How IPO Pricing Is Determined: Key Valuation Methods Explained

Introduction to the Initial Public Offering Process

An initial public offering (IPO) is the process by which a private company becomes a public company, unlocking access to public capital, heightening visibility, and providing liquidity for early investors. Companies go public mainly to raise capital from outside investors to fuel future growth and shake off the limitations of lacking marketability in the private sector. An IPO can create significant capital opportunities and add value for the company, the management team, and existing shareholders through a higher public valuation.

At the heart of a successful IPO lies the critical task of pricing—striking the right balance between maximizing proceeds for the company and ensuring sufficient upside for new investors. For business valuation experts, understanding and executing the complex process behind IPO pricing is both an art and a science. In this article, we explore the methodologies and considerations that shape IPO pricing, offering a comprehensive perspective for valuation professionals.

The IPO Pricing Process: An Overview

IPO pricing is one stage in the broader IPO process involving several stakeholders: the issuing company, investment bankers, the lead underwriter, the underwriting syndicate, institutional investors, regulators, and, ultimately, the public market. The journey begins with internal valuation assessments and culminates in the final offer price announced just before trading commences.

IPO planning often takes 4-6 months and includes due diligence, SEC filings, and review by the Securities and Exchange Commission. Read more in-depth about the IPO readiness process in our comprehensive guide.

Key stages include:

Initial Company Valuation: Early estimates based on financials, growth prospects, and market conditions.

Investor Roadshow: Company executives and underwriters present to institutional investors, meeting potential investors to test market demand.

Book Building: Underwriters compile indications of interest and price levels from potential buyers.

Final Pricing: The offering price, or final price, is typically set just before the IPO date and before trading begins on the stock exchange, taking into account both intrinsic value and real-time market sentiment.

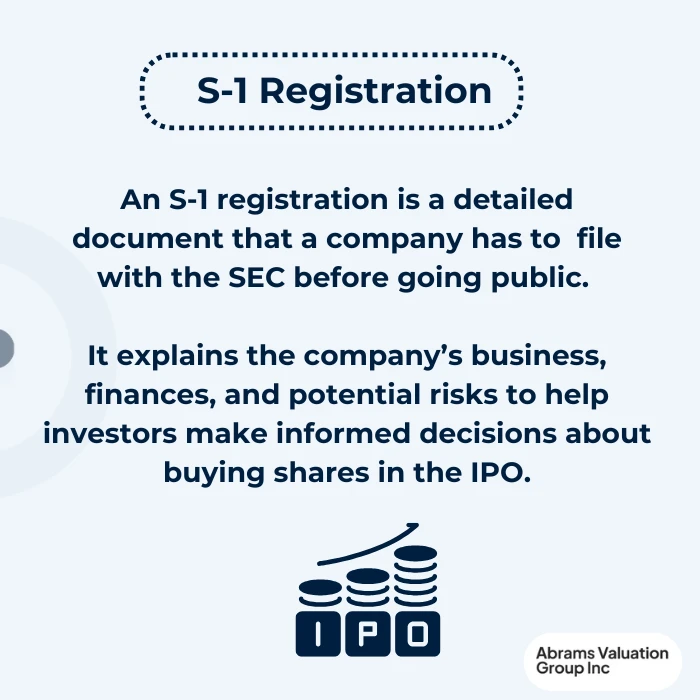

An initial prospectus is filed early in the process and updated as regulatory review progresses.

Throughout, valuation experts play a crucial role in analyzing data, benchmarking against peers, and advising on adjustments in response to market feedback.

Pre-IPO Valuation Foundations

A company’s IPO journey is anchored in its financial history and future prospects. Pre-IPO valuation is part of the broader valuation process and depends on historical performance as well as future growth. Pre-IPO valuation draws heavily on:

Historical Financials: Revenue growth, profitability trends, and cash flow generation, though companies with a limited operating history or those in the early stages may have a shorter track record, which can make comparisons harder.

Projections: Management’s forecasts and scenario analyses, scrutinized for realism and consistency.

Benchmarking: Comparisons with similar companies, including trading multiples from peers with publicly traded stock; investment banks often use this approach to gauge what investors may pay in the new offering.

At this stage, underwriters analyze financial statements and other financial information to support the valuation work.

These foundational analyses inform the choice of valuation methods and provide context for discussions with underwriters and investors.

Core Valuation Methods Used in IPO Pricing

Discounted Cash Flow (DCF) Analysis

DCF remains a cornerstone for intrinsic valuation, projecting future free cash flows and discounting them to present value using an appropriate cost of capital. In an IPO context, sensitivity analyses are crucial—growth rates, margins, and terminal value assumptions are all subject to heightened scrutiny. While DCF offers a rigorous, forward-looking perspective, its reliance on long-term forecasts can be a double-edged sword, especially for companies with limited operating histories.

Comparable Company Analysis (Comps)

The market-based approach involves identifying a peer group through comparable company analysis, comparing the issuer with similar companies that are already publicly traded on the stock market, and benchmarking key valuation multiples such as Price/Earnings (P/E), Enterprise Value/EBITDA, and Price/Sales. Selecting an appropriate peer group is both critical and challenging, and investment banks use these peers’ valuation multiples to estimate a range for the offering price—differences in business models, growth rates, and geographies can lead to widely varying multiples. Current market sentiment and sector trends can also cause rapid shifts in peer valuations, impacting IPO pricing decisions. Bankers may also have the deal priced attractively, sometimes at a 10–15% discount to peer trading multiples, to attract potential investors.

Precedent Transactions Analysis

Reviewing valuations from recent IPOs and M&A transactions offers additional context, especially in dynamic or emerging sectors where direct peers may be scarce. Adjustments are often required for timing (bull vs. bear markets), transaction structure, and one-off company characteristics. For high-growth or disruptive businesses, precedent transactions may provide the most relevant benchmarks, albeit with caution around market exuberance or pessimism.

The Role of Underwriters and Book Building

Investment bankers and the lead underwriter synthesize valuation work and manage the underwriting of the initial sale of IPO shares. They orchestrate the book-building process, with brokerage firms and the underwriting syndicate helping gather orders from institutional investors and other public investors during the roadshow. The depth and quality of demand at various price points inform the final price.

Underwriters analyze market demand, growth potential, and comparable companies to recommend the offering price.

Striking the right balance is essential:

Issuer Objectives: The company’s executives aim to sell shares at a level that supports future growth without weakening aftermarket performance.

Investor Appetite: Attracting committed, long-term shareholders and supporting confidence in the company’s shares.

Post-IPO Performance: Maintaining aftermarket stability; avoiding both dramatic “pops” and disappointing debuts.

The final price determines the gross IPO proceeds before underwriting fees, the net new capital raised, and the company’s initial market capitalization.

Underwriters may also employ price stabilization mechanisms in the initial days of trading to support an orderly market.

Market Demand and Factors Influencing Final IPO Pricing

Beyond company fundamentals, a host of external factors shape IPO pricing. The IPO market itself can swing sharply between hot and cold periods, affecting pricing power for issuers, including those planning to list on the New York Stock Exchange:

Macro-Economic Conditions: Interest rates, inflation, and overall market volatility.

Sector Momentum: Hot sectors may command premium valuations, while out-of-favor industries face headwinds.

Regulatory Environment: Disclosure requirements and legal risks can affect investor confidence.

Media and Public Perception: News coverage and social media sentiment can sway retail investor demand, especially in high-profile IPOs.

Many heavily promoted deals have disappointed once shares begin trading, even when demand looked strong before the ipo date. Valuation experts must monitor these dynamics and adjust their analyses and recommendations as conditions evolve.

Special Considerations in IPO Valuation

Valuing Pre-Revenue or High-Growth Companies

For companies with limited revenues or negative earnings, many of which are still in the early stages and may have limited financial history (common in technology or biotech), traditional multiples are less applicable. Valuation experts may turn to alternative metrics such as Price/User, Price/Downloads, or forward-looking KPIs. When current earnings offer little support, investors focus heavily on growth potential and future growth. Communicating the inherent uncertainty and risk in such valuations is essential—transparency builds trust with both underwriters and investors.

Adjustments for One-Time or Non-Recurring Items

IPO valuations often require normalizing adjustments to remove the impact of non-recurring expenses, extraordinary gains/losses, or pro forma changes (e.g., debt paydowns). Accurate normalization ensures that the valuation reflects sustainable, ongoing performance, and strong due diligence also reviews the management team, financial statements, and financial results before a company becomes publicly traded.

Case Studies

Snowflake (2020): Despite significant pre-IPO hype and high growth, the company opted for a conservative pricing approach and was priced attractively, resulting in a dramatic first-day price surge and a large pop once public trading began—highlighting the challenge of balancing market appetite with realistic valuations. If the deal is intentionally underpriced to generate hype, initial buyers at the IPO price may see immediate gains as the stock price jumps when the market opens.

Uber (2019): Uber’s pricing reflected aggressive growth assumptions, but post-IPO trading was volatile due to concerns about profitability—illustrating the risks of over-relying on optimistic projections. Even with strong pre-IPO demand, the company’s stock can still fall after the initial sale.

Beyond Meat (2019): Priced above the initial range thanks to strong demand, Beyond Meat’s IPO benefited from favorable sector sentiment and peer comparisons, but subsequent volatility underscored the importance of sustainable valuation fundamentals.

Common Pitfalls and Challenges

Over-Optimism: Inflated projections can lead to disappointing aftermarket performance and reputational damage.

Misaligned Incentives: Tensions may arise between maximizing proceeds and ensuring a successful aftermarket.

Conflicting Signals: Different valuation methods may yield divergent results; expert judgment is required to reconcile them.

Investor Risk: For most investors, an IPO stock can be highly volatile, and investors can lose money if the stock price falls below what they paid; this is why due diligence matters before deciding to trade stocks in newly public companies.

Conclusion

IPO pricing is central to the broader initial public offering process and determines how a company enters the public market. For business valuation professionals, combining robust analytical methods with real-time market insights ensures that IPO pricing is both defensible and compelling. As the capital markets evolve, maintaining a holistic, expert-driven approach to valuation remains indispensable for IPO success, especially once trading begins and the company’s stock moves from the offering process into open market pricing on the stock exchange.

If you’re looking to accurately price your IPO stock, the experts at AVGI can help. Contact AVGI today for professional business valuation consulting through the IPO process.