IPO Lockup Period and Its Effect on Post-IPO Valuation

A Business Valuation Expert’s Perspective

The initial public offering (IPO) is a pivotal moment for any company, representing not only access to public capital markets but also increased scrutiny and expectations. For business valuation experts, one of the most critical—but sometimes underappreciated—factors influencing post-IPO share price behavior and company valuation is the lock-up period. This article explores the mechanics of lock-up periods, their rationale, empirical evidence regarding their effects, and practical implications for valuation professionals.

Lock-up periods are contractual agreements that restrict certain insiders—such as company founders, executives, employees, and early investors—from selling their shares for a specified period after an IPO, typically 90 to 180 days. These periods are designed to prevent a sudden influx of shares into the market that could destabilize stock prices.

The IPO process is a complex journey involving regulatory filings, due diligence, roadshows, and ultimately, the pricing and allocation of shares. Underwriters and company management work closely to ensure a successful market debut. A key consideration during this process is how to manage the post-IPO trading environment, where lock-up agreements play a vital role.

Lock-up periods are crucial because they help maintain initial market stability, reassure new investors, and influence perceptions of company value. By temporarily limiting share sales by insiders, lock-ups can reduce volatility and provide a buffer against large-scale sell-offs immediately after the IPO.

This article examines lock-up periods from a business valuation perspective, addressing their mechanics, intended effects, empirical outcomes, and best practices for valuation experts advising clients through IPO transitions.

What are IPO Lock-Up Periods?

Standard lock-up agreements typically last 90 to 180 days, though the ipo lockup period varies by deal terms even when standard arrangements often run in that range. The terms specify which insiders are restricted and under what circumstances early releases may occur. Some agreements allow staggered releases or exceptions for specific events, such as mergers or acquisitions.

Stakeholders subject to lock-ups generally include founders, executive management, board members, employees with equity compensation, and early-stage investors. Their collective share ownership can represent a significant portion of the company’s total equity, amplifying the potential impact when lock-ups expire.

Lock-up agreements can vary widely. A lockup agreement is typically a legally binding underwriting agreement that governs when holders of ipo shares may sell shares. Some provide for partial early releases, particularly if the company’s stock price trades above a certain threshold, while others may exclude shares purchased in the open market post-IPO. These nuances must be carefully examined by valuation professionals to assess when and how many shares may become freely tradable.

The legal and regulatory framework for lock-up periods is shaped by stock exchange requirements, securities laws, and underwriter guidelines. A company’s lock-up period is generally self-imposed by the issuer or required by the investment bank underwriting the deal, not mandated by the Securities and Exchange Commission or exchange commission rules, and it remains a near-universal feature of major IPOs that market participants closely scrutinize.

Rationale Behind Lock-Up Periods

Lock-up periods are intended to promote market stability by preventing large, sudden increases in share supply that could depress the stock price, and by stopping company insiders from trying to sell their shares immediately after the company goes public, which protects new stock from an early flood of supply. The restriction also gives the company’s stock time to develop an organic trading history on the public market before existing shareholders and major shareholders can sell their shares. This stability is critical in the early days of public trading, allowing the market to find a fair value for the company’s shares.

The existence and duration of lock-up agreements send signals to the market. Longer lock-ups may reassure public investors, including retail investors, that insiders are committed to the company’s future, while shorter periods or early releases can be interpreted as a lack of confidence, potentially affecting valuation multiples. The lockup period often signals that insiders are confident in the stock’s long-term value, rather than looking to cash out on day one and leave retail investors with a devalued stock.

Underwriters and issuers use lock-up periods as tools to manage the aftermarket for the company’s shares. By coordinating insider sales, they aim to support orderly trading and maximize the IPO’s success.

Lock-ups influence the behavior of insiders both before and after an IPO. Insiders may defer selling for strategic reasons, but the impending expiration can also create anticipation of increased selling pressure, impacting market psychology and trading patterns.

Theoretical Framework for Post-IPO Valuation

Business valuation experts often use discounted cash flow (DCF), market, and income approaches to value post-IPO companies. Each method can be affected by lock-up related dynamics, including potential volatility and liquidity constraints. Valuation models must account for the potential supply shock and price volatility that can accompany lock-up expiries.

Scenario analysis can help anticipate how share prices may react, allowing for more accurate and risk-aware valuations. Lock-up periods can exacerbate information asymmetry. Insiders possess more information about company fundamentals, and their post-lock-up trading can either confirm or contradict market expectations, influencing valuation outcomes.

Empirical Evidence: Lock-Up Expiry and Market Reactions

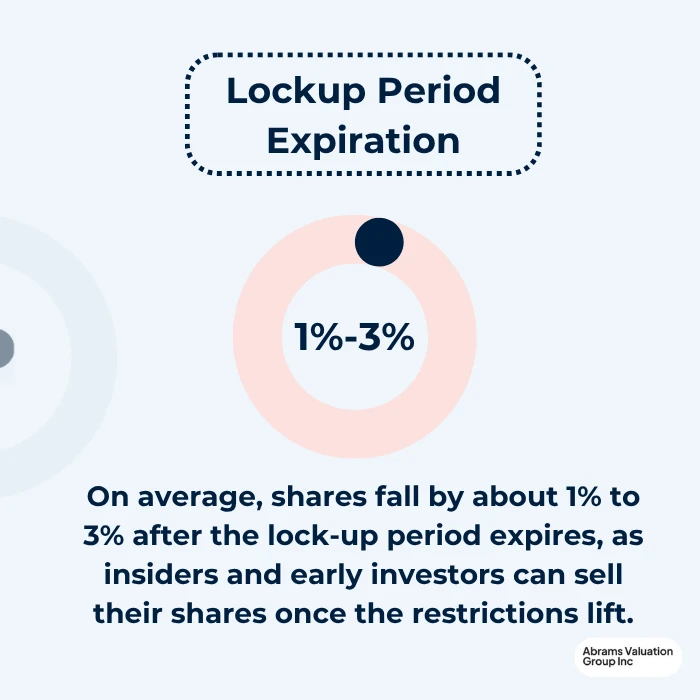

Empirical studies consistently show that lockup expiration can be a key market event: when an IPO lockup expires, stock prices tend to exhibit greater volatility. On average, shares fall by about 1% to 3% after the lock-up period expires, as insiders and early investors can sell their shares once the restrictions lift. The extent of this reaction depends on factors such as the proportion of shares subject to the lock-up and overall market sentiment.

The magnitude and duration of post-lock-up price pressure can vary. Some companies experience only temporary dips, while others face more sustained declines, particularly if insiders sell significant stakes or if the company is in a volatile sector.

Notable IPOs, such as Uber, Facebook, and Beyond Meat, have shown how lock-up expiries can trigger large share price movements. When the lock-up period ends, the first day after the expiration date often brings a jump in trading volume as restrictions are removed. In some cases, the impact is muted by strong fundamentals or positive news flow, while in others, it leads to pronounced volatility and loss of value.

Lock-up effects can vary by sector and geography. Technology and biotech IPOs, often characterized by high insider ownership, may see sharper reactions, while more mature industries or markets with different norms may exhibit less pronounced effects.

Analyzing the Effects on Post-IPO Valuation

The immediate aftermath of a lock-up expiry often sees heightened volatility as new shares become available for trading. This volatility is driven by both actual insider sales and the market’s anticipation that, as the ipo lockup period expires, a price drop may follow because more shares are available to the market.

A sudden increase in the supply of tradable shares (a supply shock) can put downward pressure on prices as the market absorbs the newly available equity. The impact is often proportional to the size of the release relative to average daily trading volumes.

Trading volumes typically spike around lock-up expiries, reflecting both insider sales and heightened speculative activity. High volumes can exacerbate short-term price swings, and some institutional investors and traders respond with short selling ahead of the lock-up expiration, increasing short interest, but this may also help the market reach a new equilibrium more quickly.

The long-term impact of lock-up expiries on valuation is less clear-cut. While some companies recover quickly after an initial dip, others may suffer from a persistent overhang if insider confidence is perceived as weak or if large sales continue.

Insider selling post-lock-up can be interpreted as a negative signal about the company’s prospects, particularly if top executives or founders are involved. However, selling may also be motivated by portfolio diversification or personal liquidity needs rather than pessimism about future performance.

Market sentiment is highly sensitive to insider actions. Large or unexpected sales can undermine investor confidence, affecting valuation multiples and future capital-raising efforts.

A persistent supply of shares from insiders can create an overhang, dampening price appreciation even after the initial post-lock-up volatility subsides. This effect is particularly notable in companies with concentrated insider ownership.

The effect of lock-up expiries may be compounded or mitigated by other post-IPO events, such as earnings announcements or the initiation of analyst coverage. Positive developments can offset selling pressure, while disappointing news can intensify it, depending on market conditions and other factors.

Practical Considerations for Business Valuation Experts

Valuation experts should adjust valuation multiples to reflect the risk of increased supply and volatility around lock-up expiries, with that advice tied to a client’s risk tolerance and overall financial situation because post-IPO stock price fluctuations can be severe around these events. Discounting for potential price dips or using lower comparables can produce more conservative and realistic estimates.

Scenario analysis—modeling valuations before and after lock-up expiration—allows experts to highlight potential risks and opportunities for clients and stakeholders. In some cases, traders may seek to purchase shares after dislocations around expiry, depending on client objectives and risk tolerance. This approach provides a more dynamic, risk-adjusted view of value.

Incorporating behavioral finance and market sentiment considerations into valuation work is essential. Surveys, analyst reports, and market data can help gauge likely market reactions to lock-up expiries.

Clear communication is paramount. Valuation professionals must educate clients about the implications of lock-up periods, ensuring they understand both the risks and opportunities inherent in the post-IPO landscape.

Strategic Implications

Best practices for structuring lock-up periods include staggered releases, performance-based exceptions, and clear disclosure in prospectuses. In initial public offerings, lock-up structures are often set by the issuer and underwriters to prevent insiders from flooding the market when the company transitions from private to publicly traded. These approaches can reduce market shocks and align insider and investor interests.

The timing of secondary offerings should be coordinated with lock-up expiries to minimize market disruption. The company may also raise capital through new stock sales, so coordination matters with respect to the IPO price and aftermarket demand. Proper planning can support price stability and optimize capital-raising outcomes.

Managing insider expectations and ensuring transparent disclosures about lock-up terms and upcoming expiries can help mitigate uncertainty and build market trust. Prospectus and SEC filing disclosures should identify when the lockup period expires and which holders, such as venture capitalists and other existing holders with stock options at a predetermined price, may become eligible to sell.

Issuers should work with advisors to tailor lock-up structures to company- and market-specific factors, while investors should monitor lock-up calendars and anticipate related trading dynamics.

Conclusion

Lock-up periods play a critical role in shaping post-IPO valuation and market dynamics. Their effects are multifaceted, influencing both short-term volatility and long-term investor perceptions. Valuation professionals must account for these complexities to provide accurate, actionable advice. As capital markets evolve, lock-up practices may become more flexible and tailored, with increased transparency and innovation in structuring. Valuation experts will need to stay attuned to these trends and adapt their methodologies accordingly.

For business valuation experts, understanding the nuances of lock-up periods is essential for accurate post-IPO analysis. By integrating empirical evidence, market sentiment, and best practices, professionals can better guide clients through the challenges and opportunities of the IPO transition, since high demand can soften lockup-related pressure, while weaker demand can make the event more disruptive to the company’s reputation.

Contact AVGI today for professional business valuation consulting through the IPO process.