Can NOL Offset Capital Gains? Understanding the Rules and Limitations

This is an important tax-planning question that savvy business owners are asking. With the recent legislation extending NOL carryforward for an unlimited number of years (at least until 2028, when legislation will be reviewed again), owners want to know how NOLs interact with Capital gains for future tax planning purposes. AVGI’s valuation experts explore this topic in depth to help business owners make informed decisions about their tax planning options.

Introduction to Net Operating Losses

When business deductions exceed taxable income for the year, that creates a Net Operating Loss or NOL. The NOL can only be carried forward to future tax years, and is considered a deferred tax benefit. NOLs created in recent tax years can only reduce up to 80% of a business’s taxable income in the tax year that the NOL is actualized.

NOLs are a valuable asset that can help businesses reduce their taxable income in future years. However, due to Internal Revenue Service limitations, it can take decades for a business that sustained substantial losses to realize all the tax benefits from the NOLs. Understanding NOL rules is crucial for tax planning and maximizing tax savings, especially for businesses with significant capital gains or losses.

Understanding Capital Gains

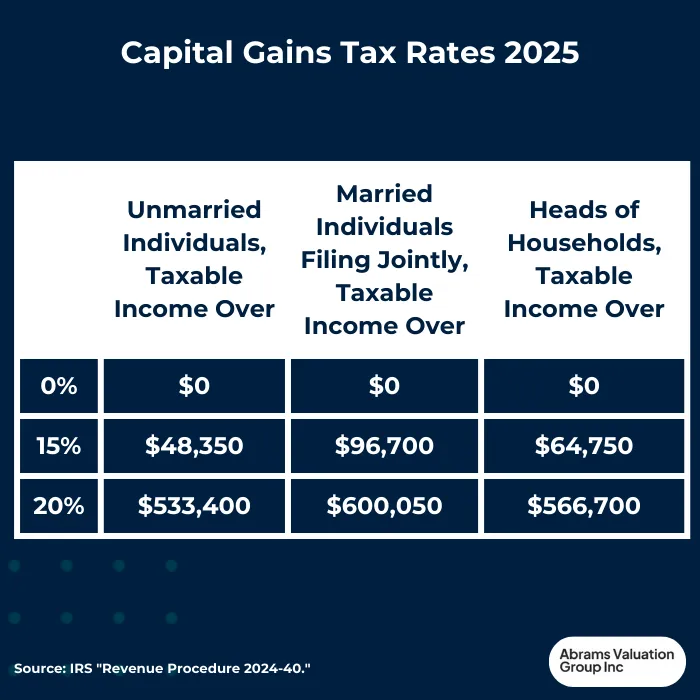

Capital gains occur when an asset is sold for more than its original purchase price, resulting in a taxable gain. Capital gains are classified as either short-term (asset held for under 1 year) or long-term (asset held for 1 year or more), with different tax rates applying to each.

Short-term capital gains are taxed as ordinary income, at the taxpayer’s individuald income tax bracket. In contrast, long-term capital gains are taxed at favorable rates of 0%, 15%, or 20%, based on income and filing status. Capital losses, resulting from selling an asset at a loss, can offset capital gains, reducing taxable gains and lowering tax liability.

Capital Losses and Tax Liability

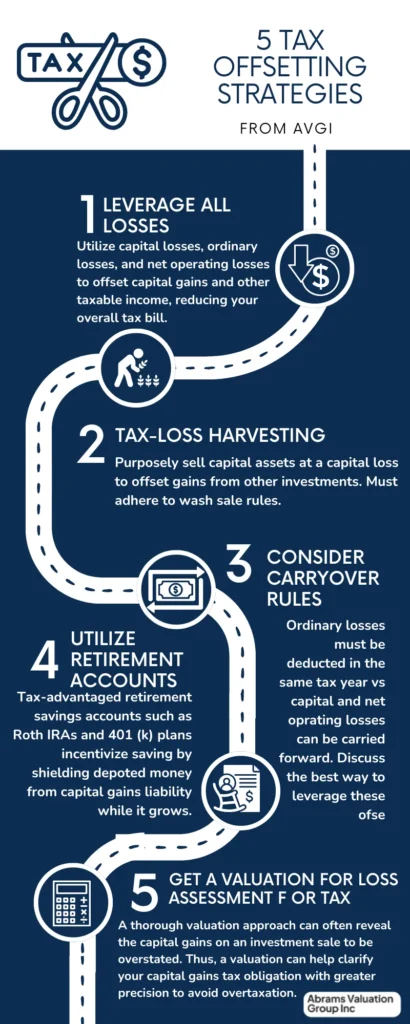

Capital losses can offset capital gains, reducing taxable gains and lowering tax liability. Capital losses can also be carried forward indefinitely, providing a potential tax benefit in future years. However, capital losses are limited to $3,000 annually, and excess losses must be carried forward as an NOL. Taxpayers should consider harvesting capital losses to offset capital gains and reduce tax liability.

Can NOL Offset Capital Gains for Tax Purposes?

No, NOLs from one year cannot be used to offset capital gains in subsequent years, because the IRS considers these as two distinct revenue streams. NOLs can only offset taxable income in future years. Excess capital losses can offset future capital gains. This is important knowledge for business tax planning, as it means that owners must plan well to offset capital gains in a year that they anticipate a sale of assets at a capital gain.

However, they cannot rely on NOLs to offset capital gains. Instead they must employ other tax planning strategies like tax loss harvesting, while adhering to wash rules. In practical terms, planning well to offset capital gains in a compliant way can make a difference of thousands or even millions of tax dollars saved for businesses.

Business Income and Net Operating Losses

Business income encompasses revenue generated from various operations, including sales, services, and interest income. Net operating losses (NOLs) occur when business deductions exceed this taxable income, resulting in a loss that can be carried forward to reduce taxable income in future tax years, thereby lowering tax liability. Additionally, business capital losses can offset business capital gains, offering further opportunities for tax savings. A clear understanding of how business income interacts with NOLs is essential for effective tax planning and maximizing available tax benefits.

Filing Status Considerations

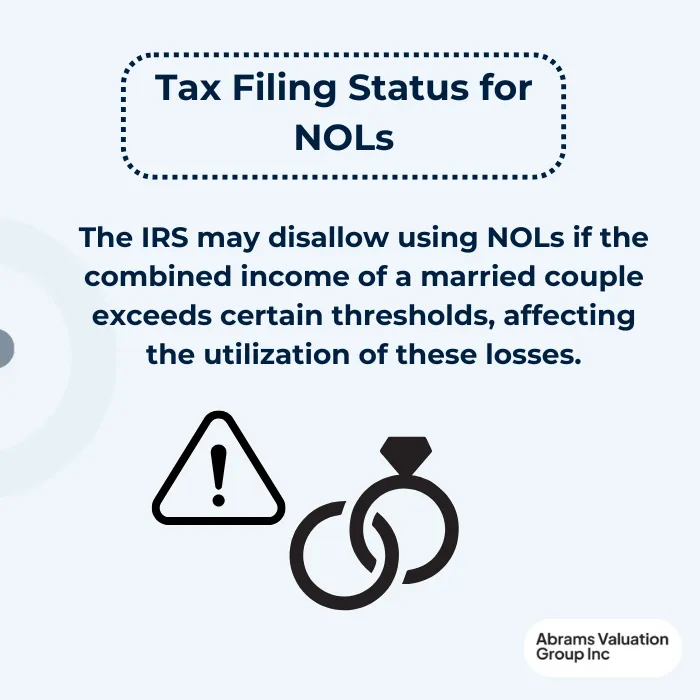

Filing status, such as single, married filing jointly, or head of household, can significantly impact tax liability and the ability to carry forward net operating losses (NOLs). While joint returns often provide additional tax benefits, including increased standard deductions and exemptions, they can also impose limitations on NOL carryovers.

Specifically, the IRS may disallow NOLs if the combined income of a married couple exceeds certain thresholds, affecting the utilization of these losses. Therefore, understanding the implications of filing status is essential for effective tax planning and maximizing NOL benefits. Taxpayers should carefully consider their filing status with a qualified tax professional to optimize their tax situation and ensure they take full advantage of available tax provisions.

Net Capital and Tax Planning

Net capital refers to the total capital gains and losses for the tax year, and understanding these rules is essential for effective tax planning and maximizing tax benefits. Tax planning strategies, such as tax loss harvesting, can help minimize net capital gains and reduce tax liability. Taxpayers should carefully review their net capital position when making investment decisions, and consulting a tax professional can be invaluable in developing a tailored tax planning strategy to minimize net capital gains and optimize overall tax savings.

Carry Forward Rules

Net Operating Losses (NOLs) can be carried forward indefinitely, allowing taxpayers to apply them to reduce taxable income in future tax years. However, there are limits on the amount that can be applied each year, and the IRS may disallow NOL carryovers if the taxpayer’s income exceeds certain thresholds or if the loss is determined to arise from a nonbusiness activity.

Understanding these carry forward rules is crucial for effective tax planning and maximizing the benefits of NOLs. To ensure proper application of NOL carryovers, taxpayers should maintain accurate records and consult IRS guidance, such as Publication 536, which provides detailed information on carry forward provisions and related tax regulations. See our comprehensive article about NOL carryforward rules here.

Tax Planning Strategies

Effective tax planning strategies, including tax loss harvesting and utilizing net operating loss (NOL) carryovers, can significantly minimize tax liability and maximize available tax benefits. Understanding these rules is essential for taxpayers aiming to reduce their tax burden and achieve their financial goals. To develop a tailored tax planning approach that suits individual needs, consulting a qualified tax professional is highly recommended. Additionally, the IRS provides valuable resources and guidance to help taxpayers comprehend tax planning strategies and optimize their tax savings.

Final Considerations

Taxpayers should carefully evaluate their tax situation and develop a comprehensive tax planning strategy to minimize their tax liability effectively. Understanding the complex tax rules and regulations is crucial for maximizing available tax benefits, and the IRS provides valuable resources to assist taxpayers in navigating these guidelines. For owners who need expert guidance, consulting a qualified tax professional is highly recommended. To ensure accurate business loss calculations—which may be higher than anticipated—contact AVGI today for expert assistance tailored to your unique financial circumstances.