What Is Considered an Estate for Estate Tax Purposes?

When planning for the future, understanding what constitutes an estate for estate tax purposes is crucial for effective wealth transfer and minimizing tax liabilities. The definition of an estate—and what’s included or excluded—directly impacts how much tax your heirs may owe. Here, we break down what the IRS considers part of your taxable estate, which deductions may apply, and why accurate valuation is essential for estate planning.

This article serves as an informative resource on estate planning and estate tax, providing authoritative guidance for readers seeking clarity on these important topics.

Definition of an Estate

For estate tax purposes, an “estate” is the total value of a person’s money and property at the time of their death. The word ‘estate’ can have different legal meanings depending on the context, such as probate assets, non-probate assets, or specific legal procedures. This includes assets owned outright, certain interests in trusts, business ownership stakes, and more.

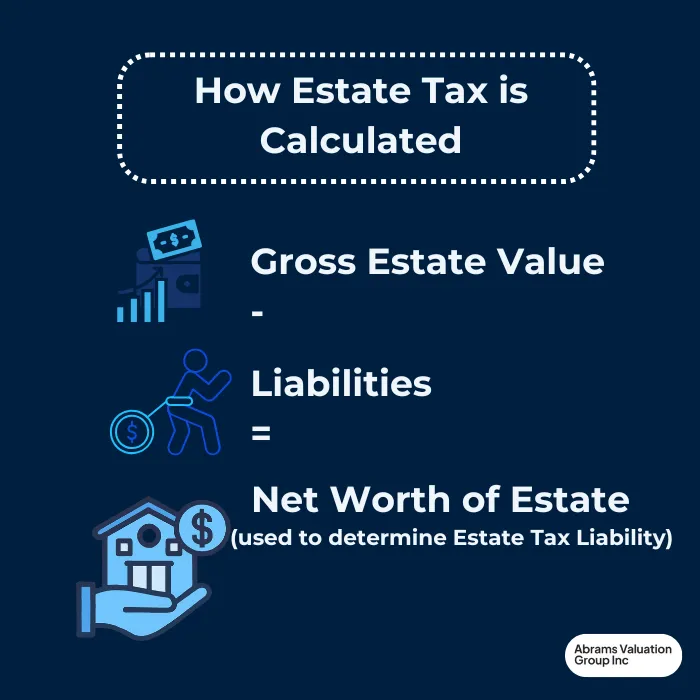

The Internal Revenue Service (IRS) requires a complete accounting of all assets to determine the gross estate, which forms the basis for calculating estate tax liability. The net worth of an estate is calculated by subtracting liabilities from assets. It is important to understand the legal definition of an estate to ensure effective estate planning and to clarify your rights and responsibilities during estate administration.

Learn more about what the IRS considers part of your estate.

Components Included in the Gross Estate

Individually Owned Assets

- Real Estate: Your personal residence (home or house), vacation homes, rental properties, mansions, and land are all included.

- Bank Accounts: Checking, savings, and money market accounts, regardless of their location.

- Investments: Stocks, bonds, mutual funds, and other securities form part of the estate.

- Personal Property: Cars, boats, jewelry, artwork, collectibles, furniture, personal belongings, and household items.

Business Interests

- Sole Proprietorships: The full value of your business is included.

- Closely Held Corporations, Partnerships, LLCs: Your ownership percentage, valued at fair market value, is part of the estate. Learn more about valuing closely held business interests for estate tax.

Retirement Accounts

- IRAs, 401(k)s, Pensions: The account value at death is included, even if beneficiaries are named. These accounts often have a designated beneficiary, and assets with beneficiary designations do not go through probate. Accounts with beneficiary designations are generally not considered part of the probate estate.

Life Insurance Proceeds

- Policies Owned by the Decedent: If you own the policy, the death benefit is included.

- Incidents of Ownership: Even if you’re not the beneficiary, if you can change beneficiaries or borrow against the policy, the proceeds may be taxable.

Trust Assets

- Revocable Trusts: Assets in trusts you control are included.

- Certain Irrevocable Trusts: If you retain certain rights or interests, these assets may be pulled back into the estate.

Living trusts are a proactive estate planning tool that can allow assets to transfer without going through probate, helping to reduce delays and protect assets as part of comprehensive estate management.

Jointly Owned Property

- Right of Survivorship: The full value may be included unless co-owners contributed.

- Tenancy in Common: Only your share is included.

Property that is titled only in the deceased person’s name is considered probate property and must go through probate.

Gifts Made Within Three Years of Death

The Clawback Rule states that certain gifts, especially those involving life insurance or with retained interests, are added back to the estate if made within three years of death. See IRS details on gifts and estate tax.

Excluded Assets: What is not considered part of an estate?

Not all property is included in the gross estate. Assets that are irrevocably transferred—meaning the decedent no longer has control or beneficial interest—are generally excluded. Examples include:

- Assets solely owned by others

- Irrevocable trust assets with no retained interest or control

Deductions from the Gross Estate

Several deductions can reduce the taxable estate, including:

- Debts and Liabilities: Mortgages, credit card debts, and other outstanding obligations.

- Funeral Expenses: Reasonable costs can be deducted.

- Charitable Bequests: Gifts to qualified charities are fully deductible. Learn more about charitable giving strategies.

- Marital Deduction: Transfers to a surviving spouse are generally exempt from estate tax.

Valuation of Estate Assets

Estates can be large or small, and the total lot or value of all assets must be carefully determined, as this affects probate procedures and estate planning strategies. The IRS requires assets to be valued at their fair market value as of the decedent’s date of death. Alternatively, executors may elect an alternate valuation date (six months after death) if it reduces the estate’s value and resulting tax. An estate may include digital assets such as cryptocurrencies and social media accounts, which also need to be valued alongside traditional assets.

Accurate, defensible valuation—especially for illiquid or unique assets like a family business, business interests, or intangible assets such as intellectual property—is essential to ensure that heirs pay the correct amount of estate taxes. Proper valuation protects heirs from potential disputes with tax authorities and helps avoid costly penalties or delays in estate settlement.

Given the complexities involved, obtaining an expert appraisal is critical for a fair and legally sound tax filing. For over 30 years, AVGI experts have specialized in valuations for estate and gift tax purposes, providing reliable, precise assessments tailored to each unique estate. Contact AVGI today for a valuation consultation to safeguard your estate planning and ensure compliance with tax regulations.

Creating an Estate Plan

Most people have an estate, regardless of its size, and should consider estate planning to ensure their assets are managed and distributed according to their wishes. An estate includes everything a person owns at the time of death, including bank accounts, personal property, real property, and vehicles. Whether an estate must go through probate depends on factors such as asset titling, legal planning, and state law. Many states have simplified procedures for small estates that allow heirs to bypass full probate. Engaging an experienced estate planning attorney is essential to minimize probate and ensure assets are distributed according to the deceased’s wishes.

Wills are legal documents that direct asset distribution and can help avoid lengthy probate procedures. The executor, referred to as the person responsible for managing the estate, is appointed by the probate court and has a legal duty to all heirs and people named in the will to ensure they receive their inheritance. The executor must ensure all debts and claims, such as those from Medicaid, are paid from estate assets before distributing the remainder. The legal process and schedule for estate administration are governed by state law. A crucial part of this planning involves understanding what constitutes an estate, including joint ownership, designated beneficiaries, and beneficiary designations that facilitate effective asset transfer.

Additionally, proper estate planning accounts for debts, creditors, and heirs to ensure a fair distribution of the estate and protect heirs from outstanding debts. Starting the estate planning process early, with guidance from a knowledgeable lawyer, helps individuals gain clarity on ownership, debts, and post-death decisions, enabling informed choices about their estate, including property, houses, and land.

Conclusion

Understanding what constitutes an estate for tax purposes is the foundation for smart estate planning. With the right knowledge and professional advice, you can minimize taxes, avoid surprises, and ensure your legacy is preserved for future generations.