Estate Tax Exemption 2026: Key Changes & Strategy for Smart Business Owners

The State of Estate Tax in 2026

The future of the estate tax in 2026 was highly uncertain due to the scheduled sunset of the 2017 estate tax exemption set for January 1, 2026. This looming expiration threatened to significantly reduce the exemption amounts, potentially increasing estate tax liabilities for many taxpayers. Adding to the uncertainty were President Trump’s remarks in July 2025, which fueled speculation that the US estate tax might be eliminated altogether.

One Big Beautiful Bill Brought Clarity to Estate Taxes

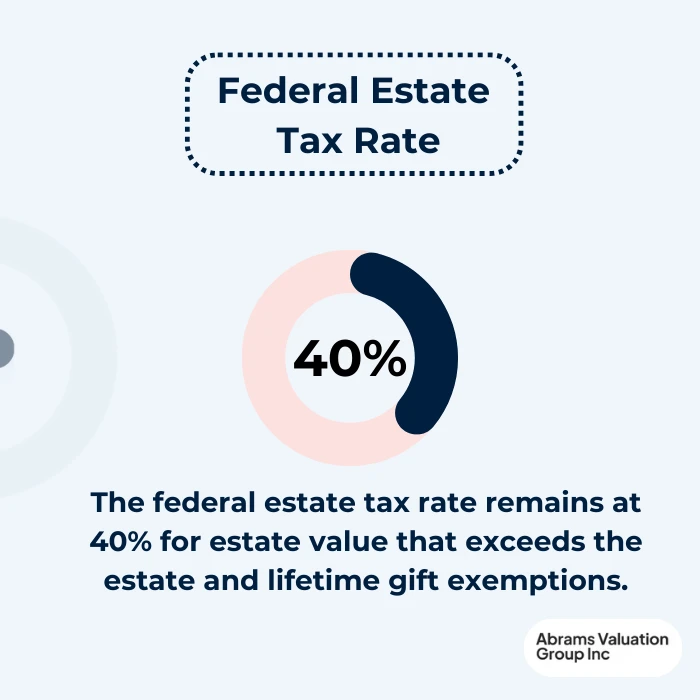

Public Law 119-21, known as the One Big Beautiful Bill Act (OBBB), was passed into law on July 4, 2025, bringing clarity to taxpayers on estate taxes. This bill did not eliminate the estate tax; instead, it set the estate tax exemption at $15 million per individual, effective in 2026. Furthermore, the bill makes the increased exemption amount permanent and indexed for inflation starting in 2027. The federal estate tax rate remains at 40% for amounts above the exemption.

This legislative change ensures that the exemption amounts will increase annually to keep pace with inflation, providing greater certainty and stability for taxpayers and estate planners. The OBBBA eliminates the ‘use it or lose it’ urgency in estate planning by eliminating sunset provisions, giving people more peace of mind to make good estate planning decisions. This clarity allows taxpayers and estate planners to move forward with confidence under the new rules.

Below is a detailed overview of the estate tax exemption limits for 2026, reflecting the latest changes and providing important information for single individuals, married couples filing separately, and married couples filing jointly.

Filing Status | Estate Tax Exemption 2025 | Estate Tax & Gift Tax Exemption 2026 | Annual Gift Tax Exclusion 2026 |

|---|---|---|---|

Single Individuals | $13,990,000 | $15,000,000 | $19,000 |

Married Filing Separately | $13,990,000 | $15,000,000 | $19,000 |

Married Filing Jointly | $27,980,000 | $30,000,000 | $38,000 |

This table highlights the significant increase in exemption amounts compared to previous years, largely due to legislative changes. Understanding these exemptions is crucial for effective estate planning and minimizing potential estate tax exposure in 2026 and beyond.

5 Estate and Gift Tax Planning Takeaways for Small Business and Farm Owners

1. Significantly Increased Exemption Provides Planning Opportunity

The exemption has been set at $15 million for 2026 (indexed for inflation thereafter) under the One Big Beautiful Bill Act (P.L. 119-21), with the 2025 exemption at $13.99 million. Married couples can combine their exemptions, and any unused exemption can be inherited by a surviving spouse, effectively allowing up to $30 million in combined exemptions for 2026.

Action Step: Review your current estate plan to determine whether your business and personal assets will exceed these thresholds. If you’re approaching these limits, proactive planning is essential now while the higher exemptions remain in place.

2. Obtain a Professional Business Valuation to Identify Minority Interest and Marketability Discounts

One of the most powerful planning tools for family-owned businesses involves proper valuation that accounts for minority interest discounts and lack of marketability discounts. There have been proposals to disallow minority discounts, though these have not been enacted. Currently, minority ownership interests and illiquid business interests can be valued at discounts ranging from 10% to 50% or more.

Why This Matters: If you own a $10 million business and structure ownership to create minority interests (such as gifting non-controlling shares to children), those interests might be valued at only $6-7 million for estate tax purposes after applying appropriate discounts for lack of control and marketability. This can result in substantial estate tax savings.

Action Step: Engage a qualified business appraiser certified in business valuation (ASA, ABV, or CVA designation) to conduct a formal valuation that properly accounts for:

- Minority interest discounts (for non-controlling ownership stakes)

- Lack of marketability discounts (for closely-held, non-publicly traded interests)

- Any special circumstances affecting your business value

Document these valuations thoroughly, as concerns about estate and gift taxes often center on farms and family businesses, where assets are not liquid, and a number of special rules are in place to protect them.

3. Leverage IRC Section 6166: Defer Estate Tax Payments Over 14 Years

For farms and family businesses where assets are not liquid and paying the tax could require selling some or all of the business, family businesses can pay any estate tax due on businesses in installments over 14 years.

Qualification Requirements:

- The interest in a closely held business must exceed 35 percent of the decedent’s adjusted gross estate

- The business must be actively operated (not a passive investment)

- For partnerships, the deceased partner’s interest must be 20 percent or more of the total capital interest, or the partnership has 45 or fewer partners; for corporations, 20 percent or more of voting stock must be included in the gross estate, or the corporation has 45 or fewer shareholders

Benefits: Principal and interest on the deferred tax can be paid over a 14-year period, with the option to defer tax (but not interest) for up to 5 years, then pay in up to 10 equal annual installments.

Action Step: Work with your estate planning attorney to ensure your estate will qualify for Section 6166 deferral. Structure your business ownership and estate to meet the 35% threshold, and ensure the executor knows to make this election on a timely filed Form 706.

4. Farm Owners: Utilize IRC Section 2032A Special Use Valuation

Section 2032A permits certain real property to be valued for Federal estate tax purposes on the basis of its “current use” rather than its “highest and best use,” and may qualify if it is located in the United States and is devoted to use as a farm for farming purposes. The term “farm” is defined to include forest land, and “farming purposes” includes the planting, cultivating, caring for, and cutting down of trees.

Value of This Provision: Farmers and businesses can value assets based on use rather than market value, with a limit on the reduction in value of $1 million, indexed for inflation (a $1.19 million limit in 2021). The current indexed limit is approximately $1.39 million.

Qualification Requirements:

- At least 50 percent of the adjusted value of the estate must be qualified real and personal property used in farming or business, and at least 25 percent must be qualified real property

- The property must have been used for a qualified purpose for at least five of the eight years preceding the decedent’s death

- Property must pass to qualified heirs (family members)

- Material participation by the decedent or family members is required

Action Step: If you own farmland or business real estate that could be valued higher for development purposes than agricultural use, consult with an estate planning attorney about making a Section 2032A election. This can reduce your estate value by over $1 million, resulting in significant tax savings.

5. Implement Strategic Gifting Using Annual Exclusions and Lifetime Exemptions

There is an annual inter vivos gift exemption of $19,000 per donee for 2025, which allows tax-free gifts without using the lifetime exemption.

Strategic Approach:

- Make annual exclusion gifts of business interests to family members

- Consider gifting minority interests in your business, which can be valued with appropriate discounts

- Gifts are primarily to children (52%) and grandchildren (19%), allowing multi-generational wealth transfer

Tax Rate Consideration: The taxable estate is subject to a 40% rate, making proactive planning essential for estates exceeding the exemption amounts.

Action Step: Work with your financial advisor and estate planning attorney to develop a systematic gifting strategy that:

- Maximizes annual exclusion gifts ($19,000 per recipient in 2025)

- Strategically uses the lifetime exemption for larger transfers

- Incorporates properly valued minority interests with appropriate discounts

- Documents all transfers with qualified appraisals where required

Summary: Immediate Next Steps

Get a comprehensive business valuation from a qualified appraiser that identifies potential minority interest and marketability discounts.

Review your current estate plan in light of the new $15 million (2026) exemption levels.

Assess qualification for Section 6166 installment payment deferral if you own a closely held business.

Evaluate Section 2032A special use valuation if you own farmland or business real estate.

Implement a strategic gifting program using annual exclusions and lifetime exemptions.

Consult with experienced professionals, including estate planning attorneys, CPAs, and business valuation specialists who understand how to best utilize and apply these complex provisions to your advantage.

The combination of increased exemptions, special valuation methods, deferred payment options, and proper use of discounts can dramatically reduce estate tax liability for family business and farm owners. However, these benefits require advance planning and proper documentation to implement effectively.

Filing an Estate Tax Return

Estate tax returns, filed using Form 706 with the Internal Revenue Service (IRS), are necessary to report estate tax liability and to claim the estate tax exemption. Recent legislative changes have increased the filing threshold, which means fewer individuals are now required to file these returns. It is important to adhere to IRS guidelines regarding filing requirements, exemption amounts, and tax liabilities. Typically, estate tax returns must be submitted within nine months of the decedent’s death, although extensions may be granted under certain circumstances to ensure proper compliance and processing.

Estate Planning Strategies

Effective estate planning strategies, including charitable giving and asset protection, play a crucial role in minimizing estate tax exposure and facilitating a smooth transfer of assets to beneficiaries. Working with tax advisors and attorneys, individuals can develop customized estate plans tailored to their unique needs and goals.

Strategies such as removing future appreciation from the taxable estate are particularly beneficial in reducing estate tax liability. Other important approaches include leveraging minority interest and marketability discounts through professional business valuations, utilizing special use valuations for farmland and business real estate, and deferring estate tax payments under IRC Section 6166. With changes to estate and gift tax exemptions introduced by the Big Beautiful Bill Act, it is essential for individuals to review and update their estate plans to align with the new law and maximize available benefits.

Estate Tax Exemption 2026 Strategies: In Conclusion

In summary, the estate tax exemption for 2026 has increased significantly to $15 million per individual, thanks to the One Big Beautiful Bill Act, providing greater certainty and planning opportunities for taxpayers. Married couples can combine exemptions for a total of $30 million, and the exemption amount will be indexed for inflation starting in 2027.

Strategic estate planning, including professional business valuations, minority interest discounts, and special use valuations, remains essential to minimize tax exposure and preserve wealth. AVGI are expert business valuation professionals specializing in valuations for estate and gift tax purposes. To ensure your estate plan maximizes the benefits of the new exemption limits and aligns with current law, contact AVGI today for an obligation-free consultation.