Exit Strategies for Angel Investors: A Practical Guide from a Valuation and Exit Planning Perspective

As a business valuation professional and exit planning coach, I’ve seen firsthand how critical a well-defined exit strategy is for angel investors. This guide is designed for active and aspiring angel investors who want to maximize returns and minimize surprises when seeking liquidity from their early-stage investments.

Understanding Angel Investment Illiquidity

Angel investing is inherently illiquid. Unlike public stocks, there’s no daily market for your shares. Exits are rare, often unpredictable, and typically require years of patience. Recognizing this reality helps set reasonable expectations and underscores the importance of strategic planning.

Why Exit Strategy Matters for Angel Investors

Exiting is how you realize returns and recycle capital. Without an exit, even the most promising paper gains remain just that—on paper. Since most startups fail or stagnate, a thoughtful exit strategy helps you focus on deals with genuine liquidity prospects and manage your portfolio’s risk.

Angel investments typically take between 5 and 10 years to reach an exit event, reflecting the long-term nature and inherent illiquidity of investing in early-stage companies. Some investments may take even longer to provide returns, while others may never exit at all, underscoring the risk involved in early-stage investing.

Often, a seed-stage startup requires multiple rounds of funding and years of growth before attracting acquisition interest or preparing for an initial public offering (IPO). During this period, early investors often face uncertainty and must be patient, as the pathway to a profitable exit can be lengthy and unpredictable. Understanding these typical timeframes helps angel investors set realistic expectations and plan their portfolios accordingly, balancing the potential for high returns against the extended lock-up of their invested capital.

Common Exit Strategies:

- Acquisition (M&A)

- Initial Public Offering (IPO)

- Secondary market sale or tender offer

- Founder/company buyback

- Liquidation

Assessing Your Risk, Goals, and Constraints

Before investing, quantify your personal risk tolerance. For example:

- Risk Tolerance: Willing to lose up to $X of total angel capital.

- Target Return: Aim for a 3–5x multiple over 7 years.

- Capital Commitment: Maximum $Y locked up per deal or year.

These numbers clarify your investment boundaries and shape your exit planning.

Detailed Overview of Exit Strategies

1. M&A: Acquisition by Larger Companies

Acquisitions by larger companies are the most common and often preferred exit route for angel investors seeking liquidity. Potential acquirers typically include strategic buyers within the startup company’s industry or adjacent markets who see value in integrating the startup’s innovative product or technology into their existing offerings. For example, a fintech startup developing a novel payment solution might attract acquisition interest from established banks or payment processors looking to expand their digital capabilities.

Early identification of these strategic buyers allows investors to better understand market conditions and potential exit timing. Regular updates from the founders about acquisition interest and negotiations are essential, as they provide insight into deal terms and valuation expectations. Intellectual property (IP) is a critical factor during acquisitions; buyers conduct thorough due diligence to assess IP ownership, validity, and any potential risks. For instance, unclear patent assignments or unresolved licensing issues can delay or derail deals, reducing the startup’s attractiveness to acquirers.

Therefore, angel investors should actively flag any IP concerns early and encourage founders to maintain strong IP protection and documentation. Successful acquisitions not only provide a faster path to cash but also often offer a smoother transition for existing shareholders, including angel investors, who can realize returns as the startup’s technology or team becomes part of a larger, established company.

2. IPO and Public Offering Considerations

An initial public offering (IPO) represents a significant but relatively rare exit strategy for angel investors, offering the potential for substantial returns by allowing a company to issue shares to the public and gain access to public markets. However, preparing a startup for an IPO involves meeting rigorous milestones such as achieving consistent revenue scale, ensuring audit readiness, and establishing strong governance and compliance frameworks.

These requirements often mean that companies reaching IPO readiness are mature and operationally stable, with a median age of around 12 to 14 years before going public. After the IPO, angel investors typically face lockup periods of 6 to 12 months, during which they cannot sell their shares, delaying liquidity despite the public listing. Moreover, going public entails high regulatory costs and timing risks, including market volatility that can affect valuation and timing of the exit.

For example, companies like Airbnb took years to mature before going public, delivering high returns to early investors but requiring patience and strategic planning. While IPOs can provide a prestigious and potentially lucrative exit, angel investors should weigh these factors carefully and consider whether the company’s growth trajectory and market conditions support this path as the best exit strategy.

3. Secondary Market Sales and Tender Offers

Secondary market sales and tender offers present alternative exit options for angel investors seeking liquidity before a traditional exit event such as an acquisition or IPO. Secondary markets consist of private platforms that facilitate the buying and selling of shares in private companies, enabling investors to potentially cash out earlier than waiting for a full exit. However, these transactions often come with transfer restrictions set forth in the company’s bylaws or charters, which can limit the timing and conditions under which shares may be sold. Angel investors should carefully review these documents to understand any limitations.

Tender offers, on the other hand, are company-initiated opportunities that allow shareholders to sell a portion of their stake back to the company or to new investors, providing partial liquidity while the company remains private. Staying informed through regular management updates about upcoming tender offers is essential, as these events can offer valuable liquidity without requiring a full company sale.

For example, some startups have conducted tender offers to provide early employees and angel investors with cash before an acquisition, helping to maintain goodwill and reduce pressure on the cap table. While secondary sales and tender offers can provide useful exit options, they typically involve lower valuations compared to acquisitions or IPOs and may require negotiation and patience. Therefore, angel investors considering these routes should weigh the trade-offs between earlier liquidity and potential return, factoring in the company’s growth prospects and their own investment horizon.

4. Founder/Company Buybacks and Recaps

Founder or company buybacks, also known as recapitalizations, represent an important exit strategy for angel investors seeking liquidity without a full sale of the startup. In this scenario, the founders or the company itself repurchase shares from early investors, often to simplify the cap table, consolidate ownership, or meet requirements from new investors. This type of exit is more common in mature startups with stable cash flow, as buybacks typically involve significant sums and require careful valuation negotiations.

For example, a management team confident in the company’s long-term prospects might initiate a buyback to regain greater control or to reward early investors while maintaining strategic independence. From an angel investor’s perspective, it is crucial to review the company’s charter for any redemption or buyback clauses that permit or restrict such transactions. Valuation modeling plays a key role in determining a fair buyback price, balancing the interests of both the company and the investor.

Negotiations should also include clear payment terms and escrow arrangements to protect the investor’s interests and ensure smooth execution of the transaction. While buybacks may not offer the same immediate upside as acquisitions or IPOs, they provide a valuable alternative liquidity route, especially when market conditions or company strategy make other exit options less viable.

5. Liquidation, Shutdowns, and Asset Sales

Liquidation, shutdowns, and asset sales represent a less desirable but sometimes necessary exit strategy for angel investors when a startup fails to achieve sustainable growth or attract acquisition interest. In such scenarios, the company ceases operations and sells off its remaining assets to repay creditors and, if possible, return some capital to shareholders. Valuable assets may include intellectual property, domain names, proprietary technology, equipment, or customer lists.

For example, a software startup with patented technology might sell its patent portfolio to another company even if the business itself is shutting down. While liquidation typically yields lower returns than acquisitions or IPOs, it can provide a partial recovery of the investment, especially if the startup has built transferable assets. Angel investors should review the company’s cap table and liquidation preferences to understand the order and amount of payouts, as senior investors or secured creditors often receive priority.

Additionally, preparing thorough documentation and claims paperwork is crucial to ensure that investors can assert their rights during formal wind-down processes. Although liquidation is generally a last resort, understanding this exit path helps angel investors manage expectations and plan for downside scenarios in their portfolios.

Managing Cap Tables, Preferences, and Liquidity Events

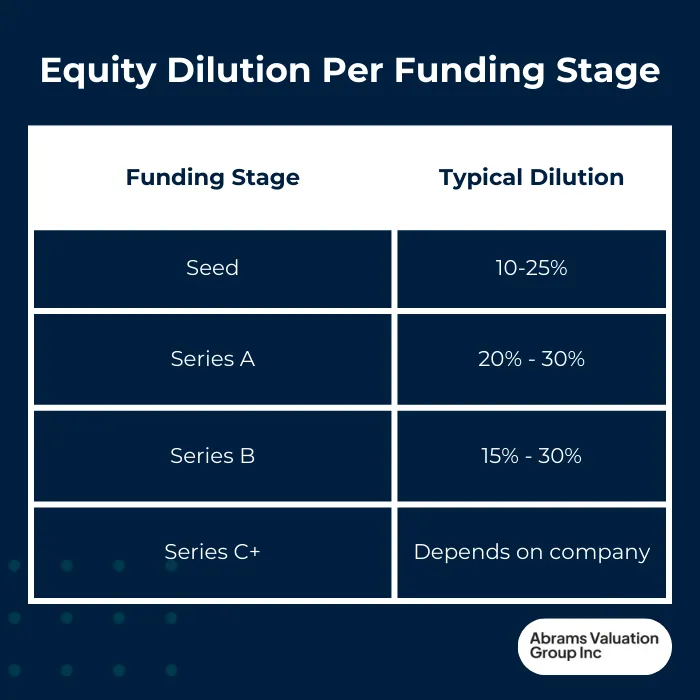

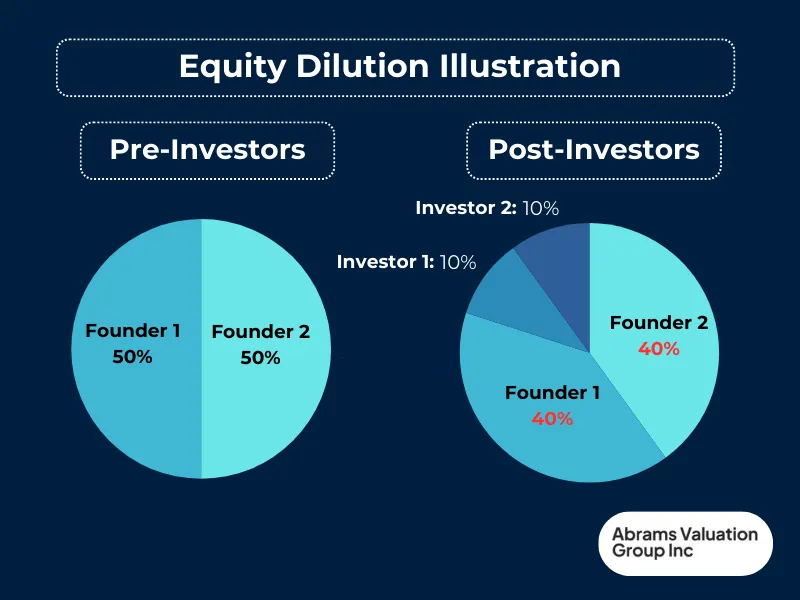

Effective management of cap tables, investor preferences, and liquidity events is essential for angel investors to optimize their exit strategies. Maintaining up-to-date cap table snapshots for each portfolio company allows investors to clearly understand their ownership percentage and how it may change over time due to dilution from subsequent funding rounds. This is critical because equity dilution directly impacts an investor’s potential returns at exit.

Liquidation preferences are equally important, as these provisions dictate the order and amount of payouts during exit events such as acquisitions or liquidations. For example, if preferred shareholders have a liquidation preference, common shareholders may receive little or no proceeds until those preferences are satisfied, which can affect the expected return for angel investors. Additionally, anti-dilution and conversion clauses can significantly influence share value by protecting investors from unfavorable financing terms or enabling conversion of preferred shares to common stock under certain conditions.

Pro rata rights are another vital aspect that impacts value for angels, granting angel investors the option to participate in future funding rounds to maintain their ownership stake and preserve their influence over exit outcomes. For instance, exercising pro rata rights in a high-growth startup’s Series B round can prevent dilution that would otherwise reduce an angel’s share of the exit proceeds. Overall, diligent monitoring and strategic management of these elements empower angel investors to anticipate how their stakes evolve, negotiate better terms, and align their investment decisions with realistic exit timelines, ultimately increasing the likelihood of achieving successful liquidity events.

Intellectual Property and Exit Value

Intellectual property (IP) plays a pivotal role in determining the exit value of a startup and, consequently, the returns for angel investors. Conducting a thorough IP audit early in the investment process is essential to confirm that all inventor assignments and employment agreements are properly documented and enforceable, ensuring clear ownership of the innovations. For example, missing or incomplete inventor assignments can create legal uncertainties that deter potential acquirers or complicate IPO preparations.

Registered patents, when properly assigned to the company, serve as valuable assets that can significantly enhance a startup’s valuation by protecting core technologies from competitors and providing a defensible market position. Additionally, understanding licensing arrangements and open-source software compliance is critical, as unresolved licensing issues or non-compliance with open-source licenses can introduce risks that reduce buyer confidence and lead to costly remediation or deal delays.

Encouraging founders to proactively address and resolve these IP issues before major funding rounds or exit discussions not only streamlines due diligence but also strengthens the company’s negotiating position. For instance, startups with well-managed IP portfolios have been able to command premium acquisition prices or attract strategic buyers interested in proprietary technology. Overall, a robust IP strategy and diligent management of intellectual property assets are integral to maximizing exit value and achieving successful liquidity events for angel investors.

Timing, Tax, and Legal Considerations

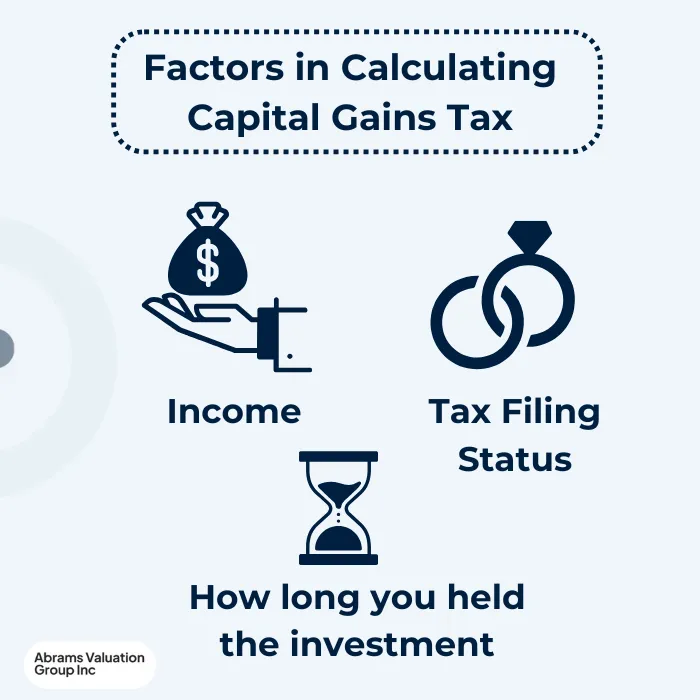

Timing and tax considerations are crucial elements in planning successful exits for angel investors. Capital gains taxes can significantly impact the net returns from an exit, so consulting with tax advisors early on is essential to understand how different exit strategies—such as acquisitions, IPOs, or secondary sales—may be taxed.

For example, holding shares for more than one year typically qualifies for long-term capital gains rates, which are often lower than short-term rates, making timing a key factor in maximizing after-tax proceeds. Additionally, investors should be aware of specific tax provisions, such as the Qualified Small Business Stock (QSBS) exemption, which can eliminate federal capital gains taxes if certain criteria are met, including holding the investment for more than 5 years. Planning exit timing around lockup periods or restricted sale windows is also vital, especially in IPO scenarios where shares are often subject to six- to twelve-month lockups that delay liquidity despite the public listing.

For secondary market transactions, preparing the necessary legal documentation in advance—such as transfer agreements and compliance with the company’s bylaws—is important to ensure smooth, timely share transfers. Overall, aligning exit timing with favorable tax treatment and legal readiness can materially improve the financial outcome for angel investors, turning paper gains into realized profits more efficiently.

Building an Exit-Aware Angel Portfolio

Building an exit-aware angel portfolio involves a strategic approach that balances diversification, liquidity planning, and active portfolio management. Diversification is key: by investing across different sectors and vintage years, angel investors can spread both timing and risk, reducing the impact of any single company’s delayed or failed exit. For example, including startups in fintech, healthtech, and consumer products launched in staggered years helps avoid a concentration of exit events all occurring simultaneously or none at all.

Maintaining capital reserves is equally important, as having available funds allows investors to participate in pro rata or follow-on rounds, preserving or increasing ownership in promising companies that show signs of exit potential. Without these reserves, investors risk dilution that can significantly reduce their share of future exit proceeds. Additionally, targeting a portion of deals with shorter expected exit timelines—such as later-stage startups or companies in rapidly consolidating markets—can provide earlier liquidity, balancing the longer waits typical of early-stage investments.

Actively monitoring the companies in your portfolio is essential to identify emerging exit opportunities, such as acquisition interest or tender offers, enabling investors to make timely decisions. Staying informed about industry trends and maintaining open communication with founders can reveal early signals of a potential sale or secondary market transaction. Together, these practices create a portfolio that is not only diversified but also strategically positioned to maximize the likelihood of successful and timely exits.

Negotiation and Communication with Founders

Effective negotiation and open communication with founders are crucial components of a successful exit strategy for angel investors. From the outset, it is important to request a written exit roadmap during your due diligence process, ensuring that both parties have a clear, documented understanding of potential exit scenarios and timelines. This roadmap should include projections of how various exit outcomes might impact the cap table and investor ownership stakes, enabling you to anticipate dilution and value changes over time.

Additionally, securing information rights—such as access to board materials and timely updates on major transactions—allows investors to stay informed about company developments that could affect exit timing and valuation. For example, receiving regular updates on acquisition interest or upcoming funding rounds can help you make proactive decisions about exercising pro rata rights or preparing for secondary sales.

Equally important is negotiating reasonable transfer rights for your shares, which can facilitate liquidity options like secondary market sales or tender offers without undue restrictions. For instance, having negotiated transferability provisions can enable you to sell a portion of your stake to other investors or the company itself, providing earlier access to cash when full exits are not yet feasible. By fostering transparent, ongoing dialogue with founders and embedding these protections in investment agreements, angel investors can better align expectations, reduce surprises, and position themselves to capitalize on exit opportunities as they arise.

Practical Checklist for Exit Planning

Create a one-page exit summary for every investment.

Include scenarios showing cap table impact at different exit values.

Update exit summaries after each funding round or major event.

Outline expected exit timelines and possible routes like acquisitions, IPOs, or buybacks.

Document key intellectual property assets and their status.

Track investor terms such as liquidation preferences and pro rata rights.

Consider tax implications, including QSBS benefits, for each exit strategy.

Maintain regular communication with founders about exit progress and opportunities.

Monitor portfolio diversification and keep capital reserves for follow-on investments.

Prepare necessary documentation to support secondary sales or tender offers.

Conclusion

Successful angel investing demands more than picking great founders—it requires proactive exit planning. By quantifying your risk, understanding common exit paths, and fostering candid founder dialogue, you can maximize your chances of achieving liquidity and strong returns. As valuation and exit planning professionals, we’ve seen that those who plan early and review often thrive in the long game of angel investing. Would you like to discuss your exit strategy options?