What is Standard of Value & How it Affects Your Business Valuation

As a savvy business owner, you want to understand and communicate your company’s value. But which standard of value are you using? Is that the fair market value or the book value of the company? Does it make a difference? Understanding the various business valuation standards is crucial for accurate valuation.

In this comprehensive guide, AVGI’s experts delve into the various standards of value in business valuation and how they can impact the overall valuation of your business. Whether you’re gearing up for a potential sale, seeking investment, building your case for litigation, or simply curious about the value of your business, understanding the standard of value is crucial for making informed decisions and communicating your company’s value to others. So, let’s dive in and explore the significance of the standard of value in business valuation.

Defining the Standard of Value

In the world of business valuation, the standard of value refers to the specific premise under which the valuation is being conducted. It’s essential to recognize that different standards of value are used for different valuation purposes, and each standard can yield varying results. Understanding these business valuation terms is crucial for accurately determining the value of your business. The following are the key standards of value in business valuation and their impact on your business’s worth:

Fair Market Value

Fair market value is the price at which a property or asset would change hands between a willing buyer and a willing seller in an open and unrestricted market, neither being under compulsion to buy or sell, and both having reasonable knowledge of relevant facts. For instance, when selling a piece of real estate, the fair market value is an essential benchmark for determining the listing price. Fair market value is most commonly used for business valuations for transactions such as sales, mergers and acquisitions, estate planning, and tax-related matters. This standard of value is widely accepted and recognized by the Internal Revenue Service (IRS) and is often a key factor in determining the value of assets.

Investment Value (Strategic Value)

Investment Value, also known as Strategic Value, is a standard of value used in business valuation that takes into consideration the specific value a particular buyer places on an acquisition. This value is often higher than the business’s intrinsic value to that specific buyer due to synergies, strategic benefits, and other prospective gains that the buyer expects to achieve through the acquisition.

Investment Value is commonly used when a strategic buyer, such as a competitor or a company looking to expand into new markets, is considering acquiring a business, and the value is specific to the particular owner. This standard of value is especially relevant when the buyer’s ability to derive significant value from the acquisition is higher than that of other potential buyers due to strategic advantages, cost-saving opportunities, or synergies with their existing operations.

Unlike Fair Market Value, which assumes a hypothetical transaction between a willing buyer and a willing seller, Investment Value is buyer-specific and tailored to the individual circumstances of the acquiring party. It reflects the unique advantages, opportunities, and potential synergies that a particular buyer can realize from the acquisition.

Investment Value is often used in mergers and acquisitions, strategic partnerships, and joint ventures, where the focus is on the strategic benefits and synergies that can be derived from the transaction rather than simply the business’s standalone financial worth.

In summary, Investment Value, or Strategic Value, is utilized when a specific buyer can realize greater value from an acquisition due to synergies, strategic advantages, and other unique benefits that are specific to that buyer’s situation.

Fair Value for US Financial Reporting

Fair Value is the standard of value established by the Financial Accounting Standards Board (FASB) for US financial reporting in the Accounting Standards Codification (ASC) 820. It provides greater financial transparency and uniformity for any parties interested in a company’s financial statements. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Fair value considers the entry and exit price of the asset or liability, reflecting current market conditions and the perspectives of both buyers and sellers. This standard is also known as “exit value.” In business combinations and M&A transactions, it is essential to allocate purchase prices to assets based on the fair value standard to ensure compliance with financial reporting standards.

Fair Value for Litigation

In litigation proceedings, Fair Value in shareholder oppression and shareholder dissolution suits is determined by state law. Although it has the same name as Fair Value for financial reporting, it is a distinct standard of value that varies according to the laws of that particular state. The term “Fair Value” in this context refers to righting wrongs and many states are focused on making an abusive situation fair once again through judicial proceedings.

In many (but not all) states, state law uses the more subjective premise of value to the holder instead of the more objective value in exchange. This often means a proportionate value of the entire business, without discounts for lack of control or marketability (which would otherwise devalue the minority shareholder’s value).

It is important that the appraiser ascertain—sometimes with the help of an attorney—the appropriate premise and level of value, as well as obtain legal guidance as to the treatment of the valuation discounts when performing a state-law mandated Fair Value assignment. This elements are crucial to clarify at the beginning of the assignment so that the appraisal results accurately reflect the value in context of the litigation.

Book Value

Book value, also known as carrying value, is the value at which an asset or liability is carried on a company’s balance sheet. It’s calculated by subtracting the accumulated depreciation or amortization from the asset’s original cost.

Carry Value

Carry value, also referred to as carrying value, is another term for book value. It is the value of an asset or liability as it appears on the financial statements. It serves as a useful indicator of an asset’s current worth.

Market Value

Market value is the current price at which an asset or publicly traded security can be bought or sold. This standard is commonly used in the stock market to assess the worth of publicly traded companies.

Assessed Value

The assessed value is the dollar value assigned to a property by a taxing authority for tax purposes. Local governments use this value to determine property taxes.

Historical Cost

Historical cost is the original cost of an asset as recorded in the books of accounts. It is used to value assets in financial statements.

Why the Standard of Value Matters in Your Business Valuation

The standard of value used in business valuations plays a crucial role in determining the outcome of the valuation process. Using the wrong standard of value can lead to significant discrepancies in the valuation result and can have profound implications for business owners, investors, and other stakeholders. Let’s delve into why the standard of value matters and how using the wrong standard can impact the valuation of a business.

Imagine a scenario where a business owner is looking to sell their company. The business has substantial value due to its strategic positioning in the market and its potential for future growth. However, if the valuation is conducted using the wrong standard of value, such as using the book value rather than the fair market value, the estimated worth of the business could be significantly undervalued. Accurate financial assessments, including the valuation of cash equivalents, are crucial for determining the true worth of a business. As a result, the business owner may end up selling the company for far less than its actual market worth, leading to a substantial financial loss.

Conversely, consider the scenario of a potential investor who is considering acquiring a business. The investor does not stand to gain any particular strategic business advantage in acquiring the business; the investor identifies with the social impact mission of the target company. However, if the valuation is conducted using Investment (Strategic) Value, that would overstate the worth of the business, and the investor may end up overpaying for the acquisition. This can lead to financial strain and potential negative repercussions for the investor, especially if the actual market value of the business does not align with the inflated valuation.

Using the correct standard of value is essential for fairness, accuracy, and transparency in business valuations. It ensures that all parties involved have a clear understanding of the true value of the business and can make informed decisions based on reliable valuation metrics.

Using the appropriate standard of value in business valuation is critical for ensuring that the valuation accurately reflects the business’s true worth. Failure to use the correct standard of value can result in undervaluation, overvaluation, and, ultimately, detrimental financial consequences for business owners, investors, and other stakeholders. Therefore, it is paramount to carefully consider and accurately apply the relevant standard of value to uphold the integrity and reliability of the business valuation process.

How Different Standards of Value Compare: Drawing Comparisons and Contrasts

Now that we’ve outlined the various standards of value let’s examine some key comparisons and contrasts between different types of value:

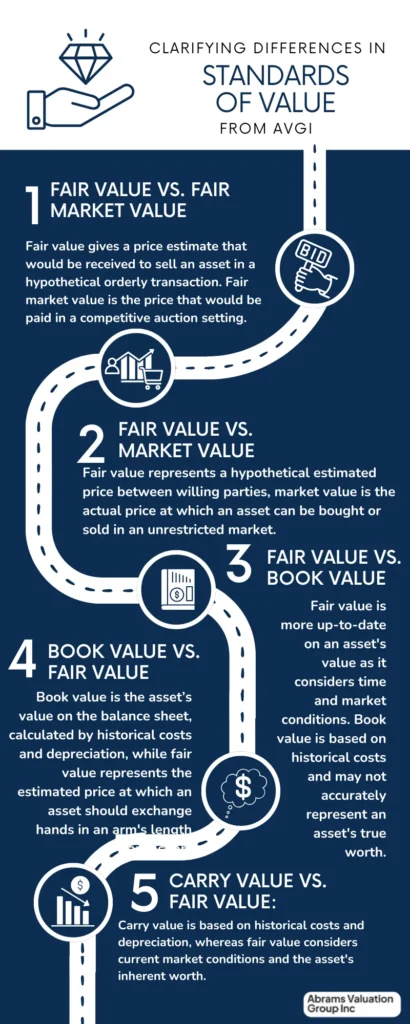

Fair Value vs. Fair Market Value Standards

While Fair value and the fair market value standard are both commonly used standards of value, they have distinct meanings, especially in the context of U.S. Financial Reporting.

Fair value (for US financial reporting) is based on the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Fair value considers the entry and exit price of the asset or liability, reflecting current market conditions and the perspectives of both buyers and sellers.

On the other hand, fair market value is defined as the price at which an asset would sell in a competitive auction setting, assuming both buyer and seller are willing participants and both have reasonable knowledge of the relevant facts. Fair market value typically emphasizes the conditions of the market at the time of the sale, without the same consideration of market participants that fair value requires.

While Fair Value is measured based on market participant assumptions and may consider hypothetical transactions and data from inactive or less active market. In contrast, Fair Market Value focuses almost exclusively on actual transactions in active markets and willing participants in the marketplace.

Fair Value is the GAAP-mandated standard of value for certain types of reporting (for example, financial instruments), whereas fair market value is often referenced in tax assessments and legal proceedings.

In summary, while both fair value and fair market value are about determining asset prices, their differences lie in their definitions, measurement approaches, market considerations, regulatory contexts, and intended uses in financial reporting.

Fair Value vs. Market Value:

While fair value represents a hypothetical estimated price between knowledgeable and willing parties, market value reflects the actual price at which an asset can be bought or sold in an unrestricted market. Fair value takes into account the specific circumstances of both the buyer and seller, whereas market value is based on current market conditions.

Fair Value vs. Book Value:

Fair value is often considered a more accurate reflection of an asset’s value as it considers variables such as time and market conditions, while book value is based on historical costs and may not accurately represent an asset’s true worth.

Book Value vs. Fair Value:

Book value is the value of an asset as it appears on the balance sheet, calculated based on historical costs and depreciation, while fair value represents the estimated price at which an asset should exchange hands in an arm’s length transaction.

Carry Value vs. Fair Value:

Carry value and fair value can differ significantly. Carry value is based on historical costs and depreciation, whereas fair value considers current market conditions and the asset’s inherent worth.

Understanding Standard of Value: In Conclusion

Understanding the standard of value is essential for gaining insights into the valuation of your business. By recognizing the impact of different standards of value, you can make more informed decisions regarding the financial aspects of your business. Whether you’re contemplating a sale, seeking investment, involved in litigation, or simply aiming to assess your business’s worth, understanding the various standards of value is invaluable in the world of business valuations. Armed with this knowledge, you can take confident steps toward maximizing the value of your business.

FAQs about Standard of Value

How does the choice of standard of value impact the valuation of my business?

The choice of standard of value can significantly impact the valuation outcome, as each standard has specific criteria and considerations that can influence the final value of your business.

Are there instances where multiple standards of value may be applicable to my business?

Yes, depending on the purpose of the valuation and the industry standards, multiple standards of value may be relevant to your business. It is best to consult with a business valuation expert about your specific business needs.

What role does fair value play in financial reporting?

Fair value is crucial in financial reporting as it provides a standard for measuring the value of assets and liabilities. Fair value is essential for financial statement preparation that is compliant with FASB requirements. This makes company financial statements more useful for lenders, investors, investment analysts, and shareholders, and others who wish to review financial reports.

How can I determine the most appropriate standard of value for my business?

The most appropriate standard of value for your business depends on the purpose of the valuation, industry standards, and specific circumstances surrounding your business. The best option is to have an experienced appraiser assess your business valuation needs and select the appropriate standard of value that will most accurately represent your company’s value in the particular situation. Contact Abrams Valuation Group, Inc. for a free consultation.