What Are Intangible Taxes? Understanding Their Valuation Impact

Intangible assets are non-physical properties, such as intellectual property, patents, trademarks, copyrights, and trade secrets, that have value and contribute to the overall value of a business. These intangible assets are subject to intangible tax. This class of assets are distinct from tangible assets, such as real estate and equipment. Intangible assets are often more valuable to businesses than tangible assets, but are harder to quantify their value.

Understanding intangible assets is crucial for navigating intangible taxes and ensuring accurate reporting and compliance with tax rules. AVGI experts break down intangible assets taxation so you can be informed and make strategic tax decisions.

Understanding Intangible Taxes

Intangible taxes typically apply to assets that do not have a physical form but hold significant value for businesses and individuals. These assets include intellectual property rights like patents, trademarks, copyrights, trade secrets, customer lists, and goodwill. Because these assets can generate revenue or future benefits, taxing authorities often impose intangible taxes to capture a portion of that value. These taxes are imposed by local governments, rather than the federal or state governments, which means that intangible tax rates can vary significantly by location.

Types of Investments Subject to Intangible Tax

Intangible taxes apply to a range of non-physical assets that produce or have the potential to produce revenue. Here are some other intangible property that may be subject to intangible taxes:

- Investment income from stocks, bonds, or other debt instruments

- Accounts receivable

- Mortgages

- Mutual funds and exchange-traded funds (ETFs)

- Insurance contracts

- Customer lists

- Intellectual property

- Patents

- Goodwill

- Future benefits (such as pension)

- Professional Licenses (such as medical practice)

- Other intangible assets

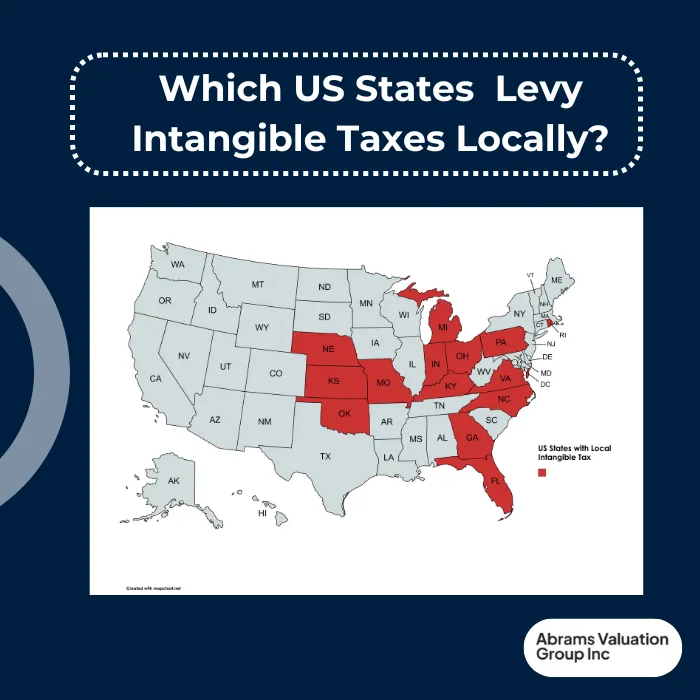

Intangible Local Tax Rates & Implications

Local tax rates and implications vary significantly by location, with different tax rates and rules applying to different areas. Only 14 US states impose intangible taxes on a local level, including Florida, Georgia, Indiana, Kansas, Kentucky, Michigan, Missouri, Nebraska, North Carolina, Ohio, Oklahoma, Pennsylvania, Rhode Island, and Virginia. Tax rates vary according to the county and city or township. For example, the lowest intangible tax rate in Kansas is for residents of Plum Township (0.125% rate) in Phillips County (.75% rate) who have a combined 0.875% intangible tax rate. Conversely, most other cities and townships are subject to the highest combined intangible tax rate of 3%, 0.75% county rate combined with 2.25% city/township rate.

Generally, the county treasurer’s office is responsible for collecting intangible taxes and issuing tax bills. Because intangible taxes vary widely by jurisdiction, it is important for corporations owning taxable property and individual taxpayers alike to stay informed about local tax codes and filing deadlines. Failure to comply with intangible tax regulations can result in penalties, interest charges, and complications such as restrictions on vehicle registration or other administrative actions.

How to Calculate Intangible Tax

The calculation of intangible taxes may depend on various factors, including the asset’s basis, income generated from the asset, and the tax year or fiscal year in which earnings are received. The asset’s basis is a key factor in determining taxable income and capital gains or losses when intangible assets are sold, and it directly affects the calculation of intangible taxes. The business’s or individual’s location is also important, as intangible tax is paid to the local government. However, nonresidents owning taxable property or receiving earnings from intangible property within the state must also file the appropriate tax returns.

Intangibles Taxes: Capitalization Requirement

Taxpayers should be aware of the capitalization requirement, which mandates that certain expenses related to acquiring or creating intangible assets be capitalized and amortized over time rather than immediately deducted. This requirement impacts how expenses related to intangible assets are reported for tax purposes and can affect the timing of tax liabilities.

Additionally, intangible taxes can apply to various types of intangible property, including receivables, mortgages, insurance contracts, and other financial interests. Understanding the scope of taxable intangible property is crucial for accurate tax billing and compliance.

Understanding intangible taxes fully, including the types of intangible assets subject to taxation, applicable tax rates, filing requirements, and the tax treatment of related expenses, empowers taxpayers to manage their tax liabilities effectively and ensure full compliance with all relevant tax rules.

Tax Treatment of Specific Assets

The tax treatment of specific assets, such as patents and trademarks, can vary depending on the location and type of asset. Capitalized costs, such as the cost of acquiring or creating an intangible asset, can affect the tax treatment of the asset. It’s important to have a qualified valuation expert determine the value of the specific asset, particularly if it is expected to be high in value. Accurately defining the value is key to accurately assessing and meeting the associated tax requirements to stay compliant.

Prepaid Expenses, Licenses, and Tax Implications

Prepaid expenses, such as insurance premiums, may be subject to intangible tax. In contrast, immediately deductible expenses, such as salaries and wages, are not subject to intangible tax. Other property that can be subject to this tax includes professional licenses, such as accountants and attorneys, and future benefits, such as pension benefits. However, the tax implications can vary depending on the type of expense and the location, so it’s necessary to consult with tax advisors who are up to date on your circumstances and the latest regulations.

Navigating Tax Complexity with Professional Guidance

Navigating tax complexity requires a deep understanding of intangible taxes and their implications. Taxpayers must ensure compliance with tax regulations, including filing requirements and payment deadlines. Understanding tax complexity is crucial for minimizing tax liability and ensuring compliance with tax regulations. Seeking professional advice, such as from a tax attorney or accountant, can help taxpayers navigate intangible taxes.

Getting an intangible asset valuation from a qualified valuation professional can significantly simplify and clarify the tax compliance process. AVGI has over 30 years of experience valuating unique and complex intangible assets, often for tax purposes. Contact us today to clarify your asset’s worth and your tax obligations to minimize your tax liability and ensure compliance with tax regulations.

Conclusion and Next Steps

In conclusion, understanding the complexities of intangible assets and intangible taxes is essential for both businesses and individuals aiming to ensure compliance with ever-evolving tax rules and regulations. Intangible assets—such as intellectual property, goodwill, trade secrets, and customer lists—can have a significant impact on a company’s value, tax liability, and overall financial health. Properly valuing and managing these intangible assets is crucial for maximizing tax benefits and avoiding costly mistakes.

To successfully navigate the world of intangible taxes, it’s highly recommended to consult with tax professionals who are well-versed in the latest tax code and regulations. These experts can help you determine the correct tax treatment for each intangible asset, ensure compliance with local and state tax requirements, and identify opportunities for tax savings. Staying informed about the capitalization requirement, capitalized costs, and the distinction between immediately deductible expenses and those that must be amortized is key to accurate reporting and minimizing your tax burden.

Here are some important steps and considerations when dealing with intangible assets and taxes:

Clearly understand how intangible assets are defined and classified for tax purposes, including the difference between tangible assets and intangible property.

Familiarize yourself with the various types of intangible taxes, such as intangibles tax, and how they are imposed at the local level.

Stay up-to-date on tax rules, including capitalization requirements, exceptions, and the specific tax treatment of different types of intangible property.

Ensure that all intangible assets are properly valued, especially when dealing with high-value intellectual property, patents, or goodwill.

Seek professional advice to ensure compliance with tax regulations and to uncover potential tax savings opportunities.

Ultimately, managing intangible assets and intangible taxes requires careful planning, ongoing education, and proactive compliance. By working with experienced professionals and keeping abreast of changes in tax laws—such as updates to the Kansas income tax return process—you can confidently navigate the complexities of intangible taxation, support state government revenue, and maximize the benefits for your business or personal finances.

By following these best practices and staying informed, you can ensure compliance, minimize your tax liability, and make the most of your intangible assets.