How to Calculate Lost Profits Precisely in Litigation

Business is a fast-paced world where time is money. The business loses a lot when outside interference or a wrongful act disrupts regular operations. The business may seek damage reparations through litigation. But how can we accurately quantify these damages? In this article, AVGI presents a real-life case (all identifying details have been altered) with simplified formulas to help businesses calculate lost profits and lost inventory damages for litigation purposes.

What are Lost Profits?

Lost profits occur when something disrupts normal business operations, resulting in economic damages from the unrealized profits that the business could not make during the downtime. Lost profits can arise from various factors, including breach of contract, intellectual property infringement, or liability. Lost profits damages are a primary damage that businesses pursue in business litigation. Therefore, it is highly relevant for business owners to understand how these damages can be calculated accurately.

Lost profits damages can be either direct or consequential. Direct damages flow directly and immediately from the interference (i.e., breach of contract), while consequential damages arise from losses deemed reasonably foreseeable by the interfering party.

To recover lost profits, a party must prove the revenues it would have generated and the total expenses that would have been spent generating those revenues. AVGI experts have been engaged in many litigation cases to quantify damages and serve as expert witness to support the client’s case. An expert witness is often a crucial part of a successful lost profits litigation, particularly when the data is complex for the layman to interpret.

What is Lost Inventory?

Lost inventory is a separate category of damages referring directly to the cost of inventory that was produced and subsequently destroyed by the disruptive event. Alternatively, it can refer to We will examine how to calculate both types of damages in the article.

Lost Profits Litigation: A Real-World Case

A fire broke out in Sir Harvard Cucumber’s manufacturing firm, Cucumber Pickles (CP), and spread to his next-door neighbor’s firm, Billabong’s Boomerangs (BB), owned by Constance Billabong. BB sued CP for a variety of different damages.

In this case, there are two main categories of damages:

Two Categories of Damages

The cost of the lost inventory (burned boomerangs)

The lost profits from lost sales of boomerangs

Digging deeper, there are two categories of lost profits:

Two Categories of Lost Profits

Lost profits from the inventory that was produced and destroyed

Sales were lost from inventory that was never produced because the Company could not take new orders for one day and did not manufacture the inventory for the orders that were not taken.

In this article, we will calculate the Lost Profits and Lost Inventory Damages in different ways to address each category of damages and to reach the most accurate and reasonable damage calculation.

Determining Damages for a Manufacturing Company

First, we examine the manufacturing costs and profits with and without the fire. Then, we can take the difference to determine the damages. Fixed manufacturing overhead, as well as general & administrative expenses, are costs that BB would have incurred with or without the fire, so they are not considered in calculating the lost profits damages.

In this case, the lost inventory of burned boomerangs totals $95, and the lost profits from unmade boomerang sales come to a total of -$5 in net income. The total lost inventory and lost profits damages calculation comes to $90.

Lost Inventory Formula

This formula states that the inventory damages are the variable manufacturing costs that relate directly to producing the inventory.

Lost Profits Calculation

The lost profits are calculated by subtracting the VM costs and Selling Expenses from the Sales.

Combining the Lost Inventory and Lost Profits Formulas yields a Total Damages Formula:

Total Damages Formula

The Total Damages Formula simplifies the calculation, as the VM costs would have been incurred with or without the fire, so they are not included in the damages. BB’s total damages are $100 in Sales – $10 in selling Expenses = $90 Total Damages.

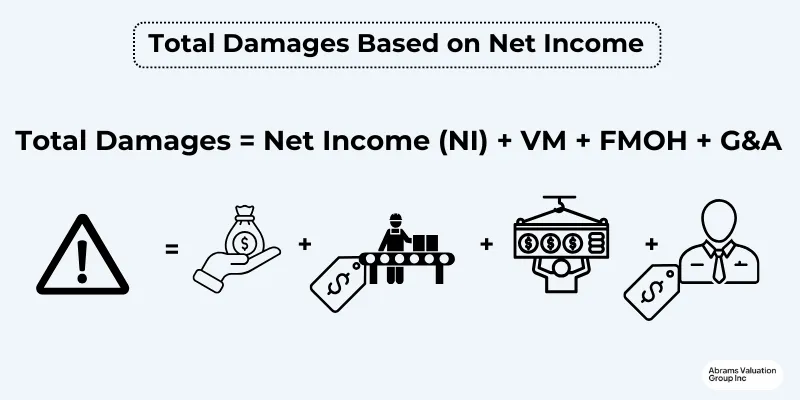

Calculating Lost Profits & Total Damages Based on Net Income

Now, we’ll examine an alternative way to calculate damages based on Net Income. (For the full derivation of the formula, please see the full article here).

This formula works off of net income to determine the damages. We add the VM costs to account for the lost inventory (burned boomerangs). Adding the FMOH lets us examine the incremental profits analysis, which is the relevant measurement in damage calculations. (GAAP uses absorption costing for financial statements, subtracting FMOH from Net Income.) Lastly, the General & Admin expenses also need to be added to give us a full incremental profit picture.

Using the Net Income formula, we reach the same total damages calculation of $90 for BB.

Determining Lost Profits Based on Net Income

The lost profits on the destroyed inventory can be calculated by adding the Fixed Manufacturing Overhead Costs and General & Admin expenses to the Net Income before the fire. This formula yields -$5, the same lost profits calculation as the previous method.

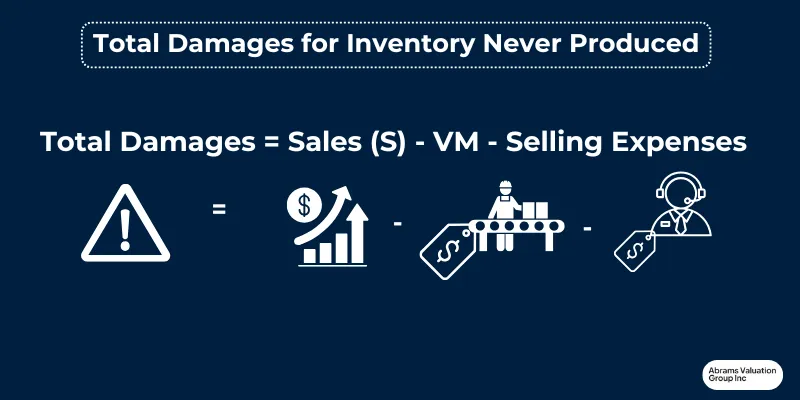

Lost Profits Damages Calculated by EBITDA for Lost Sales on Inventory Never Produced

In this litigation, BB was a wholly-owned subsidiary of Sticks & Stones, Inc., a publicly traded company. Sticks & Stones annual report listed BB’s EBITDA at -$40 million. The plaintiff claimed that the fire in BB’s local manufacturing plant caused an electrical outage that crashed the Sticks & Stones nationwide computer sales system, effectively interrupting sales for the whole company across the country for an entire day. Furthermore, each order is customized, so no sales made meant no inventory was produced. This information necessitated a different approach to calculating lost profits on inventory never produced.

Total Damages for Inventory Never Produced

These calculations differ from the previous methods as the inventory was never produced, so the direct manufacturing costs (VM) were never incurred. Here, we assume the VM costs were $65 rather than the previous $95.

Making the calculations for BB, we determined the damages to be $25 for boomerangs never produced.

Lost Profits Based on EBITDA

AVGI derived this formula to calculate the lost profits based on EBITDA, as that was the information available in this case. Plugging in the relevant data for BB to this formula gives us the Lost Profits for the entire year of 2001, the year of the fire.

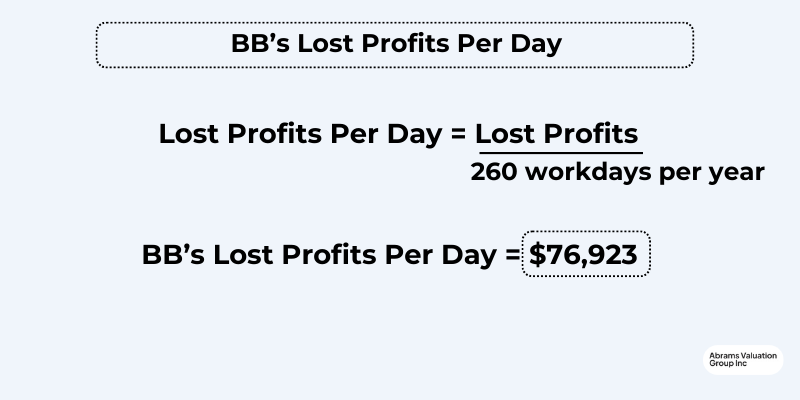

Since the fire only put regular company operations on hold for one day, we need to determine the lost profits per day.

The result is a lost profits calculation of $76,923 for the single day of disrupted operations, contrary to the plaintiff’s accountant’s claims of hundreds of thousands of dollars in lost profits. Accurately calculating lost profits damages is critical to ensuring that the case is ruled justly and the wronged parties receive the proper reparations.

Applying AVGI’s Lost Profits Formulas to Other Litigations

As the facts in every case differ, it is crucial for the professional performing the damage calculation to use common sense in applying these formulas to other scenarios. The correct path in certain cases may be to make specific modifications to the formulas based on the facts of the scenario to produce the most accurate damage calculation for that particular case.

4 Common Misperceptions About Lost Profits Claims

Below are 4 common misconceptions businesses may have going into a lost profits litigation. It is important to clarify these points to avoid misunderstandings and unrealistic expectations.

Misconception: Lost profits equal lost revenues.

Fact: Lost profits damages are lost “net” profits, not loss of revenue or loss of gross profit.

Misconception: Businesses that lose money don’t sustain lost profits.

Fact: A business operating at a loss can still sustain damages from lost profits. Obviously, it will depend on the details of the particular case, but even a business operating at a loss may be able to claim lost profits.

Misconception: All decreases in business should be included in the lost profits claim:

Fact: Claims for lost profits should only include lost profits caused by the defendant’s actions.

Misconception: Future profits claims for new businesses are speculative & therefore not recoverable lost profits:

Fact: Courts have moved away from the “new business rule” and now consider the quality of evidence presented.

Mitigating Lost Profit Damages

Economic experts will consider any potential efforts the affected business could have made to mitigate those losses and factor them into the calculations. Mitigated losses can reduce the amount of damages suffered by the business. The affected business should take reasonable steps to mitigate losses and minimize the impact of the disruption. This also assists in supporting the plaintiff’s claim for loss of profits, as they demonstrate that despite their best efforts to mitigate the damages, the wrongful act still inhibited the Company’s ability to generate profits during that time.

In Conclusion: Accurately Determining Lost Profits for Litigation

AVGI has developed these formulas to help calculate lost profits with reasonable certainty. These formulas are far more empirical than some of the more standardized damage calculation methods and can withstand scrutiny in a court of law- a crucial point in litigation. AVGI brings over 30 years of damage calculation and expert witness experience to each litigation. If you are facing business litigation involving lost profits damages, we encourage you to contact us for a free consultation.