Confronting Capital Gains Tax on Business Sale: Key Insights & Strategies

Thinking of selling your business now or sometime in the future? Is a business sale an integral part of your exit plan and retirement strategy? It’s essential for business owners to factor in capital gains tax on business sales, as that single tax can drastically reduce your profits from the sale and drive up your overall tax bill. AVGI presents the key information for business owners to know about capital gains tax on the sale of a business as well as effective strategies that can reduce your tax obligation.

What Are Capital Assets and Capital Gains?

Capital assets include personal property, stocks, bonds, real estate, businesses, and business interests that can be bought or sold. Capital gains are the profits earned upon selling the capital asset for more than you bought it; those profits are subject to capital gains tax. On the flip side, capital losses occur if you sell the assets for less than the price you bought it. It’s essential to know the basis of the asset- the price at which you bought it in order to determine the capital gains or losses upon selling it.

Stepped-Up Basis for Certain Types of Assets

The IRS grants a stepped-up basis to assets that were gifted or inherited. That means the cost basis of the asset is adjusted to its value at the time it was gifted or the deceased’s date of death for an asset bequeathed as an inheritance. This step-up in basis is instrumental in saving on capital gains taxes, as it often significantly reduces the amount of taxes owed on inherited or gifted property. You can read more about how Capital Gains Tax works in our informative guide.

Tax Implications of Selling a Business

Capital gains tax is the primary tax concern for business owners selling their business. The profits from the sale are taxed as capital gains. Generally, income taxes do not apply to the profits from a business sale. The exact tax implications of a business sale will depend on the type of business or business interest being sold (S Corporation vs C corporation) as well as the structure of the sale. Small differences in how the sales contracts are worded can sometimes have a significant tax impact. It’s important for business owners to understand the tax implications of selling their business so they can structure deals to minimize taxes more effectively.

Capital Gains Tax on Sale of Business

In most cases, the owner must pay capital gains tax on the profits from selling their business or business interest. The capital gain is calculated as the difference between the sale price and the business basis, which equals the original cost of acquiring or founding the business plus the costs of improvements or maintenance.

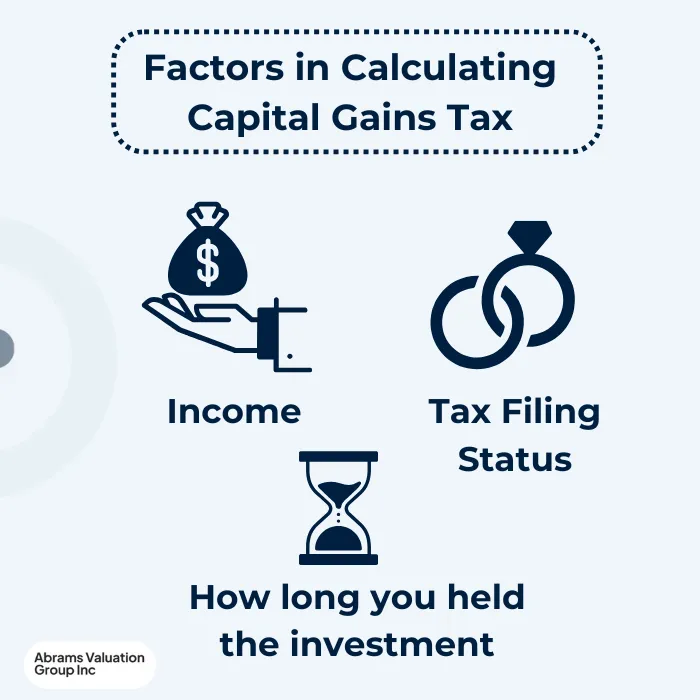

The capital gains tax rate you’ll pay will depend on:

- your income

- filing status

- how long you held the business or business interest before selling it

Short-term capital gains tax matches ordinary income tax rates. This rate is applied to businesses sold after being held for under 1 year. In contrast, long-term capital gains rates are typically lower than income tax rates, but can range from 0% to 15% to 20% depending on income. Long term capital gains apply to selling a business after holding it for a year or more. Taking advantage of the more favorable tax treatment for long term capital gains is a simple tax strategy that can have a significant impact, if it makes sense for your situation. Remember, you only have to pay taxes on the portion of the sale price above the business’s basis, not the entire amount.

Tax-Efficient Strategies for Business Sales

Owners can leverage several tax strategies when selling their business to reduce their capital gains tax bill. AVGI explores some of these strategies below:

Break down the business sale price and allocate it to individual capital assets. This clarifies the cost basis of each asset and makes it easier to claim lower capital gains per asset (by proving maintenance costs associated with individual assets.)

Additionally, the IRS taxes certain categories of assets, such as inventory and accounts receivable, with income tax rates, rather than the potentially lower long term capital gains tax rates. This itemized approach to laying out the business sale price allows for greater clarity and precision in calculating the capital gains tax owed.

Consider an installment sale where the buyer pays off the business acquisition over a set number of years. This can help spread the tax owed over time and minimize a huge tax bill all at once.

Use tax-loss harvesting to offset capital gains and reduce taxable income. Tax loss harvesting involves selling underperforming assets at a capital loss in order to offset any capital gains from the business sale or selling other high-performing investments. Use caution to adhere to wash sale rules to preserve the tax advantage of this strategy.

Utilize tax credits and incentives, such as investment credits and research credits, to reduce tax liability.

Opt for long-term capital gains due to the preferred tax treatment.

Consider selling to an ESOP rather than a third party investor. Although there are both advantages and disadvantages to this approach, AVGI has developed a formulaic way to calculate the breakeven point to help owners decide if this is a worthwhile option to pursue. Selling shares of a C corporation to an ESOP allows the owner to avoid personal capital gains tax entirely.

Special Tax Considerations

Installment Sales and Their Tax Implications

An installment sale allows you to sell your business in phases or installments to take advantage of tax advantages. This strategy can help you spread out your tax obligation and minimize your capital gains tax. You can set up an annual payment schedule with the buyer and limit it to a specific number of years. It’s important to note that only capital assets are eligible for installment sale treatment; ordinary income is not eligible.

1031 Exchanges

Take advantage of Section 1031 “like-kind” exchange to defer capital gains and reinvest in investment real estate. This strategy can help you defer payment of capital gains tax, particularly on sale of business real estate. The exchange must be done within a certain timeframe, and the properties must be “like-kind” in order to qualify.

Opportunity Zone Reinvestment and Its Tax Benefits

Business owners can defer capital gains tax by reinvesting capital gains from the sale of a business into Opportunity Zones. Opportunity Zones are economically distressed communities where investments are incentivized through tax breaks to spur economic development and job creation. To qualify for this tax break, any capital gains must be reinvested within 180 days of the sale. This strategy can help you defer payment of capital gains tax, potentially until 2026, and if the investment is held for at least 10 years, any additional gains earned within the Opportunity Zone can be permanently excluded from capital gains tax. This makes it an attractive option for business owners looking to support community development while also managing their tax liability effectively.

Restructuring the Business for Tax Purposes

Consider restructuring as either a pass-through business (such as LLC, partnership, or S corporation) or, conversely, restructuring to a C-corporation to take advantage of tax benefits. What is most advantageous will depend on your tax situation and the particular details of the business sale.

For example, switching to an S corporation can eliminate the double taxation on any appreciation after the date of the switch. On the other hand, restructuring as a C-corp would allow the owner to sell the business or a portion of it to an ESOP, eliminating personal capital gains tax. Tax-free reorganizations can defer tax due on the sale of a business. AVGI always advises owners to consult with a qualified tax professional to determine the most advantageous course of action from a tax perspective.

Charitable Giving and Tax Benefits

A charitable remainder trust (CRT) provides tax benefits while allowing the seller to receive income from the proceeds of a business sale. By transferring the business into a CRT before selling, the owner can avoid capital gains tax at the time of sale. The trust then sells the business, reinvests the proceeds, and provides the seller with regular income payments for a set period or for life. This and other charitable giving can be highly effective tax strategies to minimize capital gains tax on business sales.

Getting a Business Valuation Before Selling your Business

There are numerous reasons to get a valuation before selling your business. The two main reasons, however, are pricing your business correctly based on market factors to facilitate a sale at fair market value, and minimizing capital gains tax for the seller.

Capital Gains Tax on Business Sale: In Conclusion

It’s crucial for business owners to understand the tax implications of selling a business so they can minimize their tax liability. Consulting with a tax expert can help you develop a robust tax plan for avoiding or at least minimizing capital gains tax on a business sale. Proper planning can help business owners maximize their wealth and minimize tax liability. If you are contemplating selling your business, reach out to AVGI today for a capital gains tax consultation. You may owe less in capital gains taxes than you initially thought.