How to Avoid Taxes on Inheritance: 10 Strategies To Minimize Tax Burden

Introduction to Estate and Inheritance Taxes

Estate tax and inheritance tax are two important types of taxes that can significantly affect the transfer of wealth after death. Understanding the distinctions between the federal estate tax and state inheritance tax is essential for effective estate planning and minimizing the tax burden on inherited assets. Since these taxes can be complex and vary by jurisdiction, it is highly recommended to seek guidance from an estate planning attorney or tax professional who can tailor advise to your situation. This article explores 10 effective strategies to help you navigate estate and inheritance taxes, reduce tax liability, and protect your assets for your beneficiaries.

Understanding Federal Estate Tax

The federal estate tax applies to estates with a value exceeding $13.99 million in 2025, with tax rates ranging from 18% to 40%. This tax is imposed on the taxable estate itself, which includes assets such as real estate, investments, life insurance, and other property owned by the deceased at the time of death. It is important to note that the estate pays the federal estate tax before any assets are distributed to heirs or beneficiaries, so the tax liability reduces the estate’s overall value rather than directly affecting the individuals who inherit the assets.

The fair market value of these assets on the date of death is used to determine the taxable estate, and certain deductions and exemptions may apply to reduce the taxable amount. Given the potential for significant estate tax liability, it is essential to consider strategies to reduce estate taxes and preserve wealth for beneficiaries.

Minimizing Inheritance Taxes

Inheritance tax is a state-level tax imposed in only five states in the United States: Iowa, Kentucky, Maryland, Nebraska, and Pennsylvania. This tax is paid by the beneficiary receiving the inheritance, and the rate varies by state law and the beneficiary’s relationship to the deceased. In addition to these inheritance taxes, twelve states impose their own state estate tax on the deceased person’s estate, separate from the federal estate tax.

Minimizing inheritance and estate tax liability requires careful estate planning, which may include establishing trusts, using gift tax exemptions, and making charitable donations. Understanding the varying inheritance and estate tax rates and exemptions across different states is essential for effective estate planning and reducing the overall tax burden on inherited assets.

Estate Taxes vs Inheritance Taxes

In the table below, we break down all the differences between estate and inheritance taxes.

Feature / Category | Federal Estate Tax | State-Level Estate Tax | Inheritance Tax |

States Affected | All states (federal law) | CT, DC, HI, IL, MA, ME, MD, MN, NY, OR, RI, VT, WA | IA, KY, MD, NE, NJ, PA |

Tax Rates | 18%–40% (progressive) | Varies by state, typically 0.8%–20% | Varies by state, up to 18% (PA); usually 4%–16% |

Who Pays the Tax | Estate (before distribution to heirs) | Estate (before distribution to heirs) | Beneficiaries (heirs who receive inheritance) |

Exemption Amount | $13.99 million per individual (2025) | Varies by state, from ~$1 million to $12.9 million | Varies by state and heir’s relationship to deceased |

Taxable Assets | Global assets of the deceased | State-resident’s assets or in-state assets of non-residents | Inheritance received by beneficiary |

Impact of Relationship | No effect—same for all heirs | No effect—same for all heirs | Yes—closer relatives (spouse, children) often exempt or taxed at lower rates |

Deductibility | State estate taxes may be deductible from federal tax | Federal and other state taxes may be deductible | Not deductible on federal tax return |

When Tax is Paid | After death, before assets are distributed | After death, before assets are distributed | After inheritance is received |

Practical Strategies to Minimize Inheritance Taxes

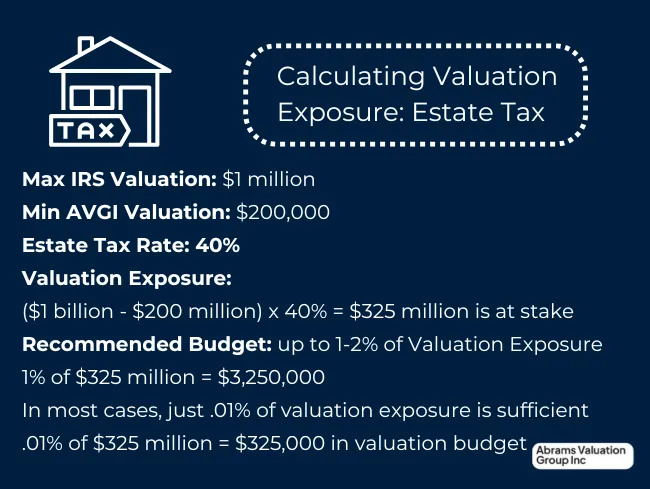

Seek Accurate Estate Valuation

Hire qualified appraisers and financial experts to assess the true value of estate assets. An accurate valuation ensures you do not pay taxes on inflated asset values, which the IRS may overstate. Ensuring proper documentation and expert opinions can often result in significant tax savings. This is particularly important for unique or illiquid assets such as real estate, artwork, or privately held businesses.

Utilize the Lifetime Estate and Gift Tax Exemption

Take advantage of the federal estate and gift tax exemption, which allows individuals to transfer a significant amount of wealth tax-free over their lifetime. Strategic gifting can gradually reduce the size of your taxable estate. It is important to keep careful records of all gifts and consult with a tax advisor to maximize the benefit.

Leverage the Step-Up in Basis Rule

When heirs inherit assets, the cost basis is “stepped up” to the asset’s current market value at the time of inheritance. This means that if the asset is later sold, heirs only pay capital gains tax on appreciation after the date of inheritance. This can significantly reduce or even eliminate capital gains taxes on inherited property.

Establish Trusts for Asset Protection

Irrevocable trusts, such as Grantor Retained Annuity Trusts (GRATs) or Qualified Personal Residence Trusts (QPRTs), can be used to remove assets from your taxable estate. Trusts provide control over how and when heirs receive assets, and can help avoid probate. Many trusts are designed specifically to take advantage of tax-saving provisions in the law.

Gift Assets During Lifetime

Gifting assets to heirs while still alive allows you to utilize the annual gift tax exclusion, reducing the size of your taxable estate over time. Spreading gifts over several years can help maximize tax-free transfers. Coordinating gifts with your overall estate plan can ensure you stay within legal limits and achieve your family’s financial goals.

Charitable Giving Strategies

Donating a portion of your estate to qualified charities can reduce your taxable estate and provide valuable tax deductions. Charitable trusts and bequests can be structured to benefit both heirs and charitable organizations. This strategy not only minimizes taxes but also supports causes that are meaningful to you.

Pay Off Debts and Expenses

Outstanding debts and certain expenses can be deducted from the gross value of the estate, lowering the taxable amount. This includes funeral expenses, legal fees, and some outstanding bills. Proactively managing and documenting these liabilities can help reduce the estate tax burden.

Consider State Inheritance and Estate Tax Laws

Some states impose their own estate or inheritance taxes, separate from federal taxes. Understanding and planning for state-specific rules can help avoid unexpected tax liabilities. Relocating or structuring assets with state laws in mind can sometimes yield significant savings.

Utilize Family Limited Partnerships (FLPs) or LLCs

Transferring assets through family limited partnerships or limited liability companies can create valuation discounts, reducing the reported value of the estate for tax purposes. These structures also offer flexibility in management and distribution of assets among heirs. Proper legal setup is crucial to ensure these benefits are recognized by tax authorities.

Work with Experienced Estate Planning Professionals

Estate laws are complex and subject to change, so it’s vital to consult with experienced estate attorneys and tax advisors. Professionals can tailor strategies to your specific family and financial situation, ensuring compliance and optimal tax outcomes.

For those managing assets on behalf of others, resources like the Consumer Financial Protection Bureau’s guide to Managing Someone Else’s Money offers valuable support. Regular reviews and updates to your estate plan are essential to keep pace with changing laws and circumstances.

Capital Gains Tax Considerations

Capital gains tax applies to the sale of inherited assets, such as real estate or investments, and can significantly impact the overall tax burden. Typically, the cost basis of these inherited assets is stepped up to their fair market value at the time of the deceased’s date of death, which helps reduce the capital gains tax liability when the assets are eventually sold. Understanding the rules and exemptions related to capital gains tax is crucial for minimizing taxes on inherited property. To ensure compliance with all relevant laws and regulations, it is advisable to consult a tax professional who can provide tailored guidance on managing capital gains tax implications effectively.

Income Tax Implications

Income tax implications must be carefully considered when inheriting assets such as retirement accounts or life insurance policies, as these inherited assets may be subject to income tax depending on the type of asset and the beneficiary’s tax bracket. Understanding these income tax implications is essential for minimizing taxes and ensuring compliance with tax laws and regulations. To navigate these complexities effectively, it is highly recommended to seek professional advice from a qualified tax professional or financial advisor who can provide tailored guidance based on your specific situation.

Avoiding Inheritance Tax on Specific Assets

Certain assets, such as life insurance policies and retirement accounts, may be subject to inheritance tax or income tax, making it crucial to understand the tax implications of these specific assets for effective estate planning and minimizing taxes. Strategies to avoid inheritance tax on these assets often include the use of trusts, careful beneficiary designations, and tax-free transfers. Consulting with a tax professional or estate planning attorney is highly recommended to ensure compliance with tax laws and regulations and to tailor strategies that best fit individual circumstances.

State-Specific Inheritance Tax Rates

State-specific inheritance tax rates and exemptions vary significantly across the United States, making it essential to understand these differences for effective estate planning. While the federal government does not impose an inheritance tax, several states, including Maryland, Nebraska, Kentucky, New Jersey, and Pennsylvania, do levy this tax on beneficiaries receiving assets from a deceased person’s estate.

The rates and exemptions often depend on both the beneficiary’s relationship to the deceased and the value of the inherited assets. For example, Maryland imposes a 10% inheritance tax but exempts transfers to a surviving spouse, children, and certain other close relatives. In contrast, Nebraska’s inheritance tax rates range from 1% to 15%, with non-relatives subject to the highest rate on amounts exceeding $25,000. These state-specific rules can significantly affect the tax liability of heirs, so seeking professional advice from a tax professional or estate planning attorney is highly recommended to ensure compliance with local laws and to optimize tax planning strategies.

Federal Inheritance Tax Exemptions

The federal government does not impose an inheritance tax, but some states do. Federal inheritance tax exemptions may apply to certain assets, such as life insurance policies and retirement accounts. Understanding these federal inheritance tax exemptions is essential for minimizing taxes and ensuring compliance with tax laws and regulations. Consulting a tax professional or estate planning attorney can help ensure that you comply with federal tax laws and optimize your tax planning strategies.

Estate Taxes and Trusts

Trusts can serve as an effective strategy for reducing estate taxes and avoiding the often lengthy and costly probate process. In particular, irrevocable trusts offer valuable tax benefits and enhanced asset protection by transferring ownership of assets out of the taxable estate. However, understanding the tax consequences and implications associated with different types of trusts is crucial for effective estate planning and minimizing tax liability. Given the complexities involved, it is highly recommended to seek professional advice from an experienced estate planning attorney or tax professional to tailor strategies that best suit your individual circumstances and ensure compliance with current tax laws and regulations.

Capital Gains and Estate Planning

Capital gains tax can significantly impact the tax burden on inherited assets, making it essential to understand the applicable rules and exemptions to minimize taxes and ensure compliance with tax laws and regulations. Effective estate planning strategies often incorporate tools such as trusts, lifetime gift tax exemptions, and charitable donations to reduce capital gains tax liability. Consulting with a tax professional or estate planning attorney is highly recommended to navigate the complexities of capital gains tax and to develop a tailored plan that aligns with your financial goals and legal requirements.

Avoid Paying Taxes on Inherited Assets

Avoiding taxes on inherited assets requires careful planning and a thorough understanding of relevant tax laws and regulations. Effective strategies to minimize tax liability may include the use of trusts, proper beneficiary designations, and tax-free transfers tailored to specific asset types. It is crucial to comprehend the tax implications associated with different inherited assets to optimize estate planning and reduce taxes owed. Seeking professional advice from a qualified tax professional or estate planning attorney is highly recommended to ensure compliance with current laws and to develop a personalized plan that best protects your inheritance.

Inheritance Taxes and Estate Planning

Inheritance taxes can significantly impact the transfer of wealth after death, making it essential to understand the relevant laws and regulations for effective estate planning. Strategies to minimize inheritance taxes often involve the use of trusts, careful beneficiary designations, and tax-free transfers tailored to specific assets. Consulting with a tax professional or an estate planning attorney is highly recommended to ensure compliance with inheritance tax laws and to develop a plan that best protects your assets and beneficiaries.

Conclusion

Avoiding taxes on inheritance requires careful planning and a thorough understanding of tax laws and regulations. Effective estate planning strategies—such as establishing trusts, utilizing lifetime gift tax exemptions, and making charitable donations—can significantly minimize tax liability. It is essential to seek professional advice from a qualified tax professional or estate planning attorney to create an effective plan that ensures compliance with applicable tax laws. Additionally, understanding the tax implications of specific assets and being aware of state-specific inheritance tax rates are crucial components for successful estate planning and reducing overall taxes owed.