to $125,175 ($137,000 – $11,825).

Once the exemption amount phases out completely, taxpayers must pay the alternative minimum tax on their entire AMTI without any exemption. This phaseout mechanism ensures that high-income taxpayers gradually lose the benefit of the AMT exemption as their income rises, increasing their overall tax liability.

Understanding how the AMT exemption begins to phase out is critical for taxpayers subject to the alternative minimum tax, as it directly affects the amount of income subject to the higher AMT tax rates. Taxpayers should carefully monitor their AMTI relative to these thresholds to anticipate changes in their tax liability and plan accordingly.

Additionally, taxpayers should be aware that certain deductions allowed under the regular tax system, such as state and local taxes (SALT) and miscellaneous itemized deductions, are disallowed or limited under AMT rules, which can further increase AMTI and accelerate exemption phaseout.

By factoring in these phaseout thresholds and deduction adjustments, taxpayers can more accurately calculate their potential AMT liability and consider strategies to minimize their exposure, such as timing income or deductions or utilizing available tax credits like the minimum tax credit for paid AMT in prior years.

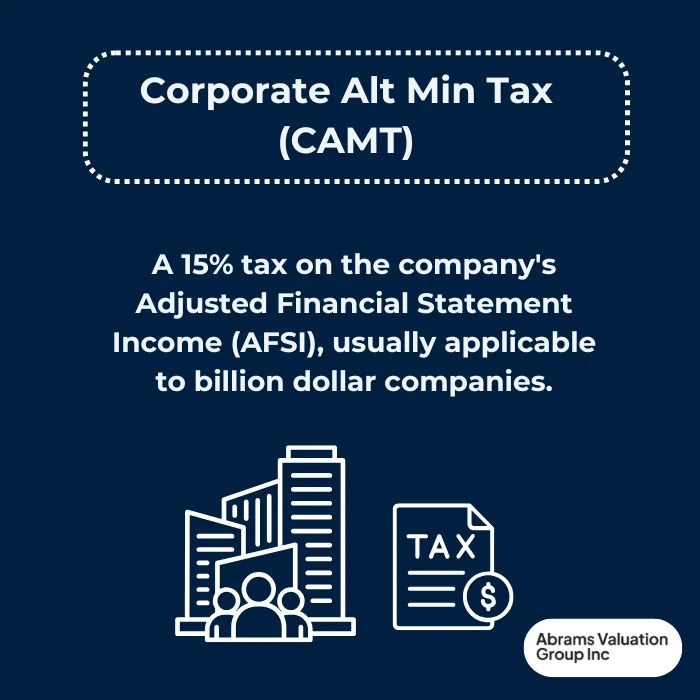

Corporate Alternative Minimum Tax (CAMT)

CAMT was introduced to the tax code by the 2022 Inflation Reduction Act. This imposes a 15% tax on the company’s Adjusted Financial Statement Income (AFSI). The CAMT generally applies only to very large corporations with average annual income over $1 billion.

Calculating AMT Liability

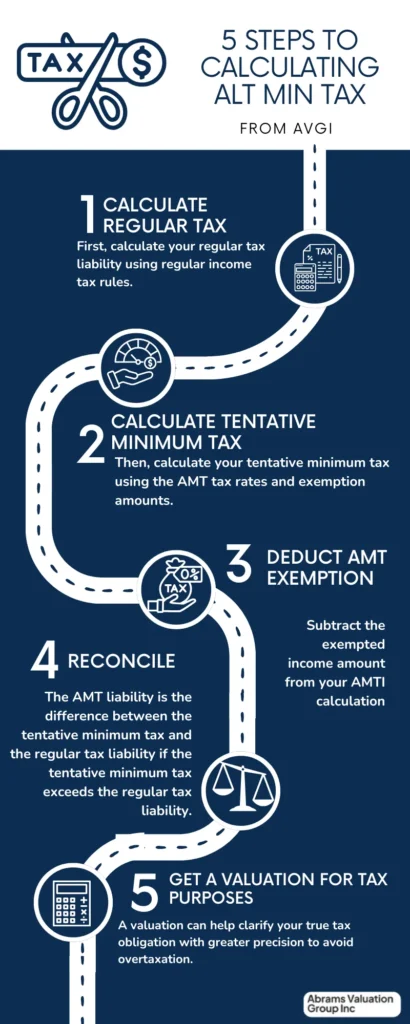

Here are straightforward steps to calculate whether you need to pay alt min tax, and if so, how much.

First, calculate your regular tax liability using regular income tax rules.

Then, calculate your tentative minimum tax using the AMT tax rates and exemption amounts.

Subtract the exempted income amount from your AMTI calculation

The AMT liability is the difference between the tentative minimum tax and the regular tax liability if the tentative minimum tax exceeds the regular tax liability.

Use tax preparation software or consult a tax professional to help with the AMT calculation.

Example of Calculating Alternative Minimum Tax

Suppose Jane is a single filer with a regular taxable income of $200,000. Under the regular income tax system, her tax liability is calculated as $40,000. To determine if she owes AMT, she must calculate her alternative minimum taxable income (AMTI) by adding back certain tax preferences and deductions disallowed under AMT rules, resulting in an AMTI of $210,000.

Next, Jane subtracts the 2025 AMT exemption amount for a single filer, which is $88,100, from her AMTI:

$210,000 – $88,100 = $121,900 taxable under AMT.

Jane then applies the AMT tax rates: 26% on the first $239,100 of AMTI after exemption, and 28% on any amount above that. Since $121,900 is less than $239,100, her tentative minimum tax is:

$121,900 × 26% = $31,694.

Jane compares this tentative minimum tax of $31,694 to her regular tax liability of $40,000. Since the tentative minimum tax is less, she does not owe any AMT.

Now, if Jane’s AMTI were higher, say $300,000, after subtracting the exemption, $211,900 would be subject to AMT tax rates. The calculation would be:

26% on $211,900 = $55,094

In this case, since $55,094 (tentative minimum tax) is greater than $40,000 (regular tax liability), Jane would owe AMT of $15,094 ($55,094 – $40,000).

This example illustrates how the alternative minimum tax ensures that taxpayers with certain tax benefits still pay a minimum level of tax.

Impact of Capital Gains

Capital gains can increase a taxpayer’s alternative minimum taxable income (AMTI), potentially reducing their AMT exemption amount. Long-term capital gains are taxed at a preferential rate under the regular income tax rules, but may be subject to the higher AMT tax rates. Taxpayers should consider the impact of capital gains on their AMT liability when planning their tax strategy.

Minimizing Tax Liability

Here are a few effective strategies to minimize your Alt Min Tax liability

Taxpayers can minimize their AMT liability by timing their income and deductions to avoid triggering the AMT.

Consider using tax credits, such as the minimum tax credit, to reduce their regular tax liability.

Consult a tax professional to develop a tax planning strategy that takes into account the AMT rules.

Minimize tax liability while ensuring compliance with the tax laws and regulations.

Conclusion

Understanding the alternative minimum tax (AMT) is crucial for high-income taxpayers to ensure compliance and optimize their tax liability. The AMT serves as a safeguard to guarantee that taxpayers with significant deductions and tax preferences pay a minimum level of tax. With its unique calculation method, exemption amounts, and tax rates, navigating AMT can be complex, especially when dealing with capital gains, incentive stock options, or asset sales. Proper planning and accurate valuation of intangible assets and business value are essential to effectively manage AMT exposure.

If you are facing a sale of assets or exercising stock options, AVGI’s valuation experts can help you accurately calculate intangible asset and business value for alt min tax purposes. Contact AVGI today to ensure your tax planning is precise and tailored to your unique financial situation.