Can Ordinary Losses Offset Capital Gains? Here’s What You Need to Know

As a tax-savvy business owner, you know that you can offset capital gains with capital losses. You may have even employed loss harvesting to offset capital gains and reduce your capital gains tax bill. But you may be wondering about the tax treatment of other types of losses. Can ordinary losses offset capital gains? AVGI delves into the topic to give you the clarity you need.

Defining Ordinary Losses

An ordinary loss is a loss realized by a taxpayer in normal business operations when expenses exceed revenues. Ordinary losses are distinct from capital losses. Ordinary losses are (generally) fully deductible and can be used to offset taxable income in the year of the loss, reducing the tax owed by a taxpayer. Ordinary losses can also be used to offset capital gains, but the beneficial impact of that tax strategy will depend heavily on the taxpayer’s personal situation. AVGI always encourages taxpayers to seek the advice of a tax professional in determining the most advantageous tax strategy for their circumstances.

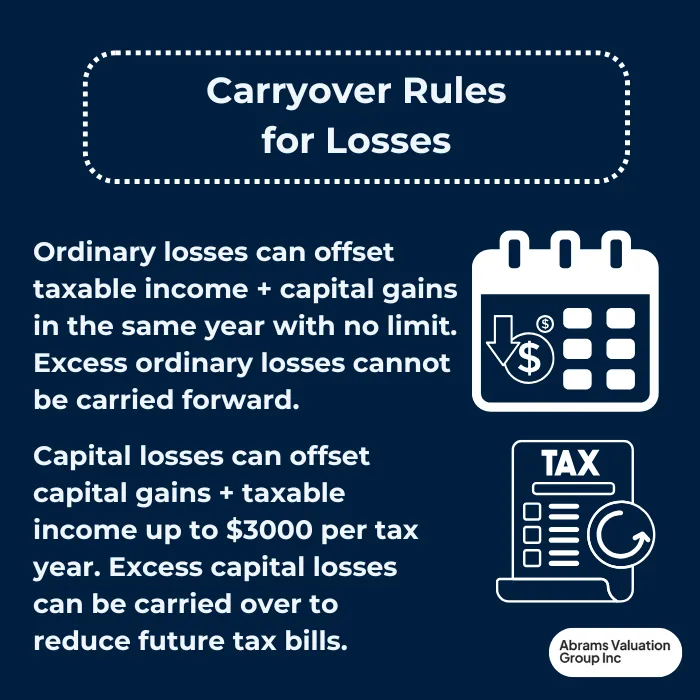

There is no limit on how much ordinary loss can be deducted from taxable income in the year of the loss, which is a substantial advantage for the taxpayer. However, excess ordinary losses cannot be carried forward to offset income in future tax years.

A Recap of Capital Gains and Losses

A capital gain is the profit you make when you sell a capital asset, such as stocks, bonds, or real estate for a higher price than you acquired it. Conversely, a capital loss occurs when you sell a capital asset at a lower price than you acquired it.

Capital gains and losses are subject to different tax treatment and rules than other types of income and losses. For example, long-term capital gains (on assets held for more than one year) are taxed at a lower rate than short-term capital gains. Capital losses can be used to offset capital gains, reducing the amount of capital gains tax owed. Read AVGI’s comprehensive guide to capital gains taxes here.

How to Offset Capital Gains with Ordinary Losses

Ordinary losses can be used to offset capital gains, reducing tax liability. In fact, ordinary losses from an active business or trade can completely offset all capital gains and any other kind of income in the same tax year. If the ordinary losses are substantial, this could, theoretically reduce the taxpayer’s tax liability to zero. It is important to note that unlike excess capital losses that can be carried forward indefinitely, excess ordinary losses cannot be carried forward to future tax years.

Business Losses and Taxable Income

Other types of business losses can offset capital gains as well, further reducing your tax liability. Net operating losses (NOLs) can be deducted from other sources of income, including wages, interest, dividends, and capital gains. However, NOLs must pass the IRS’s at-risk and passive activity tests. If they do pass, then NOLs can legitimately be deducted from taxable income.

Capital Assets and Losses

Capital assets are any property excluding literary, musical, and artistic compositions. Capital gains or losses occur when a capital asset is sold for more or less, respectively than its original cost. Capital losses can be used to offset capital gains, reducing the amount of tax owed. Although long and short term capital gains are taxed differently, either type of capital loss can offset either type of capital gain.

Tax Loss Harvesting Strategy

Tax loss harvesting capitalizes on offsetting rules to reduce capital gains tax liability. With this strategy, the investor intentionally generates capital losses by selling underperforming investments or capital assets to offset capital gains. This strategy is particularly effective and impactful for offsetting short-term gains, which are taxed at a higher rate. Another excellent application of this strategy is offsetting the capital gains from a business sale, which can be a heavy tax burden.

It is crucial to abide by wash sale rules when implementing a tax loss harvesting strategy; failing to do so may undermine the ability to deduct the harvested capital losses from the capital gains, rendering the strategy fruitless.

Deductibility of Losses & Carryover

As we mentioned earlier, ordinary losses are fully deductible from taxable income, with no limits within the same tax year. In contrast, capital losses are subject to a $3,000 annual limit on the amount that can be deducted from ordinary income. However, excess net capital losses can be carried forward to future tax years, while excess ordinary losses cannot be carried forward. These are important considerations to keep in mind when deciding on the most beneficial tax strategy.

Tax Planning Strategies

If your taxpayer portfolio contains business, investments, and capital assets, then it is crucial to consider carryover rules as part of your tax planning strategy. Here are some additional tax planning strategies that have proven to be highly effective for other taxpayers.

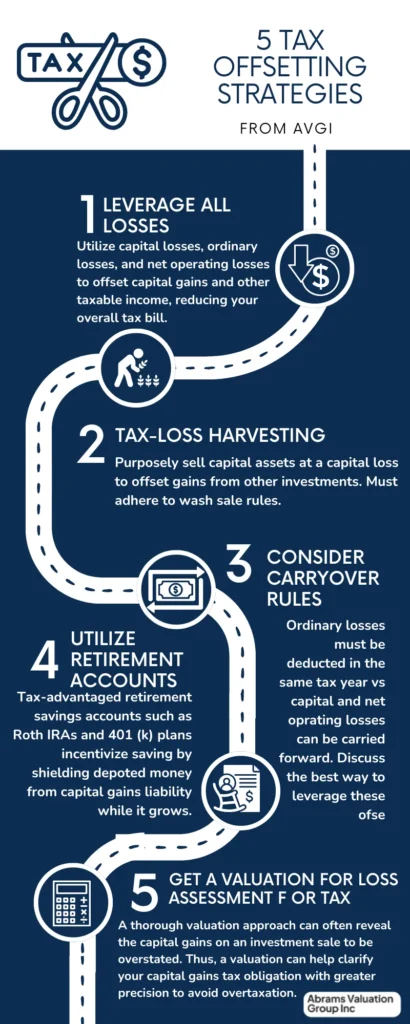

- Offset capital gains with capital losses, ordinary losses and business losses to reduce tax liability.

- Consider deferring capital gains realization until future years with lower taxable income.

- Utilize retirement accounts to shelter capital assets from capital gains taxes.

- Effective planning around gain and loss recognition can help minimize tax liability.

- Consider the most advantageous schedule to carrying forward losses from previous years.

- Get a business valuation for tax purposes to accurately quantify losses to leverage in offsetting gains and taxable income.

As always, discuss these strategies with your personal tax consultant to determine the right ones for your situation.

So, Can Ordinary Losses Offset Capital Gains? In Conclusion

Yes. We have established that taxpayers can use ordinary losses to offset capital gains, reducing their tax liability. Additionally, other business losses, such as NOLs can further reduce taxable income and the total taxes due. Strategic tax planning can help you minimize tax liability and maximize tax savings. AVGI advises taxpayers and business owners in particular to consult with a qualified tax professional to ensure accurate tax planning and compliance.

Business Valuation for Ordinary & Business Loss Tax Purposes

Need help accurately quantifying ordinary or business losses for tax purposes? A business valuation by a qualified valuation professional can empirically establish those losses, which can drastically reduce your tax liability. Contact AVGI today for a free consultation.