Pre Revenue Company Valuation: A Comprehensive Guide for Founders and Investors

Valuing a pre-revenue company is both an art and a science. Without the guidance of revenues or profits, founders and investors must rely on a combination of market benchmarks, qualitative judgment, and structured frameworks. As a business valuation expert, I’ve seen how the right approach can attract high-quality investors, safeguard founder equity, and set the stage for successful growth. This guide walks you through every major consideration, method, and best practice for pre-revenue valuation and fundraising.

What Are Pre-Revenue Companies?

A pre-revenue company is a startup that has not yet generated sales or operating income from its primary product or service; pre revenue means the business is still in the pre revenue stage before generating revenue. Typically, these are early stage companies refining their offering, validating the market, or completing initial development, and that progress may include a minimum viable product, a working prototype, or early users.

Common Pre-Revenue Milestones:

- Product prototype, minimum viable product, or working prototype built

- Early customer feedback, pilots, or insight from early users

- Team assembled and key hires made

- Intellectual property (IP) protection initiated

- Partnerships or letters of intent secured

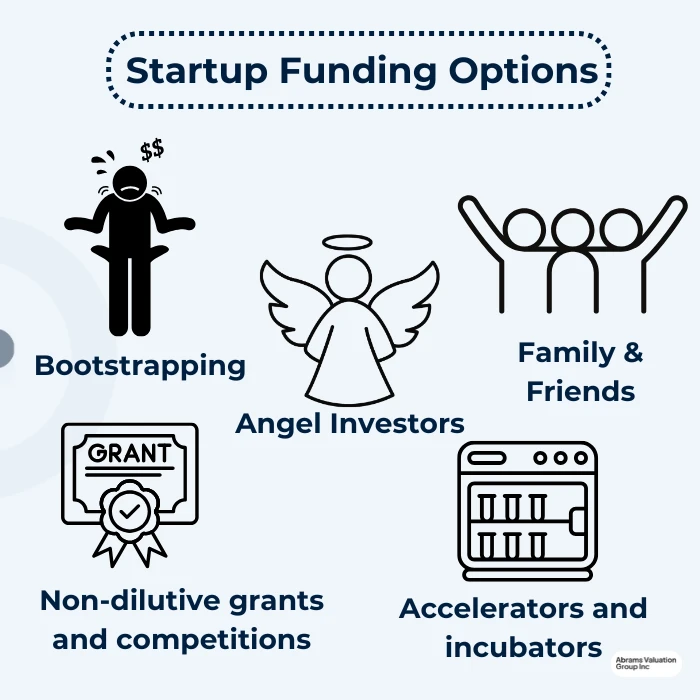

Common Funding Sources:

- Founders’ own capital (bootstrapping)

- Friends and family investments

- Angel investors

- Non-dilutive grants and competitions

- Accelerators and incubators

Key Considerations Before Raising

Before embarking on fundraising, founders must make critical assessments:

Runway Needs: Estimate the capital required to reach your next value milestone, accounting for both fixed and variable costs. Most founders aim for 12–18 months of operational runway. Many pre-revenue startups target roughly $250K to $2.5M in their first funding round, depending on the milestones they need to hit.

Product and Validation Milestones: Outline the product, technical, and market validation milestones you intend to achieve with the next capital infusion, tying them to your business model and how you plan to raise funds. These milestones will shape your fundraising narrative and valuation rationale.

Non-Dilutive Funding Options: Seek out grants, competitions, and partnerships that provide capital without requiring equity. These sources can extend your runway and reduce dilution.

Preparing for Pre-Money Valuation

Comparable Company Data: Research startups in your sector, stage, and geography, including comparable transactions in the same industry. Platforms like PitchBook, Crunchbase, and AngelList can provide data on recent pre-revenue fundraising rounds and valuations.

Conservative Financial Model: Even without revenue, prepare a detailed forecast of expenses, burn rate, and future revenue potential. Investors expect to see realistic, defensible financial assumptions.

Qualitative Strengths and Risks: Document the unique strengths of your company—such as team expertise, IP, or partnerships—and be transparent about product, market, or regulatory risks, while recording the qualitative data and qualitative factors that support your quantitative assumptions. Evidence like user interviews and LOIs can strengthen investor confidence.

Without historical financials, investors rely more heavily on qualitative assessments of future potential and growth potential.

Calculating Pre-Money Valuation

The fundamental formula is:

Pre-Money Valuation = Post-Money Valuation – Investment Amount

Inputs Checklist:

- Comp data from similar startups

- Financial projections

- Analysis of qualitative risks and strengths

- Market size and opportunity data for the target market, including market opportunity and market growth

One-Page Rationale: Summarize the logic behind your proposed valuation, referencing both qualitative and quantitative factors. In startup valuation for pre revenue companies, the case is forward-looking and shaped by the competitive environment. Transparency and data-driven reasoning are essential for credibility.

Post-Money Valuation and Share Impacts

Example Calculation: If you raise $1 million at a $4 million pre-money valuation, your post-money valuation is $5 million.

Investor Ownership = Investment ÷ Post-Money Valuation

In this example: $1M ÷ $5M = 20% ownership

A higher valuation reduces dilution, but it can create pressure if the company misses expectations. A lower valuation may appeal to investors seeking more equity for less capital.

Cap Table Impact:Update your cap table after the round to reflect new investor stakes, option pools, and founder dilution. A clear, accurate cap table prevents future misunderstandings and is often required during due diligence.

Valuation Methods for Pre-Revenue Startups

There’s no single “correct” method for valuing a pre-revenue company. Instead, these startup valuation methods for pre revenue startup valuation often rely on several common methods, while discounted cash flow and other cash flow driven approaches are usually less useful before a company starts generating revenue:

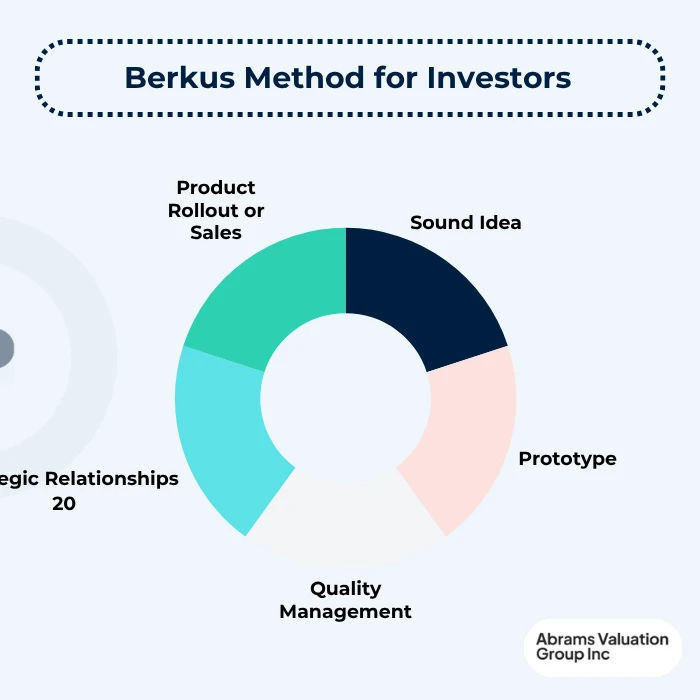

1. Berkus Method

Angel investor Dave Berkus developed this framework to assign value ranges to key company progress buckets:

- Sound Idea: Uniqueness, market potential

- Prototype: Working product, MVP

- Quality Management Team: Depth of expertise

- Strategic Relationships: Partnerships, advisors

- Product Rollout or Sales: Evidence of demand

Each factor is assigned a dollar value, and the combined estimated value is commonly capped at $2.5 million. While this can be a useful method for investors to gauge their interest in investing in a particular company, it has obvious limitations in terms of accuracy and potential bias. In order to get a clear picture of the company’s true value and potential, it’s crucial to get a professional business valuation based on sound financial forecasting to make well-informed financial decisions.

2. Scorecard Method

Start with an average pre-money valuation for similar startups in your region; for pre-revenue startups, the scorecard method is one of the most common early-stage valuation approaches. Adjust this base by assigning weightings to key factors:

- Team (30%)

- Opportunity/Market (25%): including the size and clarity of the target market

- Product/Tech (15%)

- Competition (10%)

- Marketing/Sales (10%)

- Need for additional investment (10%)

- Apply multipliers based on your own company’s strengths and weaknesses.

3. VC Method and Risk-Factor Summation

VC Method: Estimate your company’s potential exit value, then apply expected investor returns and dilution to work backward to a present valuation using the venture capital, or VC, method; venture capitalists typically underwrite pre-revenue deals to target roughly 10x to 30x returns.

Risk-Factor Summation:Start with a base valuation and adjust upward or downward for risk categories (management, market, technology, legislation, etc.) using the risk factor summation method, which helps build investor conviction by making risks explicit.

4. Cost-to-Duplicate Method

Estimate the total cost to recreate your company’s technology, IP, and progress to date. This method is best suited to deeptech or hardware startups.

How Investors Decide

Investors—angels, pre-seed VCs, and accelerators—in the pre-revenue stage rely heavily on qualitative assessments because traditional metrics are limited:

Key Decision Drivers:

- The team’s ability, relevant domain expertise, and track record

- Size and urgency of the market, including market access and the broader market opportunity

- Defensibility (IP, technology, brand)

- Early demand validation

- Competitive landscape

Qualitative Signals: Vision, founder reputation, and storytelling can meaningfully influence perceived value. At this stage, investors may accept a larger equity percentage for lower capital because risk is higher.

Angel Investors

Typical Check Sizes:$10,000–$250,000 per investor, often syndicated.

Expectations: Angels want transparency, founder commitment, realistic milestones, and a clear vision; many specialize in high-risk pre-revenue companies and weigh qualitative factors heavily.

Preferred Instruments: Most prefer SAFEs (Simple Agreements for Future Equity) or convertible notes for pre-revenue rounds, though negotiating with angel investors can lead to a more complex financing agreement than founders expect. A valuation cap sets the maximum price at which those instruments convert in a future funding round.

Pre-Seed VCs and Accelerators

Pre-Seed VC Expectations: Early traction, market validation, and a scalable team; in pre-seed rounds, many pre-seed VCs invest roughly $250K to $2.5M.

Accelerator Trade-Offs: Accelerators provide mentorship, networks, and structure—often for 5–10% equity in exchange for $125K–$500K, and strong programs can improve readiness for the next round.

Pitch Deck for Pre-Revenue Rounds

A compelling pitch deck is essential, and the business plan behind the story should be clear to any potential investor. Prioritize:

- Team Slide: Highlight relevant experience and commitment

- Demand Evidence: Show pilots, user engagement, or market research

- Clear Use-of-Funds: Specify how capital will drive milestones

- Milestones and KPIs: Outline achievable, time-bound goals

- How Much Equity to Offer

- Target Dilution Range:

10–20% in your first institutional round is standard. - Option Pool:

Allocate an option pool (typically 10–15%) before calculating investor ownership. - Advisor Equity:

Budget a separate line (e.g., 0.5–2%) for key advisors.

Equity Dilution Mechanics

- Multi-Round Modeling:

Model your cap table across several future rounds to anticipate long-term dilution. - SAFE/Convertible Note Impact:

Understand and illustrate how these instruments convert into equity, affecting ownership percentages. - Anti-Dilution Provisions:

Be aware of basic anti-dilution protections (weighted average, full ratchet) and their implications. Read our full guide on preventing equity dilution here.

- Preparing for Negotiations

- Term Sheet Negotiation Checklist:

Review key terms: valuation, option pool, board structure, voting rights, liquidation preferences. - Non-Negotiable Governance:

Founders should be clear on which items are non-negotiable (e.g., board control, vesting schedules). - Cap Table Scenarios:

Run multiple scenarios to be prepared for negotiation outcomes. - Closing, Post-Money Steps, and Compliance

- Legal Documentation:

Work with experienced startup counsel to finalize investment agreements. - Update 409A/Fair Market Value:

Obtain or update your company’s 409A valuation before issuing new stock options. - Team Communication:

Clearly communicate new ownership and dilution to your team to maintain trust and alignment.

Final Thoughts

Valuing a pre-revenue company requires careful preparation, honest self-assessment, and a willingness to justify your assumptions. By leveraging multiple valuation methods, building a credible financial plan, and communicating transparently with potential investors, founders can maximize their chances of raising capital on fair, favorable terms. For investors, a clear and balanced approach to pre-revenue valuation helps balance risk with opportunity and supports long-term partnership success. Impactful decisions need expert knowledge and experience to guide them. Contact AVGI today for a professional, unbiased pre-revenue business valuation of your company or a potential investment.