What Is Depreciation? How to Calculate it + Its Valuation Impact

Depreciation represents the decrease in value of tangible assets over their useful life, and acknowledges the negative impact of age and wear and tear on the value of the asset. Depreciation is a way of allocating the cost of a tangible asset over its useful life and matches that cost with the revenue that the asset generates. This spreads out the cost of the asset over the years the asset is in use.

Depreciation applies to fixed assets, including property, plant, and equipment, and is used to calculate the decrease in value of these assets over time.

Depreciation Expense

Depreciation expense is the amount of depreciation that is recorded on the income statement each year. It represents the decrease in value of the asset over its useful life. Depreciation expense is a non-cash expense, meaning that it does not affect the company’s cash flow. Rather, it is an accounting entry that matches the cost of the asset with the revenue it generates. The depreciation expense is calculated using one of the depreciation methods outlined below.

Calculating Depreciation

To calculate depreciation, you need to ascertain a few important pieces of information:

The cost of the asset, which is how much the company paid to acquire it.

The salvage value, which is the estimated residual value of the asset at the end of its useful life. This is the amount the company expects to recover when it disposes of the asset, either through sale or scrap. The salvage value is subtracted from the original cost of the asset to determine the depreciable cost.

The useful life of the asset, which is the estimated period over which the asset is expected to be productive and contribute to the business operations. This period can be expressed in years, units of production, or other relevant measures depending on the depreciation method used.

These values are used to determine the depreciable cost and annual depreciation expense for accurate financial reporting of the asset’s value over time.

The depreciable cost is then calculated as the cost of the asset – salvage value. This gives you the amount that depreciation affects. Then, the best depreciation method would be applied to the depreciable cost to determine the annual depreciation expense of the asset.

Accurately estimating the salvage value and useful life ensures that the depreciation expense matches the actual wear and tear or obsolescence of the asset, providing a realistic view of the company’s financial health.

3 Main Depreciation Methods

There are several depreciation methods to calculate the amount of depreciation. Here are a few of the most widely used methods, each with its own formula for calculating depreciation expense:

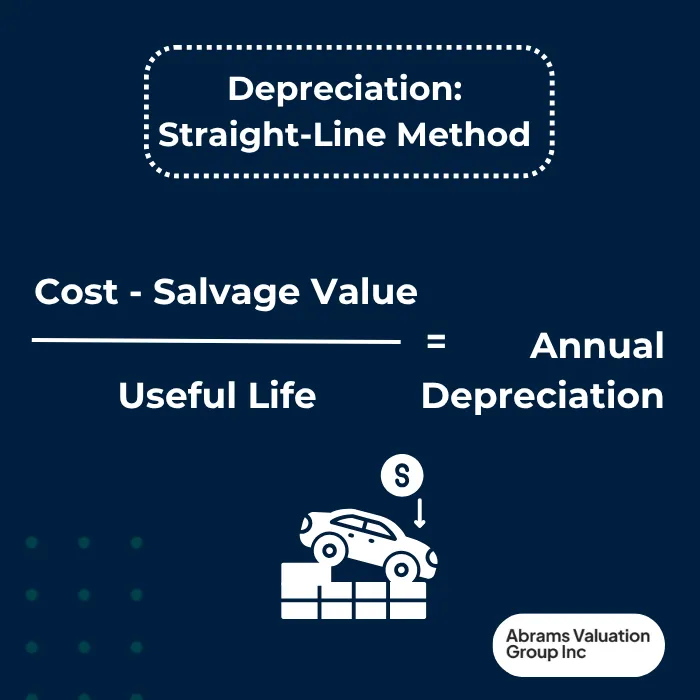

1. Straight-line method:

This is the most common method, where the depreciation expense is calculated as the cost of the asset minus the salvage value, divided by the useful life of the asset.

(Cost – Salvage Value) / Useful Life

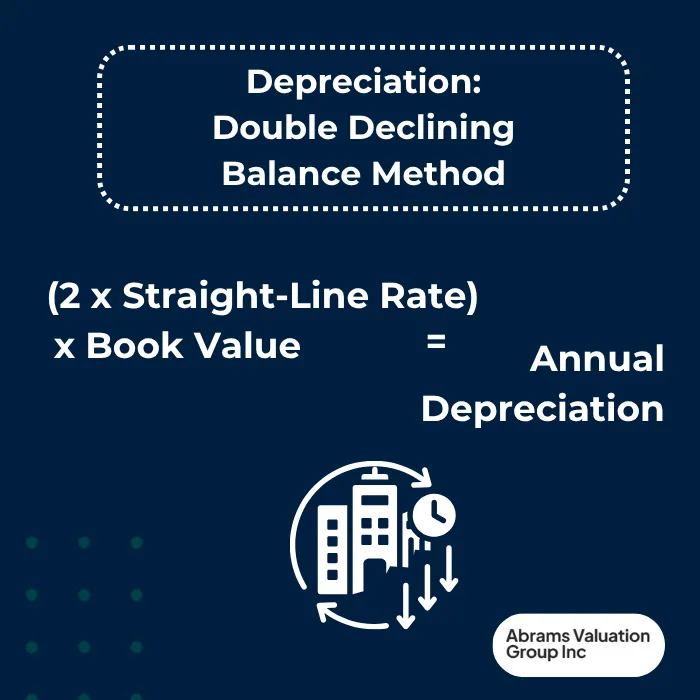

2. Declining Balance Method:

This method calculates depreciation expense as a percentage of the asset’s net book value. The declining balance method is best used to calculate depreciation expense for assets that lose their value quickly in the early years, such as technology equipment, which can quickly become obsolete in the face of fast-paced technological advancements.

The formula for calculating depreciation expense using the declining balance method is: (Depreciation Rate x Book Value)

A slight variation on this method is the double declining balance depreciation method which uses double the straight-line rate to calculate depreciation. (2 x Straight-Line Rate) x Book Value.

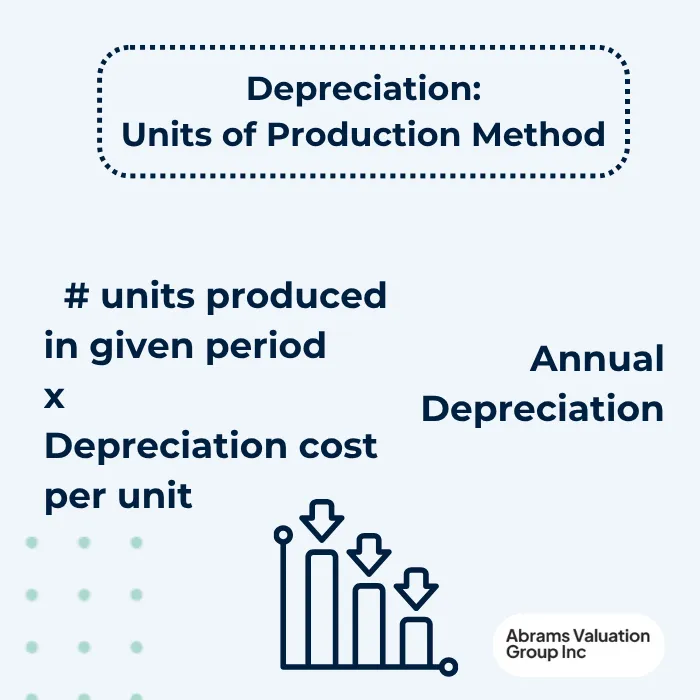

3. Units of Production Method:

This method calculates depreciation based on the actual usage or output of the asset rather than the passage of time. It is particularly useful for assets whose wear and tear depend more on how much they are used rather than how long they have been owned. To apply this method, you estimate the total number of units the asset is expected to produce over its useful life, then calculate depreciation expense by multiplying the number of units produced in a given period by the depreciation cost per unit. This approach provides a more accurate reflection of the asset’s value decrease in relation to its usage, making it ideal for machinery or equipment that experiences variable workloads.

Calculating Depreciation Example: Straight Line Method

For example, if a company purchases machinery for $50,000 with an expected salvage value of $5,000 and a useful life of 10 years, the depreciable cost would be $45,000. Using the straight-line method, the annual depreciation expense would be $4,500 ($45,000 divided by 10 years).

It’s also important to periodically review and adjust these estimates as necessary. Changes in market conditions, usage patterns, or technological advancements can affect the asset’s value and useful life, requiring updates to the depreciation calculations to maintain accurate financial statements.

Calculating Depreciation Example: Declining Balance Method

Let’s suppose that the equipment purchased above was cutting edge technology in a high-research field. This means that more advancements are expected in this technological field in the near future that could likely render this current technology obsolete. In this case it would be most appropriate to use the declining balance method, which rapidly depreciates the asset’s value in the early years to account for fast industry turnover.

The depreciable cost is $45,000 over a 10 year useful life. The straight line depreciation rate would be 10%. The declining balance rate could either be set at double the straight line rate or higher, if applicable, based on the industry.

Year 1 would be 20% x $50,000 (year 1 book value) is $10,000 depreciation.

Year 2 would be 20% x $40,000 = $8000 depreciation.

After several years, the company may choose to switch to the straight line depreciation method, as it may more accurately represent the asset’s depreciation at that point.

Calculating Depreciation Example: Units of Production Method

For example, suppose a company purchases a machine for $100,000 with an expected salvage value of $10,000. The machine is estimated to produce 200,000 units over its useful life. The depreciable cost is therefore $90,000 ($100,000 cost minus $10,000 salvage value). The depreciation cost per unit would be calculated as $90,000 divided by 200,000 units, resulting in $0.45 per unit.

If in the first year the machine produces 30,000 units, the depreciation expense for that year would be 30,000 units multiplied by $0.45 per unit, totaling $13,500. In the second year, if production increases to 50,000 units, the depreciation expense would be $22,500. This method allows the depreciation expense to reflect the actual usage of the asset, so in years of higher production, the depreciation expense is higher, and in years of lower production, it is lower. This aligns the expense more closely with the revenue generated by the asset’s use, providing a more precise matching of costs and benefits.

Choosing the Right Depreciation Method

The selection of a depreciation method depends on the type of asset and the company’s accounting policies – it is important to choose a method that accurately reflects the decrease in value of the asset over its useful life. While the straight-line method is the most common method, the declining balance method may more accurately depict depreciation for assets that lose their value quickly in the early years. The units of production method may be used for assets that have a variable usage pattern, such as machinery or equipment. Overall, it’s important for a competent professional to select the right depreciation method to accurately represent depreciation for precise accounting, financial statement, and tax filing purposes.

Accumulated Depreciation

Accumulated depreciation is the total amount of depreciation that has been recorded over the life of the asset – it represents the total decrease in value of the asset since it was purchased.

The accumulated depreciation account is a contra-asset account that is used to record the total depreciation expense over the life of the asset.

The balance in the accumulated depreciation account is subtracted from the cost of the asset to determine the net book value of the asset.

For example, assume we are in year 3 after purchasing new equipment for $50,000. The equipment has a $4,500 annual depreciation expense (as we calculated earlier with the straight line method). The equipment’s accumulated depreciation to date would be $4,500 x 3= $13,500. The asset’s net book value would be $50,000 – $13,500 = $36,500. This value is particularly important to know if the company is considering a sale of assets, so they can price the asset fairly for sale and report any capital gains or losses accurately for capital gains tax purposes.

Depreciation Schedule

A depreciation schedule is a table that shows the depreciation expense for each year of the asset’s life – it is used to calculate the depreciation expense for each year. The depreciation schedule is based on the depreciation method used, such as the straight-line method or the declining balance method.The depreciation schedule is used to determine the annual depreciation expense and the accumulated depreciation over the life of the asset.

Financial Statements: Income Statement & Balance Sheet

Financial statements, such as the income statement and balance sheet, are used to report depreciation expense and the net book value of assets – they provide information about the financial position and performance of the company. The income statement shows the depreciation expense for each year, while the balance sheet shows the net book value of the asset. Financial statements are used by investors, creditors, and other stakeholders to make informed decisions regarding the company.

Tax Implications

Depreciation has important tax implications, as it reduces taxable income. However, it is crucial to be aware that the tax depreciation method may differ from the financial reporting method. The tax depreciation method is based on the Modified Accelerated Cost Recovery System (MACRS), which provides a schedule for depreciating assets over their useful life. The tax depreciation method is used to calculate the tax depreciation expense, which is subtracted from taxable income to determine the tax liability. Be that your accountant is informed about which depreciation method your company uses for accounting and how that may differ from MACRS.

Accounting Considerations

Depreciation is an important accounting consideration, as it affects the financial statements and tax liability of the company. It is essential to accurately calculate the depreciation expense and record it in the financial statements, along with disclosing which depreciation methods were used to determine the depreciation expense. The accounting considerations for depreciation include selecting the best depreciation method, calculating the depreciation expense, and recording the asset’s depreciation in the financial statements.

Conclusion

Understanding what depreciation is and how to calculate it is essential for accurately reflecting the value of long-term assets in financial statements. Depreciation spreads the cost of a depreciable asset over its expected useful life, matching expenses with the revenue generated by the asset. By choosing the appropriate method of depreciation—whether straight-line, declining balance, or units of production—businesses can better represent the asset’s decrease in value over time. Properly accounting for depreciation impacts net income, tax liabilities, and the overall financial health of a business.

Maintaining an accurate depreciation schedule and regularly reviewing asset values ensures compliance with financial accounting standards and provides valuable insights for informed decision-making. Depreciated assets impact the value of the company as a whole, and is especially relevant when looking to sell a business. Contact AVGI today to discuss the effects of depreciation on your company and benefit from over 30 years of expert valuation experience and guidance. We look forward to speaking with you.