Understanding the Valuation Discounts of S Corp Stock for Tax Benefits

In the complex world of taxes, S Corporations are treated differently than C corporations. Savvy taxpayers can take advantage of these differences to maximize their tax benefits and reduce their tax obligations. Whether you invested in an S Corporation yourself, received S Corp shares as part of an inheritance, or otherwise have an interest in an S Corporation, it is well worthwhile to explore the valuation discounts for S Corp stock that you might be able to leverage.

Determining Fair Market Value for S Corp Stock

The fair market value of S Corp stock is used to determine the value of a business interest for estate tax purposes and is often used in conjunction with valuation discounts. Fair market value is the standard of valuation for estate tax purposes and is defined as the price at which a willing buyer and willing seller would agree to a transaction.

The fair market value of S Corp stock is also heavily influenced by various factors, including the nature of the business, economic outlook, book value, and earnings capacity, among other factors. Very often, the actual fair market value of the S Corp stock is lower than the listed value in company financial reports. This is largely due to applicable valuation discounts. When S Corp sock is part of your financial profile, AVGI highly suggests getting an appraisal by qualified valuation experts. A qualified appraisal can back a significantly lower tax obligation on S Corp stock than the IRS might initially present as your tax obligation.

Valuation Discounts and Their Applications for S Corporations

Valuation discounts are used to reduce the value of S Corp stock for estate tax purposes. Practically, this allows gifts of an ownership percentage to children or grandchildren at a reduced tax rate.

The most common valuation discounts used in transferring ownership interests in family-owned businesses are those for lack of marketability and lack of control. AVGI explores these valuation discounts as they relate to S corporation shareholders.

Lack of Marketability:

This discount reflects that unlike publicly traded companies, interests in closely-held businesses have no ready market and is often called a liquidity discount. Because S Corporations are privately held businesses, there is no ready market for owners to sell their shares to if they wish to exit the company. This presents a real challenge in liquidating their share of ownership, discounting the value of their S Corp stock compared to publicly traded stock, which can be easily sold. (This discount may not be applied if there is a company ESOP in place, as that creates an internal market for the company shares to be sold. Learn more about selling to an ESOP with AVGI’s thorough analysis)

Lack of Control:

This discount is applied when the ownership interest is not in control or consists of non-voting shares. This reflects that owners of such interests cannot make or influence critical business decisions about how the company is run. This discount is often in the 25% range, depending on the company’s unique circumstances and ownership interest.

Very often, those holding S Corporation stock can take advantage of both discounts for lack of control and marketability, which significantly reduces the business valuation of the partial ownership interest. This lower valuation more accurately depicts the value of the stock and can effectively reduce the total due on the taxpayer’s income tax, gift tax, and estate tax bills.

Maximizing Tax Benefits with S Corp Valuation

S Corp valuation can provide significant tax benefits, including reduced gift tax and estate taxes. As S Corporation election allows the company to enjoy pass-through tax entity status, the S corp avoids federal corporate tax and the dreaded “double-taxation.”However, the flip side of the pass-through entity coin is that S Corp value can be highly overstated without appropriate valuation adjustments. This is because the S Corp’s cash flows are stated in pre-tax dollars, while the actual tax is applied at the individual level. One S Corp valuation discount method to combat this problem is called tax affecting. AVGI breaks down tax affecting for S Corps in greater detail.

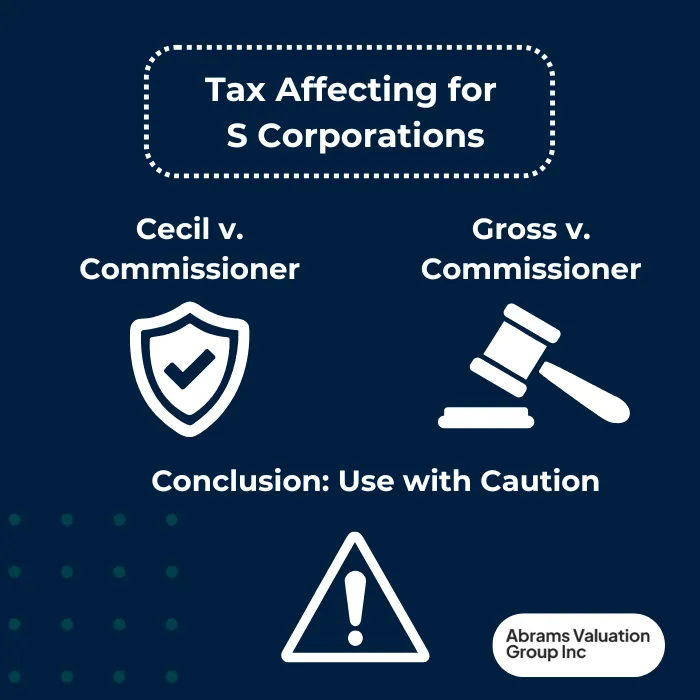

The Tax Affecting Controversy for S Corporations

Tax affecting is a valuation approach that applies a hypothetical entity-level tax to a pass-through entity’s taxable income, reducing the business’s overall value. This approach has garnered attention, particularly after the recent case of Cecil v. Commissioner, where the U.S. Tax Court upheld the use of tax affecting for valuing S corporation shares for federal gift tax purposes. In this case, both the taxpayer and the IRS acknowledged that the projected cash flows of the S corporation should be adjusted to reflect the tax liabilities that shareholders would incur at the personal level.

Historically, the IRS has resisted the application of tax affecting, such as in the case of Gross v. Commissioner. The IRS argued that since S corporations themselves are not subject to federal tax at the entity level, applying such a tax to determine value is inappropriate. However, taxpayers have contended that future income streams flowing through to shareholders should indeed reflect any personal tax obligations, advocating for a valuation adjustment.

The Cecil case offers a potentially favorable precedent for taxpayers, suggesting that tax affecting could be accepted in certain contexts. Yet, it is crucial to note that the Tax Court’s ruling emphasized the case’s unique circumstances, acknowledging that tax affecting may not be routinely applicable to S corporation valuations. The court did not clarify specific factors that might consistently justify tax affecting, leaving considerable room for ambiguity in its wider application.

Therefore, while tax affecting could lead to significant tax benefits for S corporation shareholders by reducing the perceived value of their ownership interests and thereby minimizing tax liabilities on transfers, it needs to be appraoched with caution. The precedence of tax court decisions falling on either side of the fence mean that tax affecting is still not a widely accepted standard valuation practice, and needs to be carefully applied in specific scenarios. Taxpayers should approach this valuation strategy cautiously, recognizing the potential benefits while remaining aware of the lack of a unified standard governing its use.

In Conclusion: Valuation Discounts of S Corp Stock

Understanding the valuation discounts available for S Corp stock is essential for taxpayers who wish to maximize tax benefits while meeting their tax obligations. Key factors such as fair market value, lack of marketability, and lack of control play a significant role in determining the true value of your S Corp shares. Where appropriate, tax affecting can potentially lead to substantial tax savings, but this method must be used with a lot of caution. For a precise and comprehensive valuation that accurately reflects the value of your business interests, it is imperative to consult with qualified valuation experts. Contact AVGI today to ensure your S Corp stock is appropriately valued and to optimize your tax strategy.