Understanding the Quality of Earnings Report: Crucial Insights for Business Owners and Investors

Quality of Earnings reports are a crucial tool in assessing a company’s financial health and performance. These reports provide an in-depth analysis of the sustainability and reliability of a company’s past earnings and translate them into forward-looking terms.

Additionally, they assess the company’s financial performance, comprehensively analyzing financial statements, revenue, and expenses. This assists business owners, investors, buyers, and sellers in making informed decisions regarding investments, mergers, and acquisitions and provides a basis for business valuations.

Join Abrams Valuation Group, Inc. as we delve into the topic of the Quality of Earnings reports to facilitate a better understanding for business owners and investors. We aim to empower stakeholders to fully understand QofE reports and leverage them effectively in their decision-making processes, ultimately contributing to more accurate and informed financial evaluations and transactions.

What is a Quality of Earnings Report?

A Quality of Earnings (QofE) report is a comprehensive analysis of the components and sustainability of a company’s earnings. This report is used by investors, analysts, and stakeholders to evaluate the reliability and quality of the company’s reported earnings and to assess the overall financial health and performance of the company.

The Quality of Earnings report translates the company’s past financial performance (such as one might find on the company’s financial statements or in an audit) into a useful “current view” of the company’s earnings from which readers can draw reasonable conclusions about the company’s future. A thorough analytical review of the company’s financial statements is essential for understanding revenue, expenses, and profits during the due diligence process for potential buyers or investors. While a QofE report does not make financial projections, it enables the reader to draw actionable conclusions about the company’s future based on its past performance. The QofE report acts as a bridge between past-oriented audits and future-oriented projections.

The Components of a Quality of Earnings Report: Quality of Earnings Adjustments

The quality of earnings report achieves its unique positioning as a current view of a company’s performance by making adjustments to five areas of a company’s historical performance. These adjustments help in evaluating the sustainability and reliability of the company’s earnings. This allows for deep insights into a company’s financial performance and enables stakeholders to draw actionable conclusions.

Non-essential Expenses: This section adjusts a company’s earnings to remove discretionary expenses that are not essential to the operation of the business and would likely be discontinued by new owners in the case of an acquisition. Examples of expenses to adjust for include business dining, entertainment, or travel expenses. It’s important to note that the expenses considered non-essential can vary drastically depending on the business. What may be a non-essential car for the owner’s convenience on the company dime for one business may be an essential operating expense for another business. Adjusting the QofE report to remove these non-essential expenses gives a more accurate picture of the business’s earning potential.

Cash Flow Analysis: The report includes an analysis of the company’s cash flows to determine if reported earnings are backed by strong and consistent cash generation.

Accounting Policies and Practices: This section examines the company’s accounting policies, practices, and any potential red flags that could impact the quality of reported earnings.

One-Time Events or Charges: It identifies and analyzes any one-time events or charges that might distort the true quality of earnings.

Who writes the Quality of earnings report?

A quality of earnings report is typically prepared by an external CPA or other financial professional who has the expertise to objectively assess the quality and sustainability of a company’s earnings. While an internal company member may potentially be involved in the process, an external party is usually preferred to ensure complete independence, freedom from bias, and thorough analysis. An independent accounting firm plays a crucial role in conducting the QofE report by providing an unbiased evaluation of a company’s financial operations through the analysis of historical financial data.

Quality of Earnings Report Example

A typical Quality of Earnings (QofE) report generally consists of the following components and structure:

Executive Summary: This section provides a brief overview of the key findings and conclusions of the QofE analysis. It highlights the main factors impacting the quality of earnings for XYZ, Inc., and outlines any significant concerns or areas of strength.

Company Overview: This part briefly describes XYZ, Inc., its industry, business model, and recent financial performance. It sets the stage for the QofE analysis by providing context for the company’s earnings quality.

Earnings Quality Assessment:

- Revenue Recognition: Analyze the revenue recognition policies of XYZ, Inc. to determine the consistency and reliability of reported revenues.

- Expense Management: Assess the management of expenses, including any irregular or non-recurring expenses that may impact the quality of reported earnings.

- Earnings Adjustments: Identify and adjust for any one-time events, non-recurring charges, or extraordinary items that could distort the true quality of earnings.

Cash Flow Analysis: Evaluate the cash flow statement of XYZ, Inc. to assess the consistency and sustainability of cash flows in relation to reported earnings. Analyze operating, investing, and financing activities to identify any discrepancies or potential concerns.

Accounting Policies and Practices: Review the accounting policies and practices of XYZ, Inc., focusing on key areas such as revenue recognition, inventory valuation, goodwill impairment, and any changes in accounting standards that may impact earnings quality.

Quality of Assets and Liabilities: Assess the quality of XYZ, Inc.’s assets and liabilities, including the valuation of intangible assets, provisions for doubtful accounts, and potential impairments that could affect the overall quality of reported earnings.

Risk Factors and Future Outlook: Highlight potential risks and uncertainties that may impact the future quality of earnings for XYZ, Inc. Consider industry-specific factors, market conditions, regulatory changes, and company-specific risks that could affect earnings sustainability.

Conclusion and Recommendations: Summarize the key findings from the QofE analysis and provide recommendations for stakeholders based on the assessment of XYZ, Inc.’s earnings quality. Highlight any areas of concern that may require further investigation or attention. Understanding the company’s sustainable earnings through the QofE report can significantly influence the enterprise value during the due diligence phase.

By structuring your QofE report for XYZ, Inc. along these lines, you can create a comprehensive analysis of the company’s earnings quality and provide valuable insights for stakeholders and decision-makers.

Importance of a Quality of Earnings Report in Financial Decision-Making

A Quality of Earnings (QoE) report plays a pivotal role in financial decision-making, especially during mergers and acquisitions (M&A) transactions. This report analyzes a company’s financial performance meticulously, enabling investors and business owners to make well-informed decisions. By scrutinizing a company’s earnings quality, the QoE report illuminates the sustainability and accuracy of its financial statements, which is crucial for determining the company’s value, identifying potential risks, and negotiating deal terms.

A QoE report is indispensable in financial decision-making for several reasons:

Comprehensive Financial Understanding: Beyond just net income, a QoE report offers a thorough understanding of a company’s financial performance, including cash flow and net working capital.

Risk Identification: It helps pinpoint potential risks and areas for improvement, allowing investors to make more informed decisions and avoid unpleasant surprises.

Deal Negotiation: The insights from a QoE report facilitate the negotiation of deal terms, such as the purchase price and financing structure, ensuring a fair and transparent transaction.

Enhanced Due Diligence: Incorporating a QoE report into the due diligence process reduces the risk of unforeseen issues, ensuring a smoother and more efficient transaction.

By integrating a QoE report into the financial decision-making process, investors and business owners can gain a deeper understanding of a company’s financial health and make more informed, strategic decisions.

How does the QofE Report Differ from Other Financial Reports?

The Quality of earnings report is unique in its focus and scope of analysis. Below, we compare the QofE report to several other standard reports to provide more clarity.

Quality of Earnings vs Income Statement Analysis:

While the income statement provides a summary of a company’s revenues and expenses during a specific period, the QofE report delves deeper into the quality and sustainability of the reported earnings, providing a more in-depth analysis.

Quality of Earnings vs Audit:

The auditor’s report focuses on the fairness of the financial statements in accordance with accounting standards, whereas the QofE report evaluates the underlying quality and sustainability of the reported earnings.

Quality of Earnings vs Financial Statements Analysis:

While financial statement analysis provides an overview of a company’s financial performance, the QofE report specifically focuses on the quality and reliability of the reported earnings, offering a more detailed and critical assessment.

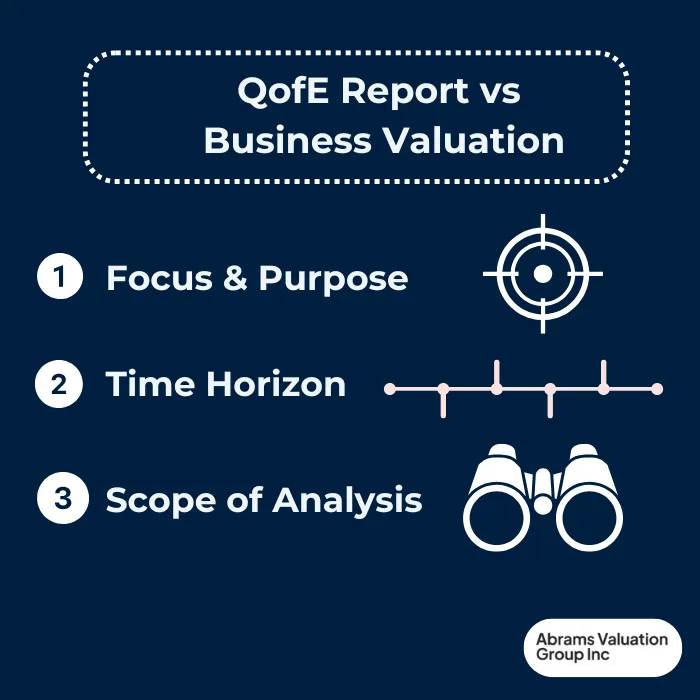

Quality of Earnings (QofE) Report vs Business Valuation in the Due Diligence Process

A Quality of Earnings (QofE) report differs from a business valuation in several key ways:

1. Focus and Purpose:

– QofE Report: The primary focus of a QofE report is to assess the quality and sustainability of a company’s reported earnings. It aims to provide stakeholders with a comprehensive analysis of the components of earnings and the reliability of the financial reports.

– Business Valuation: On the other hand, business valuation focuses on determining a business’s overall economic value. It involves assessing a company’s assets, income, and market position to estimate its total value.

2. Time Horizon:

– QofE Report: The QofE report is typically based on historical financial data and aims to evaluate the quality of earnings over a specific period, often focusing on recent financial performance.

– Business Valuation: Business valuation looks to the future and considers the long-term prospects of a business. It considers future cash flows, growth potential, and risk factors for a valuation figure.

3. Scope of Analysis:

– QofE Report: The QofE report delves deeply into the components of earnings, cash flow analysis, accounting policies, and one-time events to assess the quality of reported earnings.

– Business Valuation: Business valuation considers a wide range of factors, including market dynamics, industry trends, competitive landscape, management quality, and macroeconomic conditions, to arrive at a holistic assessment of a company’s value.

To sum up the differences, while a QofE report specifically focuses on the quality and sustainability of reported earnings, a business valuation takes a more comprehensive approach to determining the total economic value of a business, taking into consideration both historical performance and future potential.

Common Misconceptions About Quality of Earnings Reports

Despite their importance, several common misconceptions about Quality of Earnings (QoE) reports can lead to misunderstandings and underutilization. Let’s address some of these misconceptions:

QoE Report vs. Audit: A common misconception is that a QoE report is the same as an audit. While both examine a company’s financial statements, a QoE report provides a more detailed analysis of the company’s earnings quality and identifies potential adjustments to its financial statements. An audit, on the other hand, focuses on the fairness of the financial statements in accordance with generally accepted accounting principles (GAAP).

Relevance to Company Size: Another misconception is that QoE reports are only necessary for large companies. In reality, QoE reports are essential for companies of all sizes. They are a critical component of the due diligence process, helping investors and business owners make informed decisions regardless of the company’s size.

Frequency of QoE Reports: Some believe a QoE report is a one-time process. However, QoE reports should be updated regularly to reflect changes in a company’s financial performance and earnings quality. Regular updates ensure that stakeholders have the most current and accurate financial information.

Usage Beyond M&A Transactions: While QoE reports are commonly associated with M&A transactions, they are also valuable in other financial decision-making processes, such as financing and investment decisions. They provide a comprehensive view of a company’s financial health, which is beneficial in various contexts.

By understanding and addressing these common misconceptions, investors and business owners can better appreciate the importance of QoE reports and leverage them effectively in their financial decision-making processes.

Bringing it All Together: Quality of Earnings Report

A Quality of Earnings report plays a crucial role in helping stakeholders make informed decisions by providing a deeper understanding of a company’s earnings quality and the sustainability of its financial performance. It is an excellent financial tool to gain deeper insights into the inner workings of a business and its performance.

However, this report is not comprehensive enough on its own for larger and more complex applications, such as setting a sales price in an M&A transaction or for tax or litigation purposes. For a more empirical and accurate representation of a company’s value, the company should obtain a business appraisal from a qualified appraiser. Contact AVGI today if your company needs more accuracy than a QofE report.