SPAC vs. IPO vs. Direct Listing: How to Choose from a Business Valuation Perspective

Introduction

The decision to take a company public marks a pivotal moment in its lifecycle, with profound implications for valuation, access to capital, and long-term strategy. As business valuation experts, we are increasingly called upon to guide clients through a landscape that now features not only traditional IPOs, but also Special Purpose Acquisition Companies (SPACs) and direct listings. Each path presents unique opportunities and risks, and understanding these nuances is essential for maximizing value and aligning with corporate objectives.

SPAC (Special Purpose Acquisition Company) vs IPO: Key Differences

Special Purpose Acquisition Company (SPAC): A SPAC is a shell company that raises capital through an IPO to acquire an existing private company. This new company places SPAC IPO proceeds in a trust account, then has 18-24 months to pursue deals and find a target company, or return funds if no deal closes. Once a target is identified, the merger effectively takes the private company public, and SPACs can complete mergers in 3-4 months. Recent years have seen a surge in SPAC activity, with high-profile sponsors and significant investor interest. A SPAC sponsor and management team typically receive about a 20% stake for minimal investment, which can shape incentives for SPAC investors.

Traditional Initial Public Offering (IPO): The IPO is the longstanding route to public markets, in which a company issues new shares to raise capital, with the offering underwritten by investment banks that market it to institutional investors. The traditional ipo process involves rigorous due diligence, regulatory scrutiny, and a roadshow to build demand, and the IPO process usually takes about 6-12 months as part of a more complex IPO deal than a SPAC route.

Direct Listing: A direct listing enables a company to list its existing shares on a public exchange without raising new capital or employing underwriters. This path is often chosen by companies with ample cash reserves and strong brand recognition, such as Spotify and Coinbase.

vs

vs

Main Differences Between SPAC, Traditional IPO Process, and Direct Listing

Timeline and Speed to Market: SPACs typically offer a faster route to public markets—often closing in three to four months, whereas traditional IPOs often take six to twelve months. Direct listings are also relatively swift for well-prepared companies.

Regulatory Requirements and Disclosures: IPOs are subject to extensive SEC review and disclosure requirements. While SPACs and their targets must ultimately provide similar disclosures, the process can be less burdensome initially. A SPAC transaction, including the de-SPAC transaction, still involves SEC filings with the Securities and Exchange Commission, including a proxy statement that contains financial statements, historical financial statements, and risk factors. Direct listings, like IPOs, require full transparency but skip the underwriter-driven process.

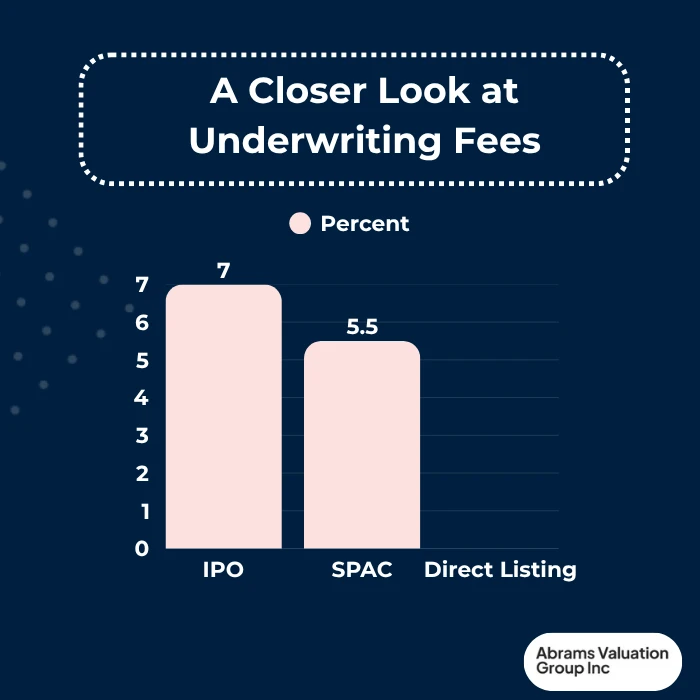

Underwriting and Marketing: IPOs involve investment banks as underwriters and require a roadshow to build demand. SPACs rely on their sponsors for credibility and marketing, with underwriting fees typically around 5% to 6% versus about 7% in an IPO, whereas direct listings forgo both underwriters and roadshows.

Pricing Mechanisms: IPO pricing is determined by underwriters and investor feedback. SPAC valuations are negotiated between the SPAC and the target company, often with input from PIPE (private investment in public equity) investors. Direct listing prices are set by market supply and demand on the first day of trading.

Dilution and Capital Raising: SPACs may lead to significant dilution due to sponsor shares and warrants. IPOs involve dilution through the issuance of new shares, whereas direct listings typically do not create new shares.

Sponsor and Investor Roles: SPAC sponsors play an outsized role, often providing strategic guidance. SPAC shareholders and public shareholders typically vote before the merger, and if shareholders approve the deal, investors can redeem their shares if they do not support the acquired company. In traditional IPOs, underwriters are the main intermediaries. Direct listings rely more on market mechanisms.

Benefits of SPACs Compared to IPOs and Direct Listings

Greater Pricing Certainty: SPACs allow companies to negotiate valuation directly with sponsors and PIPE investors, potentially avoiding IPO “underpricing” and reducing exposure to market volatility tied to capital markets timing.

Faster Execution: The merger process can be completed in as little as three to four months, helping a privately held company become a public company faster when market conditions are favorable.

Flexibility in Deal Structure: SPACs can tailor deal terms to meet the needs of both parties, including earnouts and other incentives.

Access to Experienced Sponsors and Strategic Investors: Sponsors often bring industry expertise and relationships, providing ongoing value post-merger. Public investors often assess spac stock based on the sponsor’s track record and target-sector expertise. For example, DraftKings benefited from the sports expertise of its SPAC sponsors.

Ability to Provide Forward-Looking Projections: Unlike IPOs, SPAC deals can include financial forecasts, which are invaluable for high-growth companies seeking to emphasize future potential.

Potential for Additional PIPE Investments: PIPE financing can supplement SPAC capital, as seen in the SoFi and Lucid Motors deals, providing additional funding and validation. PIPE funding can help raise additional capital beyond the SPAC cash pool when the target needs more funding at closing.

| Feature | SPAC | IPO | Direct Listing |

Main Pros | Faster to market (3–6 months) | Well-established and recognized process | No dilution if no new shares are issued |

| Negotiable valuation | Broad investor access and strong institutional demand | Immediate liquidity for shareholders | |

| Ability to provide forward-looking projections | Enhanced visibility and credibility | Market-driven price discovery | |

| Access to experienced sponsors and strategic investors | Underwriter guidance through valuation and marketing | Lower underwriting fees | |

Main Cons | Greater dilution due to sponsor promote shares | Lengthy process (9–18 months) | No capital raised unless a secondary offering is conducted |

| Potential for mispricing and overvaluation | High underwriting and marketing costs | Volatile price at launch | |

| Regulatory uncertainty and shifting landscape | Rigid regulatory process | Requires strong brand recognition and market profile | |

| Greater post-merger operational risk | Limited ability to provide forward-looking forecasts | Fewer opportunities for traditional marketing/roadshow | |

| Best Suited Industries | High-growth and capital-intensive sectors (e.g., electric vehicles, biotech, technology) | Established, profitable companies (e.g., consumer goods, industrials) | Well-known brands and companies with no immediate capital needs (e.g., tech, media) |

| Typical Timeline | 3–6 months | 9–18 months | 3–6 months |

Drawbacks and Risks of SPACs

Sponsor Incentives and Dilution: Sponsor-promoted shares can lead to substantial dilution for existing shareholders. The experience of Nikola Corporation highlighted how dilution can impact post-deal share value.

Regulatory Scrutiny and Changing Landscape: The SEC has increased scrutiny of SPACs, focusing on disclosure and accounting practices. In early 2024, the SEC adopted new rules that raised investor protection and disclosure expectations for blank check companies. The rules also focus in part on forward-looking statements, require SPACs to disclose all material assumptions in financial projections, and can treat the target as a co-registrant in certain filings. Regulatory uncertainty can complicate transactions for retail investors.

Market and Investor Perception Risks: SPACs have faced skepticism due to perceived risks and some high-profile failures, such as the post-merger performance of Lordstown Motors.

Potential for Overvaluation or Mispricing: Negotiated valuations can lead to over-optimism, resulting in volatile share prices post-listing when stock price pressure builds if optimistic projections are not supported after closing.

Post-Merger Integration and Performance Challenges: The transition from private to public can expose operational weaknesses, as seen with some companies that struggled after going public via SPAC. It also requires public company readiness, including internal controls and stronger reporting discipline.

Industry Suitability: Which Sectors Benefit from Each Path?

Industries Well-Suited for SPACs: High-growth, capital-intensive sectors—such as electric vehicles (Lucid Motors), biotech, and tech—have thrived with SPACs, leveraging future projections and sponsor expertise.

Industries Better Served by IPOs: Established, profitable companies with predictable cash flows, such as consumer goods and industrials, generally fare better with the credibility and structure of a traditional IPO, especially when an existing company has mature operations and an audited track record suited to a process that often takes 12 to 18 months.

Industries Favoring Direct Listings: Companies that do not need to raise new capital and enjoy high brand recognition, such as Spotify and Coinbase, are ideal candidates for direct listings.

3 Case Studies Lucid Motors (SPAC): Lucid Motors, an electric vehicle manufacturer, went public via a SPAC merger in 2021. As a pre-revenue, high-growth company in the capital-intensive EV sector, Lucid was well-suited for a SPAC because it needed substantial funding to ramp up production and could benefit from the flexibility to provide forward-looking projections—something not permitted in traditional IPOs. The SPAC structure suited a target that needed to raise money quickly, with PIPE financing supplementing the base SPAC cash. The SPAC structure also allowed Lucid to lock in a substantial PIPE investment and to partner with experienced sponsors who could offer sector-specific expertise and credibility with investors.

Snowflake (IPO): Snowflake, a cloud-based data-warehousing company, chose a traditional IPO in 2020. The company had achieved significant scale, recurring revenues, and strong institutional investor interest. Its business model was well understood by the market, and the competitive bookbuilding process generated significant demand, resulting in one of the largest software IPOs ever. The IPO route gave Snowflake the benefit of a robust valuation process led by underwriters, as well as the credibility and visibility that come with a traditional roadshow.

Spotify (Direct Listing): Spotify, the global music streaming leader, opted for a direct listing in 2018. The company was already well-capitalized, did not need to raise additional funds, and had strong brand recognition among both consumers and investors. Spotify’s direct listing allowed existing shareholders to sell their shares directly to the market, bypassing the traditional underwriting process and avoiding dilution. The company also benefited from price discovery driven by open market demand rather than underwriter-set pricing.

Valuation and Pricing Differences

SPAC Valuation Approaches: Valuations are negotiated, often using forward-looking projections and input from PIPE investors. This can lead to aggressive pricing relative to peers in the IPO market. After the merger, the acquired company still faces the same reporting burdens as any public company.

IPO Valuation Approaches: Underwriters lead the process, using bookbuilding and investor roadshows to determine the price, typically grounded in historical performance and relying heavily on historical financial statements and market feedback throughout the longer IPO process.

Direct Listing Valuation Approaches: Prices are set by the market on day one, without underwriter intervention, creating potential for high volatility but less risk of underpricing.

Implications for Business Valuation Professionals: Valuation experts must account for differences in disclosure, forecasting, and market sentiment. The risk of mispricing is heightened, and comparable company analysis can be complicated by structural differences between paths.

Conclusion

The decision between SPAC, IPO, and direct listing is multi-faceted, with valuation, industry context, and strategic objectives all playing crucial roles. SPACs offer speed, flexibility, and access to capital but carry unique risks, especially regarding equity dilution and regulatory uncertainty. Traditional IPOs remain the gold standard for established businesses, while direct listings suit companies with strong brands that do not require new capital. For business valuation experts, a nuanced understanding of each path—and the evolving regulatory and market landscape—is essential for guiding clients to optimal outcomes. Contact AVGI today for professional business valuation consulting on choosing the right IPO path for your business.