Goodwill in Business: Definition & Value for Business Valuation

Goodwill is all of the unseen factors that make certain businesses the unique successes that they are beyond their products or sales. But what exactly is included in goodwill in business? And how does that influence company value? AVGI discusses goodwill in depth so you can get all the answers.

What is Goodwill in Business?

Goodwill in business, often referred to as intangible asset goodwill, refers to the intangible asset that is created when one company purchases another company for more than the fair market value of its identifiable assets and liabilities. Goodwill represents the reputation, brand recognition, customer loyalty, and other intangible assets that are not separately recognized on the balance sheet. For example, if a company buys another company and pays more than the tangible assets like property, equipment, and inventory, the excess amount is recorded as goodwill.

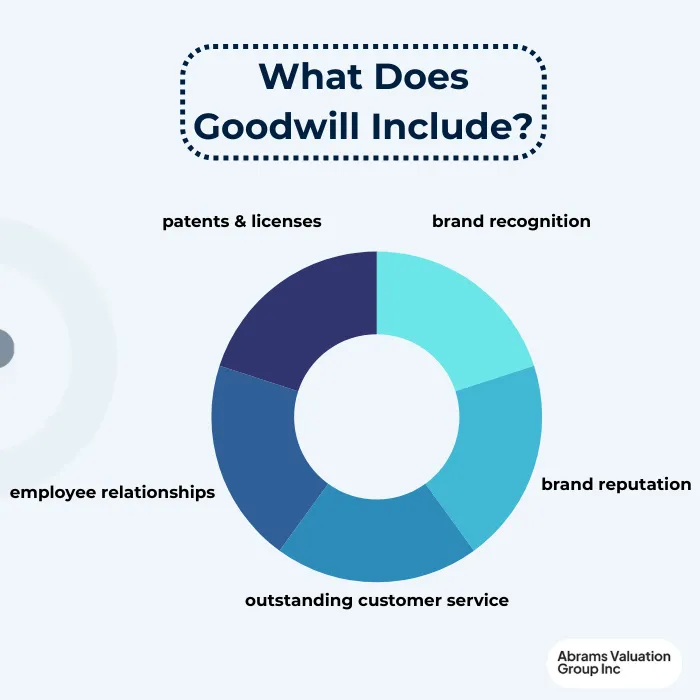

Intangible assets included in goodwill can encompass various elements, including:

- brand recognition

- brand reputation

- outstanding customer service

- customer relationships

- employee relationships

- proprietary technology

- patents & licenses

The combined value of these intangible assets contributes to the overall value of the acquired company and explains why one company would be willing to purchase another at an above-fair-market price. This combined intangible value is called goodwill and is recorded on the acquiring company’s balance sheet. Goodwill often arises during business acquisitions and significantly reflects a company’s value beyond its tangible assets.

Definition and Meaning

Goodwill is an intangible asset that represents the value of a company’s reputation, customer base, brand identity, and other intangible assets. It is created when a company acquires another company for a price higher than the fair market value of the target company’s net assets. This excess purchase price reflects the value of intangible elements that are not separately recognized on the balance sheet.

Goodwill is unique among intangible assets because it has an indefinite life, meaning it does not need to be amortized over time. However, it must be evaluated for impairment annually to ensure its fair value is accurately reflected. Only private companies have the option to amortize goodwill over a 10-year period, providing some flexibility in financial reporting.

Understanding Goodwill: Review & Reporting Requirements

Goodwill is an important concept in accounting that represents the premium a company pays for the acquisition of another business above the fair market value of its identifiable assets and net fair value of its liabilities. It reflects the value of the acquired business’s reputation, customer base, and other intangible assets.

Under Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS), companies are required to test for impairment of goodwill annually, or more frequently if there are indications of impairment. Testing for impairment involves comparing the carrying amount of the reporting unit’s goodwill with its fair value. If the carrying amount exceeds the fair value, the goodwill is considered impaired.

Upon impairment, the company must recognize a goodwill impairment loss on its income statement, reducing the goodwill to its implied fair value. The impairment loss reflects the decrease in the value of the acquired business since the acquisition, and it impacts the company’s profitability and financial position. Both GAAP and IFRS have specific guidelines for the disclosure and reporting of goodwill impairments in the financial statements to ensure transparency and comparability for investors and other stakeholders.

Negative Goodwill

Negative goodwill, also known as bargain purchase, occurs when a company acquires another business for less than the fair value of its identifiable net tangible assets. This often happens when the selling company is distressed or facing financial difficulties, leading the purchasing company to acquire the assets at a discount.

From a reporting perspective, negative goodwill is recognized as an extraordinary gain on the income statement. It is then allocated proportionately to the identifiable assets acquired based on their fair values, potentially impacting the carrying amounts of those assets on the balance sheet. The negative goodwill is counted as regular taxable income with no special tax treatment. If the acquiring company scores a significantly good deal with regard to negative goodwill, the potentially higher income tax is an important factor for them to consider before moving forward with the acquisition.

Overall, negative goodwill represents a unique scenario in business combinations and has implications for both financial reporting and tax considerations for the acquiring company.

How is Goodwill Calculated at Fair Market Value?

Calculating goodwill involves determining the premium paid for the acquisition of another business above the fair market value of its identifiable assets and liabilities. The formula to calculate goodwill is:

Goodwill = Purchase price of the target company – (Fair market value of assets – Fair market value of liabilities)

In this formula, the purchase price of the target company is reduced by the fair market value of its identifiable net assets (assets minus liabilities). The difference represents the goodwill, which reflects the intangible value of the acquired business, such as its reputation, customer base, and proprietary technology. The calculated goodwill is then recorded as an intangible asset on the company’s balance sheet, under long-term or non-current assets. This formula provides a quantitative measure of the premium paid for the acquired company and is an important metric for investors and analysts evaluating the financial implications of the acquisition.

There are several ways to calculate goodwill because it involves estimating future cash flows and other unknown factors at the time of acquisition. This can make it challenging for accountants to compare reported assets or net income between companies that have acquired other firms and those that have not.

This debate in how to calculate goodwill allows for a degree of flexibility. Depending on the circumstances of the company and acquisition, one way may be a more accurate representation of goodwill than another, which may have significant business valuation, tax, and other implications. As a result, calculating goodwill may involve judgment and estimates, leading to different approaches in different situations.

At Abrams Valuation Group, Inc., we specialize in calculating goodwill accurately and empirically. Our team understands the nuances and complexities involved in the valuation of intangible assets and can provide expert guidance tailored to your specific needs. Contact us for a free consultation with zero commitment to discuss how we can assist you in accurately calculating goodwill for your business.

Goodwill Impairments

Goodwill impairments refer to a decrease in the value of a company’s goodwill, which occurs when the fair market value of the goodwill drops below its book value. Goodwill impairments need to be tested for annually, as required by both US GAAP and IFRS Standards. Under these accounting standards, goodwill is classified as an intangible asset with an indefinite life and is not subject to amortization. Instead, it must be assessed for impairment at least once a year. It’s worth noting that private companies have the option to amortize goodwill over a 10-year period, instead of testing yearly for impairment.

Impairment Tests

An impairment test is a method used to evaluate whether the value of a company’s goodwill has declined. It is conducted using the market and/or income approaches. The market approach entails comparing the company’s market value with the carrying amount of its goodwill, while the income approach involves estimating the future cash flows attributable to the goodwill. The primary purpose of the impairment test is to ascertain whether the goodwill of a company has decreased since the previous year, serving as an indicator of potential underlying issues affecting the company’s value.

When a company’s assessment reveals that acquired net assets fall below the book value or if the amount of goodwill was overstated, then the company is required to impair or write down the value of the asset on the balance sheet.

The impairment expense is calculated as the difference between the current market value and the purchase price of the intangible asset. Consequently, the impairment results in a decrease in the goodwill account on the balance sheet. The expense is also recognized as a loss on the income statement, directly reducing the net income for the year. This, in turn, negatively affects earnings per share (EPS) and the company’s stock price.

When goodwill is impaired, it can have significant valuation and tax implications for the company. A goodwill impairment will reduce the overall value of the company, potentially impacting its ability to attract investment and obtain favorable financing terms. Furthermore, impaired goodwill may result in tax benefits as the company may be able to deduct the impairment loss from its taxable income, thereby lowering its tax liability. However, it’s important to note that the tax treatment of goodwill impairment can vary based on local tax regulations and accounting principles.

Goodwill vs. Other Intangible Assets

Goodwill differs from other intangible assets in several key aspects. Firstly, goodwill is unique in that it is considered to have an indefinite or infinite life, whereas other intangible assets such as licenses or patents have a finite useful life. This means that goodwill is not amortized over time, as it is not expected to diminish in value over time.

Additionally, goodwill is not capable of being bought or sold independently of the company to which it is attached. In contrast, licenses, patents, and other intangible assets can be bought, sold, or licensed to other entities separately from the business to which they are connected.

These distinctions make goodwill a distinct and somewhat unique intangible asset, as its value is intertwined with the overall value and performance of the company rather than being a separable and independently tradable asset.

Example of Goodwill

An excellent real-world example of goodwill was Google’s acquisition of Motorola Mobility in 2012. Google paid $12.5 billion for Motorola, but the fair value of its net assets was determined to be $5.5 billion, resulting in goodwill of $7 billion. This goodwill was recognized as a gain in Google’s financial statements.

How Is Goodwill Used in Investing?

Goodwill is used in investing to help determine the value of a company. When one company acquires another, the purchase price may exceed the fair market value of the acquired company’s identifiable assets and liabilities. This excess amount is recorded as goodwill on the acquiring company’s balance sheet. In investing, analysts consider goodwill as part of a company’s overall assets and assess its impact on the company’s valuation and financial performance.

How Does Goodwill Affect a Business’s Valuation?

Goodwill can have a significant impact on a business valuation. It represents the intangible assets of a business, such as its reputation, customer loyalty, and brand recognition. Goodwill can increase the overall value of a business, especially if it has a strong customer base and positive brand perception. However, it’s important to note that goodwill valuation can be complex, as it involves subjective assessments and various factors. In some cases, excessive goodwill can also lead to potential write-downs or impairments, impacting the business valuation negatively.

AVGI specializes in calculating goodwill value accurately and empirically. Contact us today for a free consultation of your company’s goodwill value.