What Is Capital Gains? Capital Gains Tax Explained: The Comprehensive Guide

What are Capital Gains?

If you’re in the world of business and investments, you’ve likely heard of capital gains tax. But what are capital gains exactly, and how is this tax different than other taxes? AVGI presents the topic of capital gain tax explained in simple terms. Read on to learn what capital gains are, how they affect your business and investments, tax implications, and how a capital gains valuation can help clarify your precise CGT obligation.

Capital Gains Meaning

A capital gain is the profit made from selling an investment, such as stocks, bonds, mutual funds, or real estate. Capital gains are taxed either as ordinary income or at a lower rate than regular income, depending on how long the investment was held. In contrast, a capital loss is a loss made from selling an investment, which can be used to offset capital gains for tax purposes.

How Capital Gains Tax Works (CGT)

Calculating Capital Gains Tax Liability

To calculate the capital gains or losses on selling an investment, we must begin with the cost basis or the original price for which you purchased it. Then, we subtract the original price from the price at which you sold the investment.

- If the result is positive, you sold the investment at a capital gain and now owe capital gains taxes on that sale.

- If the result is negative, then you sold the investment at a capital loss, and no CGT is due. Furthermore, this capital loss can be used to offset your CGT obligation if you have other investment sales on which you are required to pay capital gains taxes.

When Capital Losses exceed Capital Gains

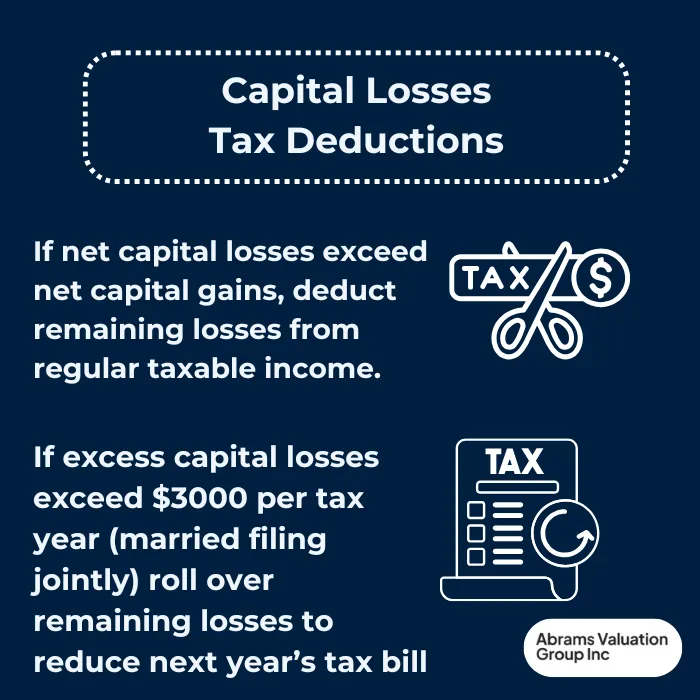

If total capital losses exceed total capital gains, the excess losses can be deducted from the investor’s tax return and used to reduce other taxable income, up to a maximum of $3,000 per tax year (for married filing jointly) or $1,500 per tax year (for married filing separately). If net capital losses exceed the annual maximum deduction, the investor can roll over the remaining losses to reduce the next (and subsequent) year’s tax bill.

Use Caution in Leveraging Capital Losses to Reduce Tax Bill

The Internal Revenue Service (IRS) instituted wash sale rules to prevent investors from exploiting potential tax deductions from losses (wash sales). Wash-sale rules prohibit investors from claiming a loss if they buy substantially identical investments within 30 days of the sale (at a loss). As with any tax-related matter, AVGI strongly encourages investors to consult a tax professional to discuss sound tax strategies and avoid triggering unnecessary IRS audits.

Capital Gains Tax Rates and Exceptions

Short Term Capital Gains vs Long Term Capital Gains

The length of time that you held the investment makes a difference in calculating the capital gains tax obligation upon selling it. If you had the investment for under a year, the gain or loss is considered a short-term capital gain (or loss) and is taxed as ordinary income (i.e. at the same income tax rate as your regular income tax bracket).

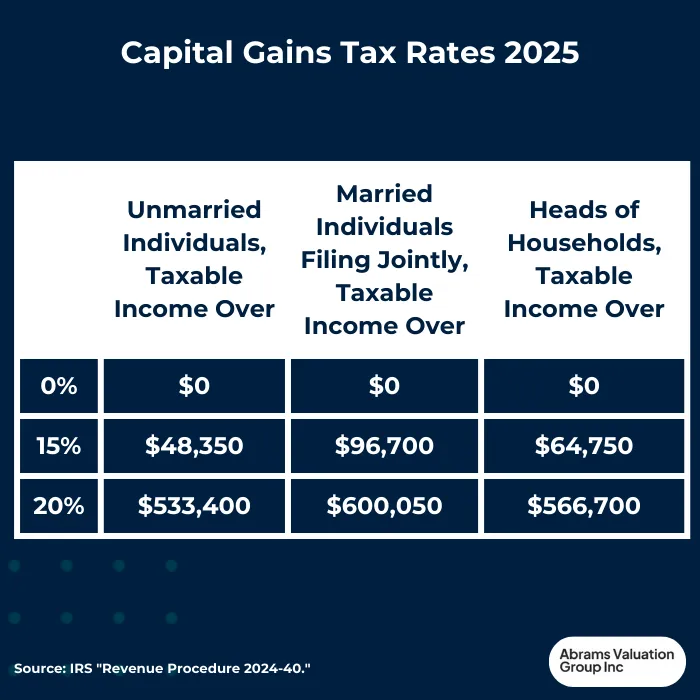

However, if you held an investment for a year or longer before selling it, the gain or loss is considered a long-term capital gain or loss and is taxed at a lower rate. The IRS sets the rates for capital gains, which can change over time.

Long-term capital gains tax rates are 0%, 15%, or 20%, depending on taxable income and filing status. See the chart below for 2025 Capital Gains Tax Rates:

Short-term capital gains tax rates are identical to ordinary income tax rates and will also mirror the taxpayer’s income tax bracket and filing status.

Certain tax-advantaged investment accounts, such as Roth IRAs and 529 plans, are exempt from capital gains tax or benefit from tax deferral. In a tax-exempt account, investments grow tax-free without being subject to capital gains tax, making these accounts a strategic part of many tax and estate plans.

Capital Gains Taxes and Retirement

Capital gains taxes can impact retirement savings and income. Investors can strategically contribute to tax-advantaged retirement savings accounts, such as 401(k) plans and IRAs, to reduce their capital gains tax liability. These tax-deferred accounts allow investments to grow tax-free until withdrawal. However, upon withdrawal, the investor will face taxation on the distributions.

Typically, these withdrawals are taxed as ordinary income rather than capital gains. This means the amount withdrawn is added to the investor’s taxable income for the year and taxed according to their income tax bracket at that time. It’s important to note that if withdrawals are made before reaching the age of 59½, they may incur an additional 10% early withdrawal penalty unless specific exceptions apply. Understanding the tax implications of these withdrawals is crucial for effective retirement planning and minimizing tax liabilities.

Net Investment Income Tax (NIIT) and Capital Gains

The Net Investment Income Tax (NIIT) is a flat 3.8% tax on net investment income, including capital gains, for taxpayers with adjusted gross income above certain thresholds. The NIIT is applied in addition to the capital gains tax rate, which means that taxpayers with high incomes may be subject to both the NIIT and capital gains tax.

Tax Implications of Selling Investments

Selling investments at a profit can trigger a taxable capital gain. The long-term capital gains tax rate is lower than ordinary income, with rates of 0%, 15%, and 20% based on their income thresholds and tax filing status. Investors should discuss tax savings strategies with a tax professional or financial advisor to reduce their capital gains tax bill, such as tax-loss harvesting and spreading the sale over multiple years.

Tax-loss Harvesting and Other Tax Minimizing Strategies

There are several strategies that you can leverage to reduce your tax bill. Let’s explore some of them now.

Tax-loss harvesting is a tax strategy that involves selling securities, stocks, and other investments at a loss to offset gains from other investments. As we mentioned earlier, investors can deduct up to $3,000 (depending on their status) of capital losses from their ordinary income, even rolling the deduction onto coming years’ tax bills if the investment losses exceed the annual limits. Be careful to adhere to wash sale rules to avoid undoing the potential benefits of this strategy.

Hold onto investments for more than a year, at least. This allows you to take advantage of the lower long term capital gains rate instead of having to pay taxes at the higher income tax rates if you sell the investment less than a year after acquiring it.

Spread the sale over multiple years, if possible. This can reduce the capital gains tax burden in a single year, particularly if you are selling multiple shares that have appreciated drastically.

Donate appreciated assets to beneficiaries, charities, or other nonprofits. This eliminates any direct capital gains as there is no sale made and defers any tax obligation to the recipient, if they should choose to sell it. Furthermore, you may be able to claim a further tax deduction for your charitable contribution. This can be an effective estate planning strategy you should discuss with your estate planning lawyer.

Obtain a formal valuation to accurately assess the value of the investment assets being sold. A thorough valuation approach can often reveal the capital gains on an investment sale to be overstated. Thus, a valuation can help clarify your capital gains tax obligation with greater precision to avoid overtaxation.

As always, AVGI stresses the importance of consulting with a tax advisor to qualify your investment strategy as lawful and avoid unwanted tax consequences such as costly fines or even jail time for tax evasion.

Capital Gains Tax: In Conclusion

Understanding the implications of capital gains tax is essential for investors aiming to make informed financial decisions. While capital gains taxes can add considerable strain, there are effective strategies to reduce this tax burden. If you are concerned about a significant capital gains tax bill, contact AVGI for a comprehensive capital gains valuation consultation. Our unwavering commitment to empirical precision can clarify your most accurate tax obligation and help you avoid over-taxation.